Radiant Capital is a new cross-chain decentralized lending protocol that has achieved outstanding results on the Arbitrum chain. The protocol enables cross-chain operations through Layer Zero and Stargate, optimizing user experience and expanding its business line. This article constructs an RDNT valuation model, using a comprehensive range of valuation methods such as DCF, P/TVL, P/S, and P/E, to predict the fair value of RDNT at the end of 2023.

TL;DR

-

Radiant Capital is a decentralized lending protocol that operates on multiple chains, enabling users to deposit any major digital asset and borrow other platform-supported assets across chains. Radiant Capital’s cross-chain operations are built on Layer Zero and Stargate, allowing users to cross-chain lending and liquidity mining.

-

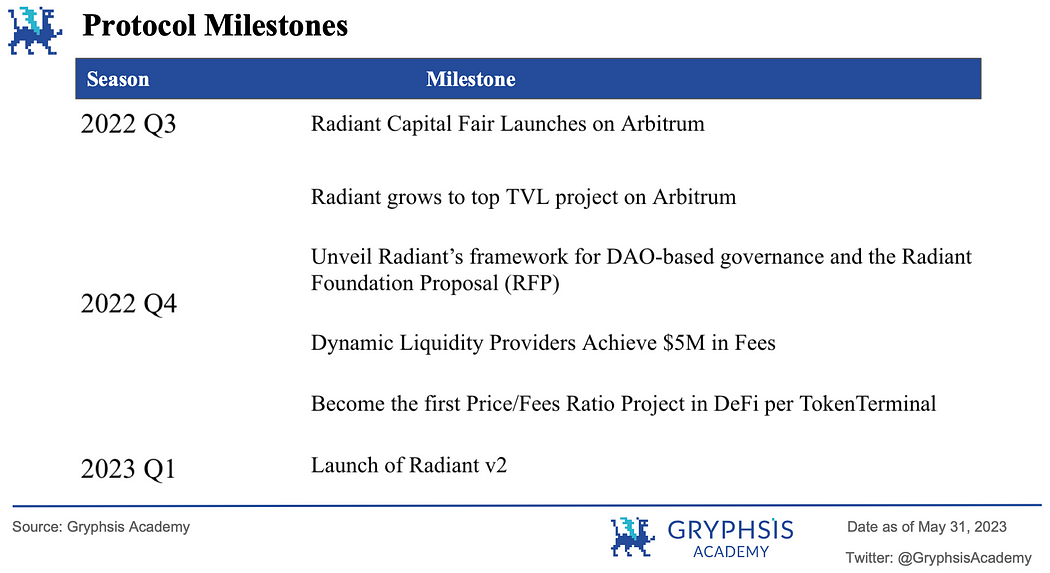

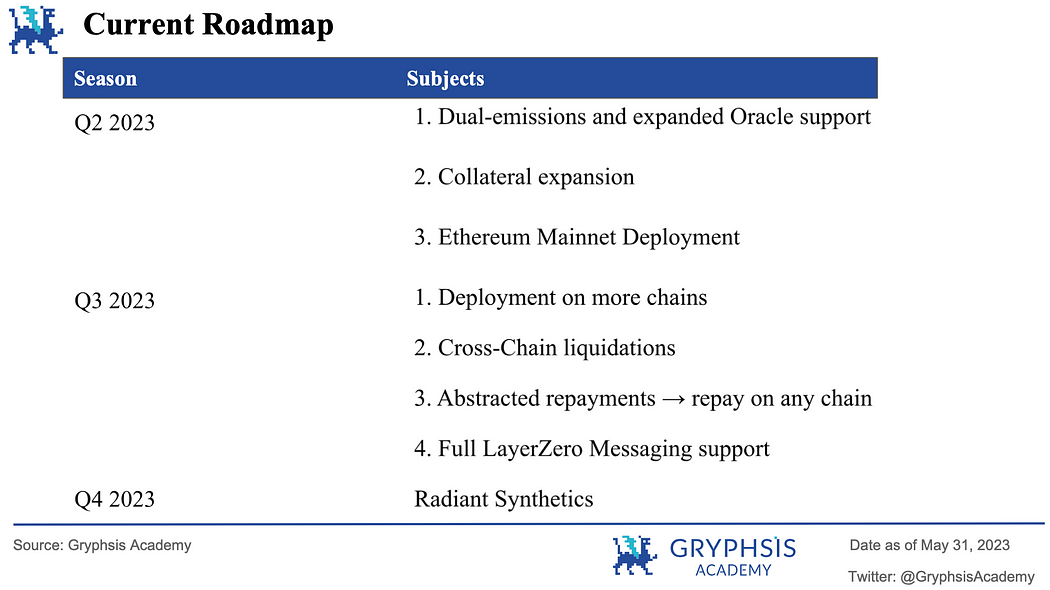

Radiant Capital has achieved milestone achievements, including becoming the highest TVL lending project on the Arbitrum chain and the launch of Radiant Capital V2. The current roadmap includes cross-chain liquidation functionality, abstract repayment (repayment on any supported chain with one click), collateral expansion, and application deployment on more chains.

-

The total supply of RDNT tokens is 1 billion, distributed to Incentives, team, reserves, contributors, treasury & LP, and liquidity providers. All tokens will be fully unlocked by July 2027.

-

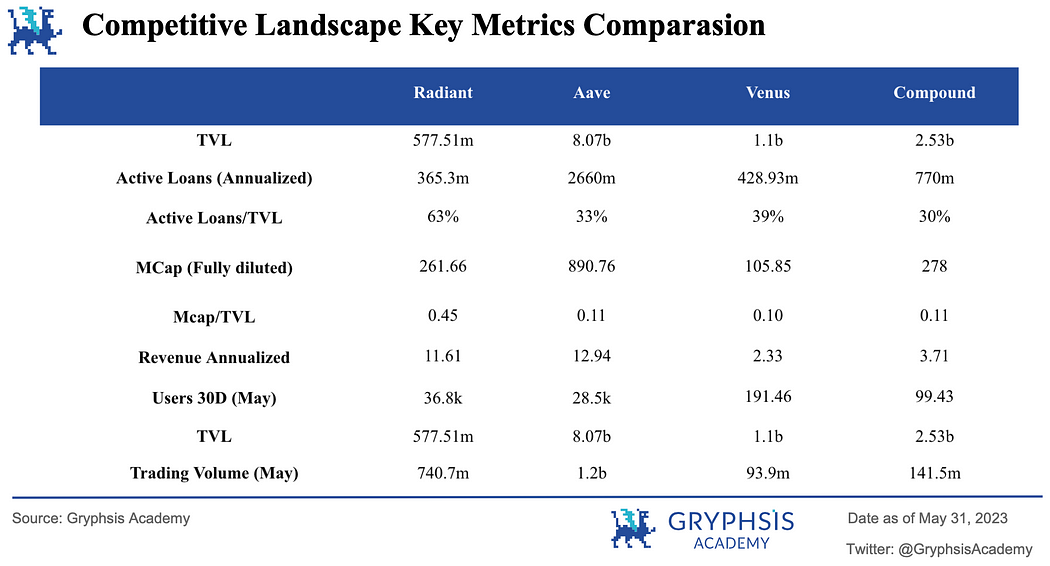

Radiant’s revenue and trading volume have both grown significantly, indicating an increasing demand for the protocol’s applications. Radiant is a leader on the Arbitrum chain, with high TVL and a large user base. Radiant’s revenue in 90 days has exceeded that of Aave and Compound, and its user participation, cumulative users (216,831), and trading volume ($740.7 million) in May have all performed well.

-

According to a probability-weighted DCF valuation, RDNT is expected to be worth $168.14 million by December 2023, with a token price of $0.37. Considering the P/TVL, P/E, P/S ratios and the weighted DCF, the price range obtained from a comprehensive analysis is between $0.45 and $0.67. Of course, the actual token price depends on future market conditions and protocol operations.

-

Suggestions for Radiant include further integration of omnichain solutions, optimizing user experience, diversifying collateral types, expanding its business line, and integrating with other DeFi protocols to create a comprehensive financial ecosystem.

1. Protocol Overview

Radiant Capital is a decentralized cross-chain lending protocol built on LayerZero. Its aim is to create a universal money market where users can deposit any major asset on any major blockchain and borrow various supported assets across chains, thus eliminating liquidity silos. Unlike most cryptocurrency lending platforms, Radiant Capital does not require users to choose a specific chain to work with nor does it limit the use of specific tokens of that chain. Instead, Radiant Capital plans to operate on most major blockchains, making it easier for users to borrow assets and generate returns by contributing their capital to lending. Radiant Capital generates actual revenue through its protocol fees and related activities. Investors can deposit their assets on the platform and earn returns by locking, vesting, and lending out their assets. Through the lending mechanism, users can use their assets as collateral to increase their liquidity.

Overall, Radiant Capital offers a more flexible and inclusive approach to decentralized lending, making it easier for users to obtain liquidity across multiple chains while earning returns for their assets. As Radiant Capital continues to develop and expand, it has the potential to become a leader in the cross-chain money market space.

2. Team and Financing Status

2.1 Team

Radiant Capital has a team of 14 members, many of whom have worked for companies such as Morgan Stanley, Apple, and Google. They have been involved in the DeFi space since early summer 2020, with many of them having been involved in cryptocurrencies as early as 2015.

2.2 Financing

Radiant Capital’s initial founders and developers completely self-funded the development of the project. There were no private sales, IDOs, or venture capital involved in the project, which is in line with the unbiased decentralized philosophy.

3. Route and K-line chart

3.1 Historical events and price trends

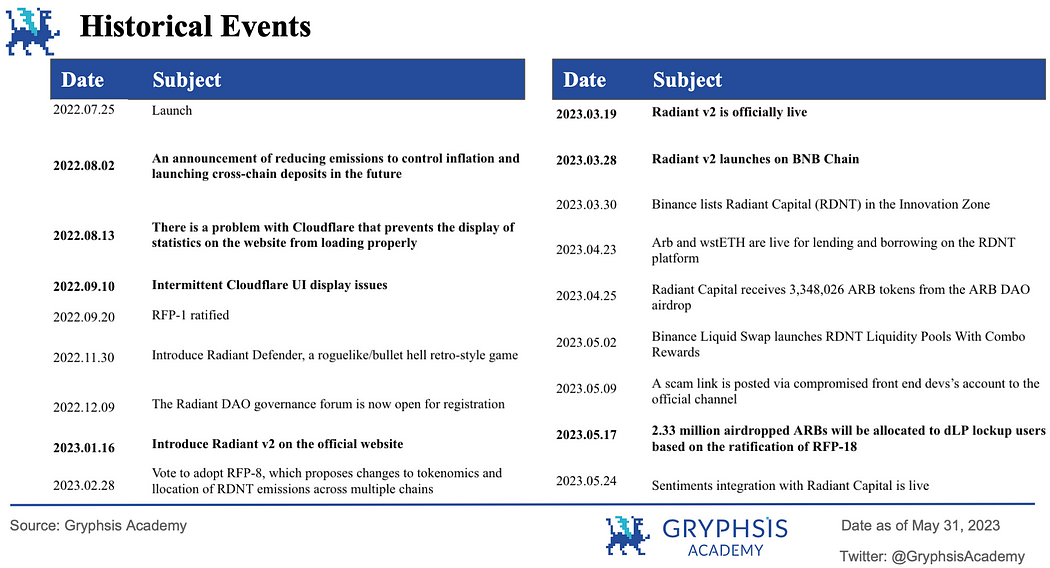

Major events and announcements have led to fluctuations in the prices and total locked-in value (TVL) of decentralized lending protocols such as Radiant Capital. From the chart, we can see that on August 2, 2022, when the team announced its intention to control token inflation, the price and TVL of RDNT both rose significantly. Conversely, when problems occur with the protocol, such as statistical data loading errors and UI display issues, user confidence may decline, leading to a decline in RDNT price and TVL. On January 16, 2023, the team announced that Radiant v2 would be released in the future, which was seen as positive news by the public; the price of the coin began to rise (of course, also affected by the overall trend of the blockchain market), and TVL doubled. Next, when Radiant v2 was officially launched on March 19, 2023, the version transition caused TVL to temporarily decline. However, with the stable operation of the V2 version, TVL quickly recovered in the following days. On March 28, Radiant v2 was extended to the BNB chain, which brought in huge traffic and caused TVL to rise rapidly in a few days.

This inspires us to pay attention to the significant events and announcements of a project, changes in user sentiment, and overall market conditions that may affect the price and TVL of decentralized protocols when investing.

3.2 Completed Milestones

3.3 2023 Roadmap

3.4 Version Roadmap

3.5 Business Progress

4. Business Composition and Code Implementation Logic

Radiant Capital’s cross-chain operations use Stargate’s stable routing interface and are built on Layer Zero. Radiant Capital allows users to deposit their assets from major blockchains and lets other users borrow those assets without intermediaries. Those who contribute funds to the platform can earn lower-risk returns.

Radiant lending market supports many assets on Arbitrum chain and BSC smart chain. On Arbitrum, users can deposit and borrow stablecoins such as DAI, USDC, and USDT, mainstream cryptocurrencies such as ETH, WBTC, and WSTETH, or Layer2 representative ARB. On the BSC chain, supported assets include stablecoins BUSD, USDC, and USDT, as well as mainstream cryptocurrencies ETH and BTCB, and other class tokens such as BNB. Users can participate in Radiant lending market with cross-chain deposit and borrowing.

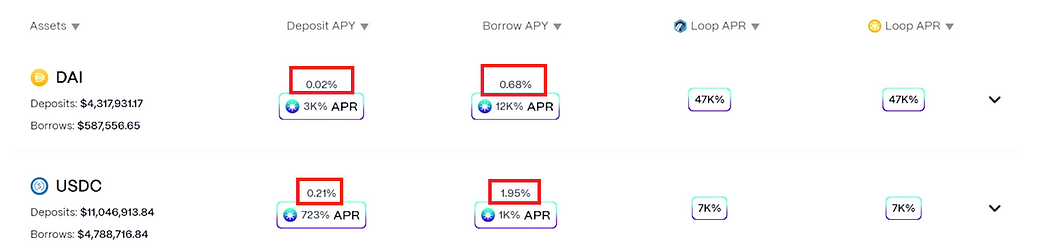

Radiant UI

Radiant market provides two interest rates, as shown in the figure, the red refers to the APY that the market lends and borrows to users, calculated based on the underlying assets, and the purple box APR refers to the reward of Radiant native utility token $RDNT, which forms an annual interest rate to users providing liquidity and loan users. Currently, higher borrowing rates are compensated by high $RDNT rewards, which attract many users.

4.1 Business composition

4.1.1 Lending

Deposit : Deposit in the Radiant lending pool, earn interest, and obtain additional value through $RDNT revenue. Deposits can be used as collateral, and depositors can withdraw their assets to the specified chain. rTokens are interest-bearing tokens, such as rUSDC, which are minted and destroyed when deposited and withdrawn. Interest will be directly distributed to rTokens holders.

Loan : Radiant increases utility for users through borrowing. Users who do not want to sell their assets can use them as collateral for loans to obtain additional liquidity. Borrowers need to pay loan fees and interest to Radiant DAO and liquidity providers. Borrowers with a health factor below 1 will cause liquidation.

Liquidation : Radiant’s liquidation procedure ensures that the borrower’s debt is not lower than the value of the collateral. When the borrower’s health factor drops to 1 or below, they will be liquidated. The overall punishment factor for liquidation is 15%.

Cycle Loans and Locking: The cycle and lock functions enable users with a health factor greater than 1.11 to increase the value of their collateral through automatic multiple deposit and borrowing cycles. The function also borrows ETH automatically and transfers it to a locked dLP position to meet the 5% dLP requirement for activating RDNT issuance. 1-Click Loop provides users with a simpler way to gradually increase liquidity and achieve higher returns with up to 5x leverage.

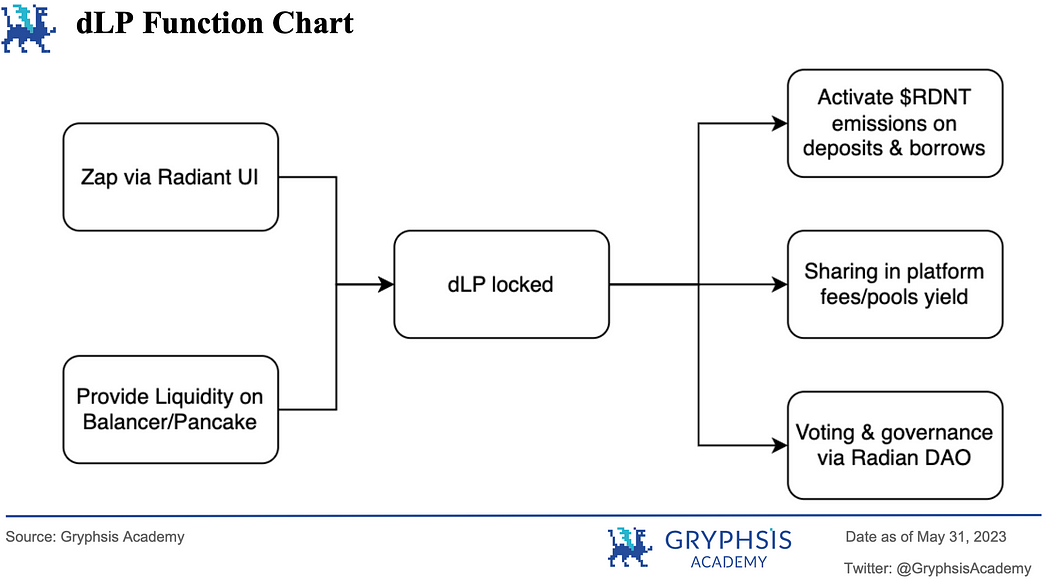

4.1.2 Liquidity Mining

Investors in Radiant Capital can earn profits by locking and vesting RDNT tokens. Dynamic Liquidity Providers (dLPs) are RDNT liquidity provider tokens. Radiant allows users to provide liquidity using the zap feature.

There are two forms of dLP trading pairs available:

-

Arbitrum: Balancer 80/20 composition (80% RDNT & 20% ETH)

-

BSC: Blockingncakeswap 50/50 (50% RDNT & 50% BNB)

Locked dLPs receive platform income allocation through rTokens (interest-bearing tokens), which users can withdraw as income or use as collateral. The platform determines the split of interest payments and liquidation fees based on dlp holdings. Users must lock at least 5% of the deposit value in USD of dLP to be eligible for RDNT reward distribution on borrowing and depositing. The vesting lock-up period for RDNT has recently been increased from 28 days to 90 days, with penalties for early withdrawal, and early withdrawal users can receive 10% to 75% RDNT rewards. The distribution of $RDNT incentives ecosystem participants to act as dynamic liquidity providers (dLPs) to provide utility to the platform.

4.1.3 Cross-Chain Bridge

RDNT OFT Bridge: $RDNT is an OFT-20 token. Layer Zero Labs’ Layer-0 Universal Interoperable Token (OFT) interoperability solution enables native cross-chain token transfers. OFT allows for combinations across multiple blockchains, eliminating fragmented liquidity, smart contract, or finality risks, and avoiding custodial risks of reporting specific tokens.

Radiant-Stargate Bridge: Radiant Capital offers users lending and bridging capabilities through the Stargate router. The bridge allows for the transfer of underlying assets between unified liquidity pools, using the Delta (∆) algorithm based on Layer Zero. Radiant V1 allows users to deposit assets on the root chain (Arbitrum) and borrow assets on any EVM chain supported by Stargate Finance. Radiant V2 supports depositing assets on both Arbitrum and BSC chains and borrowing on any EVM chain supported by Stargate Finance. Radiant is currently undergoing development testing and plans to offer full chain deposit and borrowing functionality in the near future.

4.2 Code Implementation Logic

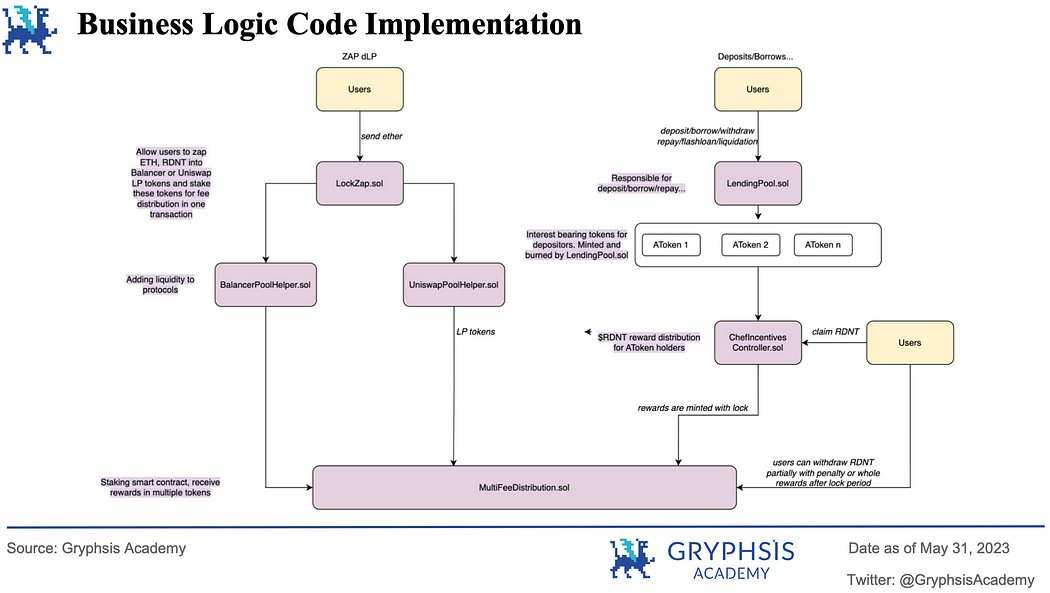

4.2.1 Business Logic Implementation Diagram

The main functions of the Radiant app are Zap (locking dLP) and lending/borrowing.

-

Users zap dLP tokens and deposit them into Balancer or Uniswap, obtaining corresponding staking rewards through MultiFeeDesitrbutions.sol.

-

Users interact with the lending pool named LendingPool.sol for actions such as depositing, borrowing, withdrawing, repaying, flash loans, and liquidation, with interaction resulting in the burning/minting of ATokens. ChefIncentiveController.sol calculates user balances and rewards, while MultiFeeDistribution.sol distributes rewards to users.

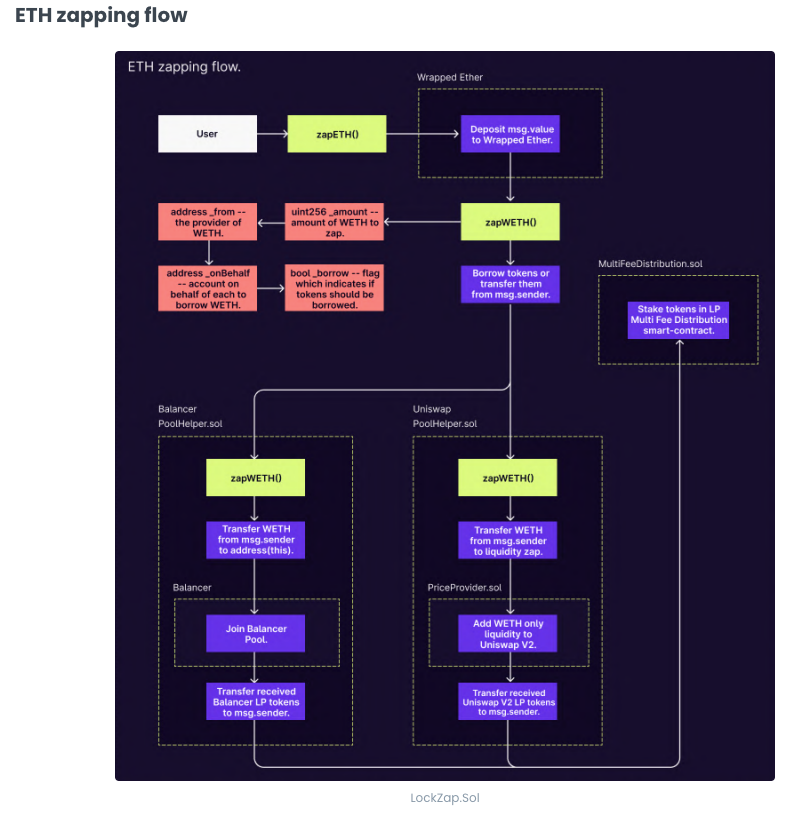

Below are details on the Zapping and One-Click Recycle process. If only one type of cryptographic asset is provided, the system will automatically borrow another asset and pair it with the provided asset in the Uniswap or Balancer pool.

Source: Radiant Capital

4.2.2 Cross-Chain Implementation

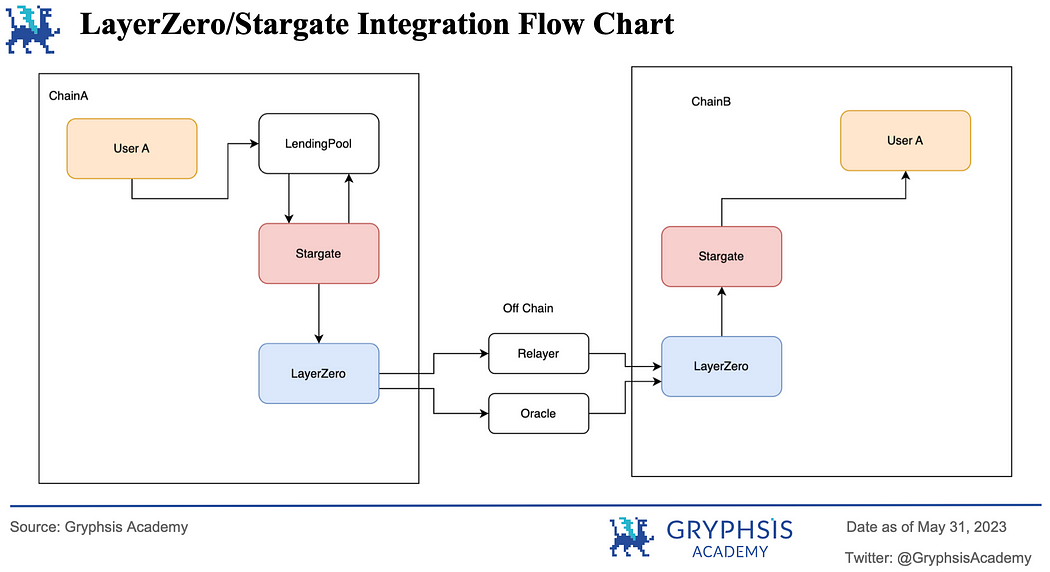

Radiant connects with LayerZero and utilizes Stargate’s reliable router interface, giving users the ability to deposit any token on Arbitrum and borrow on the same chain, or borrow on a single interface and transfer to another chain.

LayerZero : LayerZero is a universal chain that enables different blockchain networks to communicate and operate seamlessly. Radiant Capital accomplishes its goal of supporting fast and secure trading of a variety of digital assets through a currency market based on LayerZero.

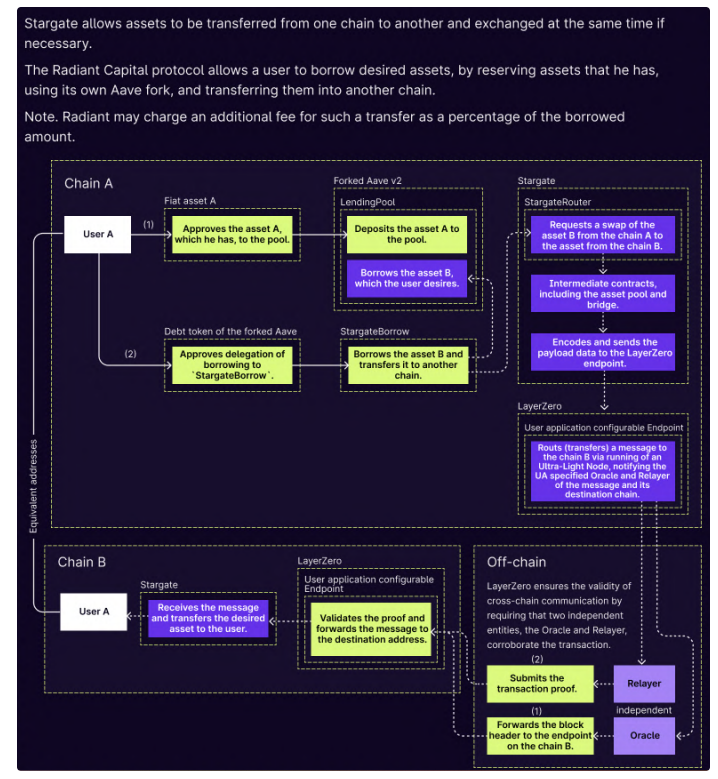

LayerZero achieves cross-chain communication by deploying LayerZero endpoints on different chains, facilitating message transmission through Relayers and Oracles. When a User Application (UA) sends a message from Chain A to Chain B, it notifies the designated Oracle and Relayer via Chain A’s endpoint. The Oracle sends the block header to Chain B’s endpoint, while the Relayer submits the transaction proof. Once validated on the destination chain, the message is forwarded to the designated address. In summary, the Oracle verifies the message on Chain A, while the Relayer checks the transaction proof, ensuring successful submission from Chain A to Chain B when both Oracle and Relayer have the same message.

Source: Blocktempo

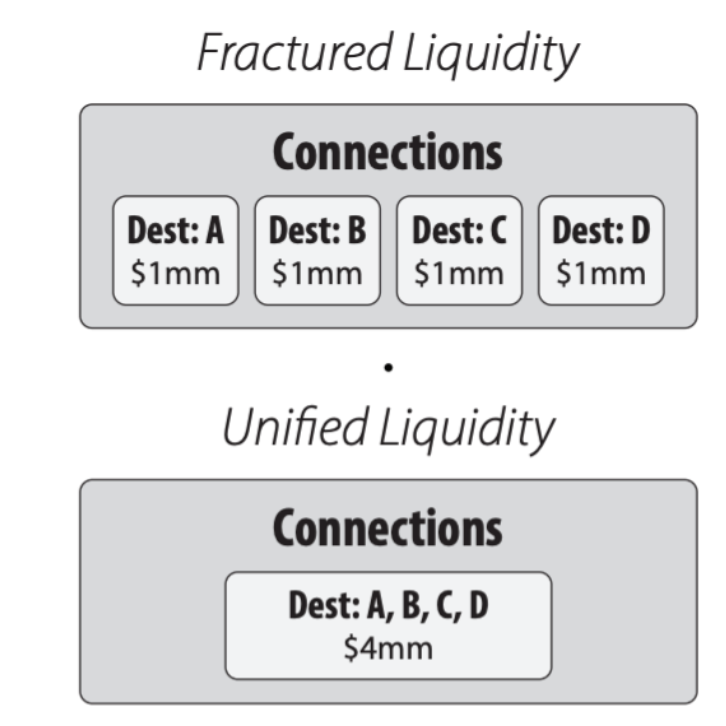

Stargate : The Stargate bridge utilizes a cross-chain shared liquidity pool, ensuring sufficient liquidity, preventing transaction reversals, and ensuring instant finality. Supported by the ∆ algorithm, the liquidity pool is automatically rebalanced to support the ∆ bridge. For example, when exchanging USDT with USDC on Ethereum, the user deposits USDT into a single USDT liquidity pool on Ethereum and receives USDC from a single USDC liquidity pool on Polygon. The ∆ algorithm seamlessly rebalances these two pools across chains to maintain balance between the deposited and withdrawn amounts. Stargate avoids maintaining separate liquidity pools for each cross-chain connection by adopting a single, unified liquidity pool for each asset on all supported chains.

Source: Consensys

Radiant Integration: Below is a simplified flowchart illustrating how assets are cross-chain borrowed and lent through LayerZero and Stargate.

Users initiate borrowing or depositing and interact with the borrowing pool. When assets are cross-chain borrowed, StargateBorrow is called and the asset is reserved in Stargate’s unified liquidity pool. Stargate sends messages cross-chain through LayerZero Endpoints, and oracles and relayers off-chain verify these messages. The detailed flowchart is shown below:

Source: Radiant Capital

5. Decentralized Lending Market

5.1 DeFi Lending

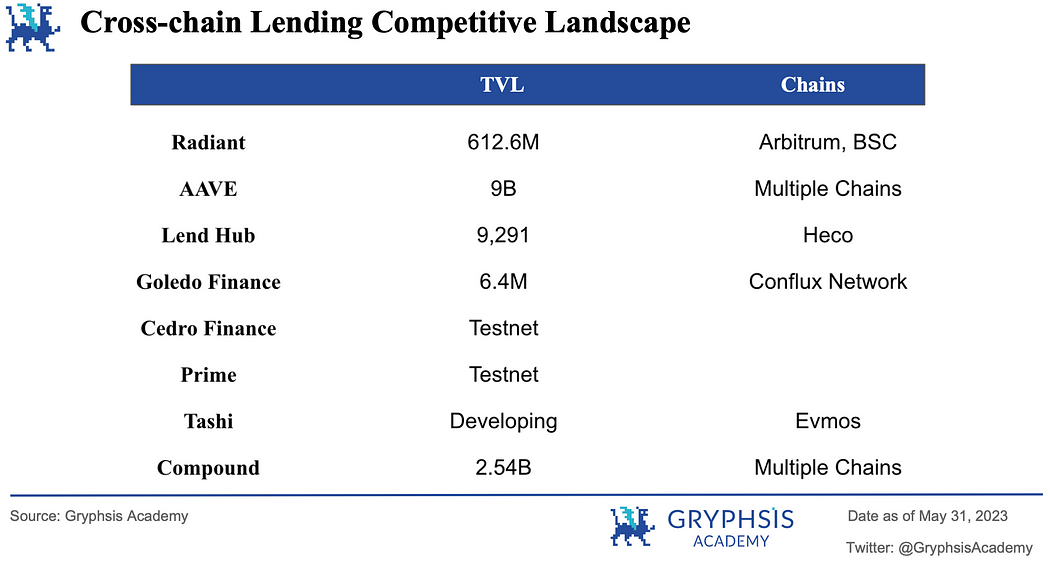

The lending industry is an important part of the decentralized finance (DeFi) sector and is the third in total value locked (TVL) after DEXes (decentralized exchange industry) and Liquid Staking. The competition in the lending sector is fierce, with over 200 protocols vying for market share. Currently, top lending protocols include AAVE, JustLend, Compound, Venus, Morpho, and Radiant.

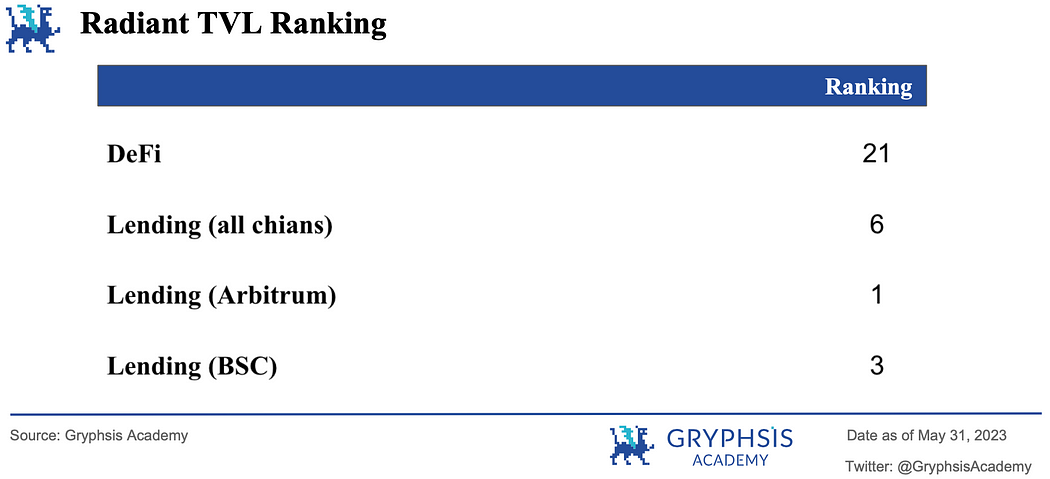

Radiant stands out as a leader in the Arbitrum and BSC smart chain ecosystems. Radiant landed on the Arbitrum chain last year and has already surpassed AAVE in TVL on the Arbitrum chain. On the BSC chain, Radiant launched in March 2023 and quickly rose to third place in terms of TVL. These achievements highlight Radiant’s strong performance on both platforms and its increasingly prominent position in the lending sector.

5.2 Cross-Chain Lending

Radiant is the first full-stack lending and flash loan protocol built on Layer Zero. With few competitors in the cross-chain lending market currently, Radiant is leading the way in cross-chain lending. As it continues to support more chains and assets in the future, Radiant has the potential to gain more liquidity and users.

As mentioned earlier, what sets Radiant apart from other lending protocols is its ability to allow users to deposit collateral on one chain and borrow on another. Radiant’s cross-chain functionality is achieved through Stargate’s cross-chain router, which allows users to deposit assets on Arbitrum and borrow on any EVM chain supported by Stargate. In contrast, AAVE’s assets currently cannot be borrowed across different chains, resulting in scattered liquidity and limited asset utilization. The flourishing of Layer 2 has brought about an indispensable demand for cross-chain asset interaction. Radiant uses LayerZero’s Omnichain technology to establish interoperability between its full-stack, providing a good solution to the problem of liquidity fragmentation across different chains.

Radiant Capital holds a relative liquidity position in the decentralized lending market. Its dLP “Dynamic Liquidity Provision Mechanism” dynamically adjusts their mining increment rewards based on the provided liquidity ratio, incentivizing both lenders and borrowers on the platform. This locks in a certain amount of RDNT in the market and enhances liquidity, achieving long-term development. In addition, Radiant Capital has a first-mover advantage in full-stack lending , which other lending protocols such as AAVE cannot imitate or surpass in the short term.

6. Token Economics

6.1 Token Distribution

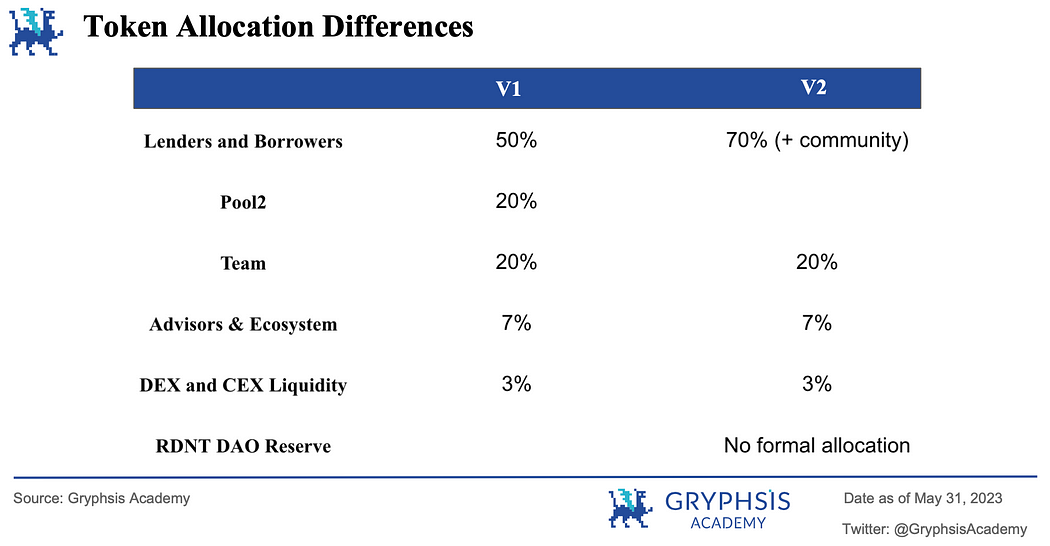

The total supply of RDNT tokens is 1,000,000,000.

-

54% is allocated as incentives for suppliers and borrowers and will be released over five years.

-

20% is allocated to the team and will be released over five years, with a three-month cliff (10% of which is locked at protocol inception and unlocks after three months).

-

14% is allocated to the Radiant DAO reserve.

-

7% is allocated to core contributors and advisors and will be released over one and a half years.

-

3% is reserved for Treasury & LP.

-

2% is allocated to Pool 2 liquidity providers between August 3, 2022, and March 17, 2023, which has been deprecated pending approval of governance proposal RFP-8.

6.2 RDNT Token Unlocking Schedule

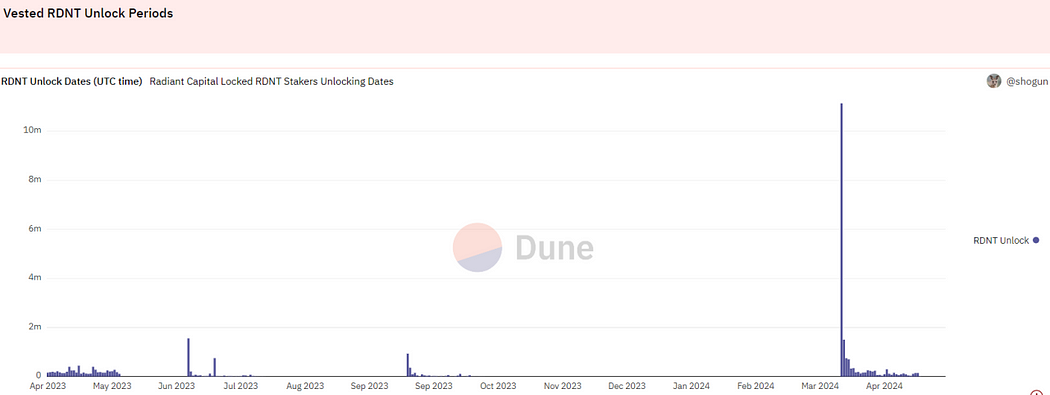

RDNT Token Unlock Schedule after issuance is shown in the above figure. On July 24, 2022, a significant token unlocking and distribution occurred in the Radiant ecosystem. The Treasury unlocked 30 million RDNT tokens, and DAO Reserve unlocked 140 million RDNT tokens. Then, 70 million RDNT tokens were allocated to core contributors and advisors, gradually released over 18 months. Additionally, 540 million RDNT tokens were allocated to supply and borrower incentives, released over 60 months. Pool 2 was incentivized with 20 million RDNT tokens, to be released in 8 months. The remaining locked tokens will be gradually released in the future, until all are unlocked in July 2027. These unlock and distribution events shape the RDNT token distribution model, incentivize participants, and affect liquidity within the Radiant ecosystem, ensuring fair distribution and sustainable growth of the tokens. This phased approach is in line with the project’s long-term vision, promoting stability and planning for token holders and ecosystem participants.

The following chart clearly shows the time when currently vested RDNT tokens will be unlocked. In March 2024, over 10 million RDNT will be unlocked. This unlocking event may affect the circulation of the tokens and have some impact on market dynamics during this period. Investors should pay attention to such milestone events and consider the potential impact on the value and trading of RDNT tokens.

Source: Dune Analytics (@shogun)

6.3 Comparison of Token Release Rules Design for Proposed (V1 vs V2)

Radiant v1 Design:

All token releases are directed towards the initial deployment of RDNT on Arbitrum. Proposed design for Radiant v2: Total Max Emissions represents the total amount of release allocated to all Radiant deployments in a given month; the maximum total emission will run according to the proposed schedule and end in July 2027. At the end of each month, the DAO will review the total locked value (TVL) for each chain and allocate the release accordingly for the next month. For example, if the Radiant total locked value on the Arbitrum chain is 30%, BNB chain is 30%, and Eth Mainnet is 20% at the end of March, then the release for these three chains should be allocated as 30%/30%/20% respectively for the next month. At the start of the project, 100% of the token release was directed to the Arbitrum Radiant market; after launching on the BSC Chain, the proposal suggests that the first month’s release of 50% be directed to the BNB Chain. This is a simple method, and more complex ideas (such as metrics for each chain and market, distribution based on generated protocol fees) should continue to be discussed and brought into subsequent proposals. This part of the RFP can be updated based on subsequent proposals generated by DAO stakeholders. This is a predictable and formulaic method that can provide transparency in the short term. As a result of the vote on Governance Proposal RFP-4, the release rules for $RDNT incentivize ecosystem participants to provide utility to the platform as dynamic liquidity providers (dLPs). Only users who have locked dLP (liquidity token) are eligible for RDNT token release rewards for activating their deposits or borrowings.

Given Radiant’s cross-chain vision and the transition from unilateral locking to LP locking, this allows Radiant to plan for a long-term future more reasonably and provides the possibility for more chain deployments.

6.4 Smart Contract Revenue Path, Value Acquisition, and Token Utility

6.4.1 Smart Contract Revenue Path

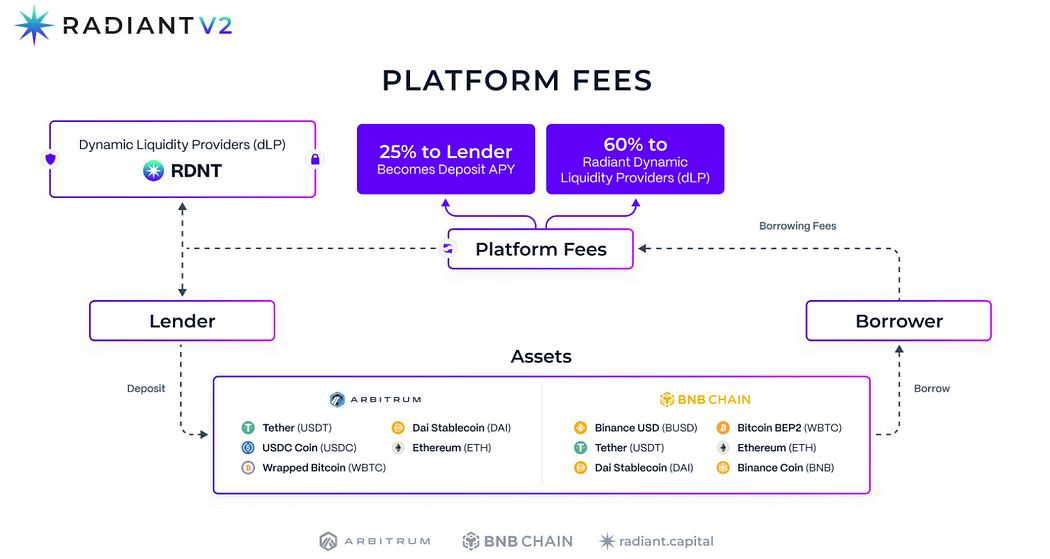

The revenue of this contract comes mainly from borrowing interest and loan fees. This process involves lenders depositing their assets on the platform, which are then borrowed by borrowers with collateral. Borrowers need to pay a borrowing fee to obtain the loan. If the borrower fails to repay the loan according to the agreed terms and conditions, the assets used as collateral may be liquidated. The platform then collects fees from these transactions and distributes rewards to lenders and dynamic liquidity providers. This revenue model incentivizes user participation and provides a revenue mechanism for the platform and its participants.

6.4.2 Platform Value Acquisition

-

Borrowing Interest, the interest rate fluctuates according to the dynamic change of liquid capital

-

Liquidation fee

-

Prepayment penalty

Revenue & Fee Blockingth, Source: Radiant Capital

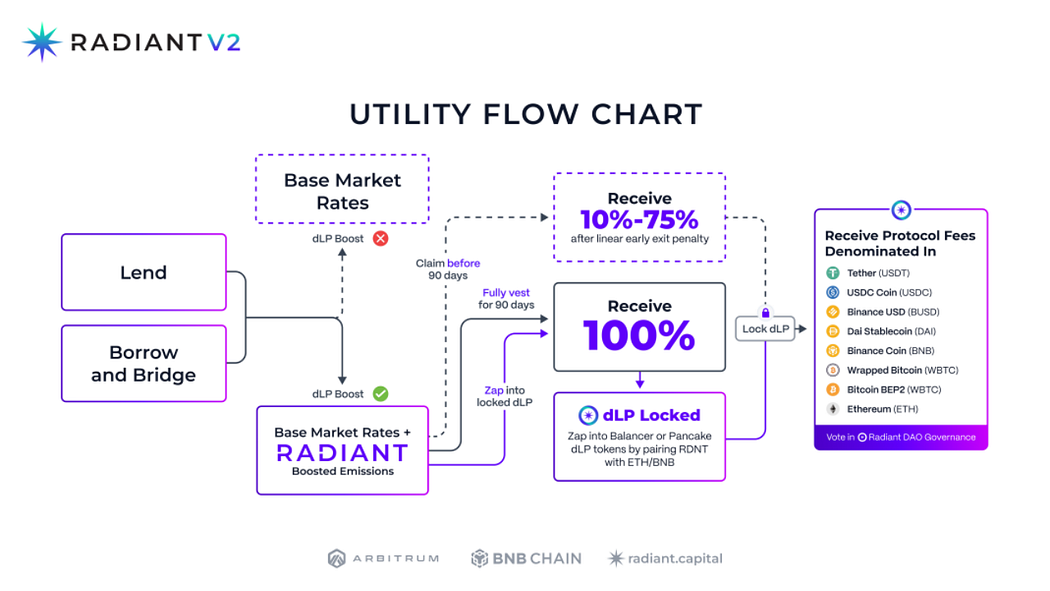

6.4.3 $RDNT Token Utility

-

Activate RDNT token release for borrowers/lenders with a minimum of 5% deposit dLP, which is additional value besides the basic market rate

-

dLP lockers earn 60% of platform fees

-

RDNT holders can also participate in DAO governance

Utility Flow Chart, Source: Radiant Capital

Sustainability is an important key performance indicator of Radiant DAO. Therefore, the protocol has implemented a dynamic liquidity (dLP) mechanism, which only allows the rewarded RDNT tokens and platform fees to be allocated to dynamic liquidity providers (dLP). As mentioned above, the dLP mechanism is a good improvement compared to Radiant v1. It incentivizes users to provide liquidity for $RDNT, with a 90-day lock-up period before fully receiving RDNT token release incentives, and early withdrawal will be penalized, which can reduce the selling pressure of the token.

7. Operational Status and Competitive Landscape

7.1 TVL

Radiant has the highest TVL on the Arbitrum chain. Its TVL is higher than other similar market cap lending protocols due to its easy-to-use locking and looping features and high incentivized rewards. However, its MCap/TVL ratio is higher than its peers, indicating that its current valuation is slightly high.

7.2 Users

Since the launch of V1, there have been two waves of user growth during the Arbitrum hype in Q3 2022 and January, but there has not been a significant increase in users after the release of Radiant V2. The current cumulative number of users is 216,831, and the daily active users are 4,750.

Source: Dune Analytics (@defimochi)

7.3 Trading Volume

$RDNT incentivizes trading volume for borrowers and lenders, reflecting its ability to drive engagement and activity on the platform. In May, the trading volume was $740.7 million, and Radiant Capital’s trading volume exceeded lending protocols with similar market caps, indicating that Radiant is effectively attracting users and spurring a lot of trading activity.

7.4 Utilization

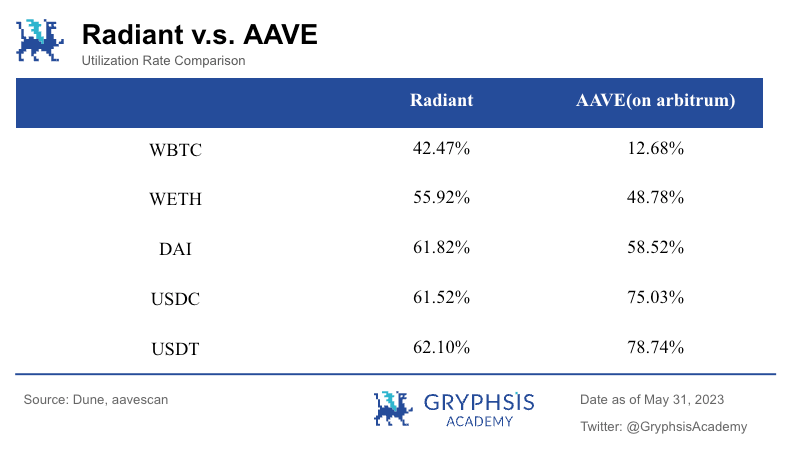

The total utilization rate is approximately 60%, which is relatively high compared to similar lending protocols. RDNT rewards and easy user interface for looping and locking increase asset utilization. Segmented by each asset, Radiant’s utilization in stablecoins is similar to AAVE, but its utilization in wbtc and weth is higher.

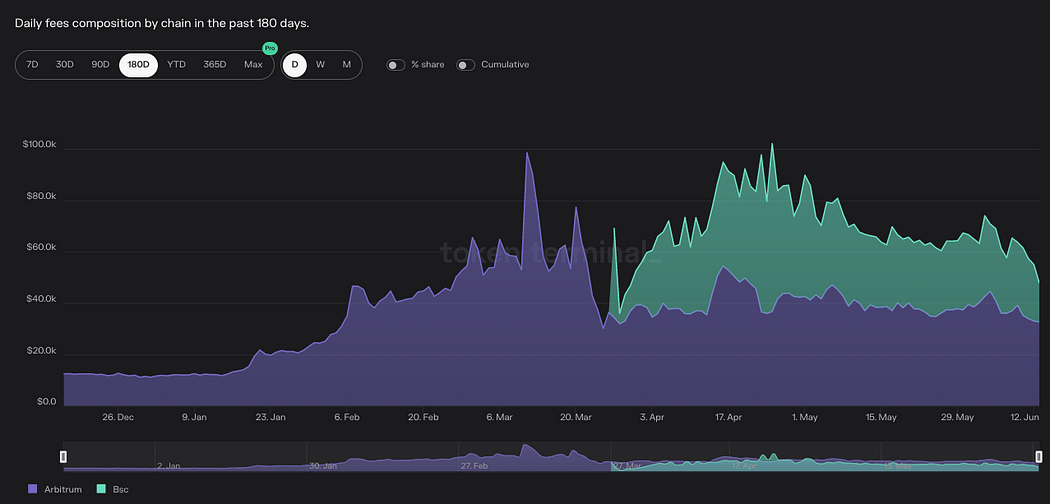

Radiant launched on the Binance Smart Chain (BSC chain) on March 27th, locking in more than $33 million. The green area in the figure below shows the income that RDNT has obtained from the BSC chain since March 27th, and the purple part shows the income that RDNT has obtained from the ARB chain. Obviously, starting from mid-April, the income that RDNT obtained from the BSC chain was higher than that obtained from the ARB chain. In the past 90 days, revenue has increased by 115.9%, achieving a significant increase in revenue. In terms of 90-day revenue, it even surpasses well-known protocols such as AAVE and Compound, making it even larger. This indicates that Radiant is experiencing rapid expansion and gaining traction in the industry.

Source: Token Terminal

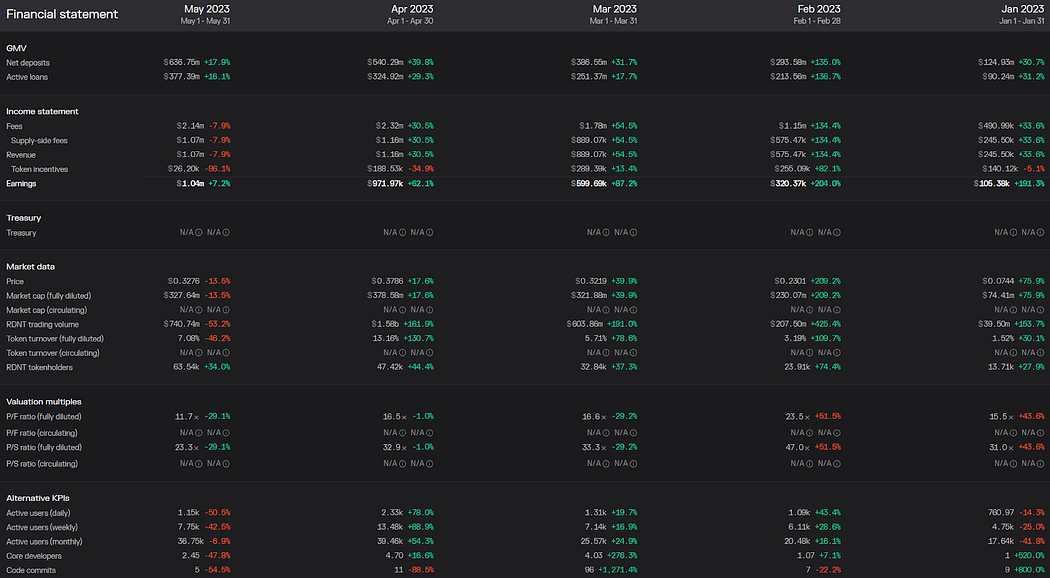

7.5 Financial Statement Analysis

According to the financial report statistics, RDNT’s revenue and transaction volume have both seen significant growth over the past several months. In January and May, RDNT’s revenue was 105.38 thousand dollars and 1.04 million dollars, respectively, representing an increase of 886.90%. In January and May, RDNT’s transaction volume was $39.5 million and $740.74 million, respectively, indicating that RDNT’s performance is rapidly improving. The increase in revenue and transaction volume indicates that the demand for the protocol continues to grow. As of May 31, 2023, the platform’s active loans were $377.39 million and net deposits were $636.75 million. The total net deposit of $636.75 million indicates that the platform has a large amount of liquidity, which is an important factor in maintaining user trust and ensuring that the platform can meet user borrowing and lending needs. In addition, the $377.39 million in active loans means that users are highly engaged with the platform, which is a positive signal for the platform’s growth prospects. Additionally, the stable loan-to-deposit ratio indicates that the platform is effectively managing its borrowing and lending activities and maintaining a healthy balance between them.

Source: Token Terminal (Date as of May 31, 2023)

Overall, the financial statements show that RDNT’s financial condition is good, providing a solid foundation for continuing to expand its user base and expand its decentralized lending market services.

8. Growth Drivers

8.1 Development of Layer2

The prosperity of Layer2 is driving the development of the RDNT protocol. As more and more users and transactions migrate to Layer2, the demand for RDNT’s decentralized lending services will increase. Radiant’s plans to launch on Ethereum and zkSync also demonstrate its commitment to capturing this growth market.

8.2 Cross-Chain Market

Radiant is the first functional cross-chain lending market. Given the frequent occurrence of cross-chain bridge theft and hacking events, cross-chain lending provides a promising alternative that can alleviate the demand for traditional cross-chain bridges. If the protocol successfully achieves full cross-chain lending, it will enhance the utility and demand for RDNT, ultimately driving up its price. Radiant is at the forefront of the cross-chain lending market and has the potential to reshape cross-chain transactions and solidify Radiant’s value proposition.

8.3 Passive Income

Users can earn low-risk passive income by lending/borrowing across chains during a bear market.

8.4 Token Design

The token design of V2’s token economic model enhances incentive value by allocating RDNT issuance to long-term protocol users to promote its sustainability. The “5% locked dlp” threshold incentivizes users to purchase RDNT and re-lock more LP to maintain above the minimum threshold.

8.5 Airdrop Opportunities

Radiant plans to airdrop $ARB to long-term dlp holders. In addition, the descriptions of LayerZero and ZKSync attract users to the Radiant platform to potentially receive airdrops.

9. Valuation

Our valuation is based on the DCF analysis and comparable analysis methods, both of which can be adjusted accordingly in our valuation model (Radiant Capital Valuation Model – Gryphsis Academy). The following is a detailed description and explanation of the valuation methods.

9.1 Cash Flow Analysis

Discounted cash flow (DCF) is a valuation method used to estimate the value of an asset based on its expected future cash flows. The principle is that the value of an investment today must equal the cash it generates in the future. Our model uses a 5-year forecast period and accounts for any cash flows after that with an estimated terminal value.

9.1.1 Assumptions

Protocol Total Locked Value (TVL) Growth Rate: We divide the assets available for lending into three categories: BTC and ETH, stablecoins, and L1 and L2 alternative assets, and assume the growth rate for each asset category under low, medium, and high scenarios.

We used the historical annual growth rate of the past five years to predict the market value of Microsoft and gold, and used the market value of Ethereum as a percentage of Microsoft’s market value, and the market value of Bitcoin as a percentage of gold’s market value to demonstrate whether the growth rate estimates under high, medium, and low scenarios are reasonable. We assumed that the growth rate is linearly decreasing. Since Radiant has supported BSC and provided BNB borrowing and lending in the market, the TVL of Alt L1/L2 assets has grown by 231.53% in the next month. Therefore, it is reasonable to assume that L1 and L2 alternative assets have a higher growth rate compared to stablecoins and BTC/ETH.

Utilization: In Radiant v1 and Radiant v2, the asset utilization rate has remained at similar levels. We rounded the average and chose a utilization rate of 73% for stablecoins, and lowered the estimated utilization rates for BTC, ETH, Alt L1, and L2 to 50% to accommodate market uncertainties.

Annual cost/lending asset: We compared this ratio with AAVE (a relatively mature lending protocol) and calculated the average annual cost/lending asset for both protocols. We compared this rate with the current annual rate of Radiant and selected the minimum of the two rates as the final year rate for 2028. The proportion for the remaining years is calculated by linearly increasing the rate to the final year rate.

Discount rate: We used the 10-year US Treasury bond as the risk-free rate and BTC as the market benchmark. The beta value is obtained from a regression model of RNDT returns as a function of BTC returns. The regression analysis is based on data from the RDNT IDO day, which is July 22, 2022. The capital asset pricing model (CAPM) calculates a capital cost rate of 35%. Regression analysis shows that Bitcoin returns significantly predict RDNT prices, but the model can only explain 1.7% of the total variance. Therefore, we choose 35% as the discount rate, which is similar to the average return rate of venture capital funds of 30%.

When conducting comparability analysis, it is essential to select companies that are as similar as possible in terms of industry, business model, risk status, and market dynamics. By ensuring comparability in these aspects, the influence of external factors is reduced, allowing us to focus on the intrinsic value drivers of the analyzed companies. If the comparable companies we choose belong to the decentralized lending industry and have similar business nature and risk status as RDNT, this can enhance the effectiveness of comparative analysis. By taking decentralized exchange (DEX) lending protocols as comparable protocols within the DEX industry, the problem of different market risks between different industries can be solved. As these four comparable items all belong to the DEX lending industry within the decentralized financial market, it can be reasonably assumed that they face similar market risks.

9.2.1 Valuation Assumptions and Variable Considerations

Fully Diluted Valuation / TVL Ratio: This ratio reflects the market’s sentiment and view of the protocol’s value by comparing the market value with the total locked value (TVL). It provides investors with insights into the corresponding valuation of assets and economic activities generated by the protocol. Secondly, TVL represents the total value of locked assets, and by dividing market value by TVL, it can give an efficiency indicator of the protocol compared to market value in attracting and retaining assets. A lower P/TVL ratio indicates potential undervaluation and strong growth prospects. Considering these factors, the P/TVL ratio can be a relevant and useful comparable multiplier for estimating the valuation of DeFi lending protocols.

Price/Earnings Ratio: The Price/Earnings ratio helps investors evaluate whether the market valuation of decentralized lending protocols is reasonable or whether it is overvalued or undervalued compared to their earnings potential by considering the relationship between price and earnings. This can help identify potential investment opportunities or risks.

Price/Sales Ratio: The Price/Sales ratio is commonly used to evaluate the valuation of traditional companies based on their revenue. For decentralized lending protocols, protocol fees (referred to as “sales revenue” in traditional companies) are a key factor in assessing their financial performance and sustainability. By using the Price/Sales ratio, the relationship between market value (price) and the fees generated by the protocol is considered, providing insight into how the market evaluates the income-generating ability of the protocol.

Average P/S ratio : We use the market multiplier method commonly used in the cryptocurrency industry, taking the average P/S ratio of four comparable protocols as the market multiplier 1. By calculating the average, we basically consider the upper and lower limits of comparable projects and provide a balanced market multiplier estimate. Therefore, we choose to use the average of comparable projects as a quantified market multiplier to avoid potential biases that may arise from relying solely on the maximum or minimum value.

Median : Statistically, the median is not influenced by extreme values in the distribution sequence, which to some extent improves the representativeness of the median for the distribution sequence. Therefore, we believe it is reasonable to choose the median as market multiplier 2.

Revenue and protocol fees : Analyzing the revenue generated by a protocol can evaluate its ability to generate revenue and maintain operations. Revenue is a key indicator of protocol financial health and growth potential. Evaluating protocol fees helps to understand the revenue streams directly related to lending activities and the profitability of lending protocols. Revenue and protocol fees can come from various sources within decentralized lending protocols, including interest rate spreads, liquidation fines, transaction fees, and other revenue sharing. By considering revenue and protocol fees as variables, analysts can assess the diversification of revenue streams. This helps to assess the ability of the protocol to withstand market volatility and long-term survival.

9.2.2 Valuation

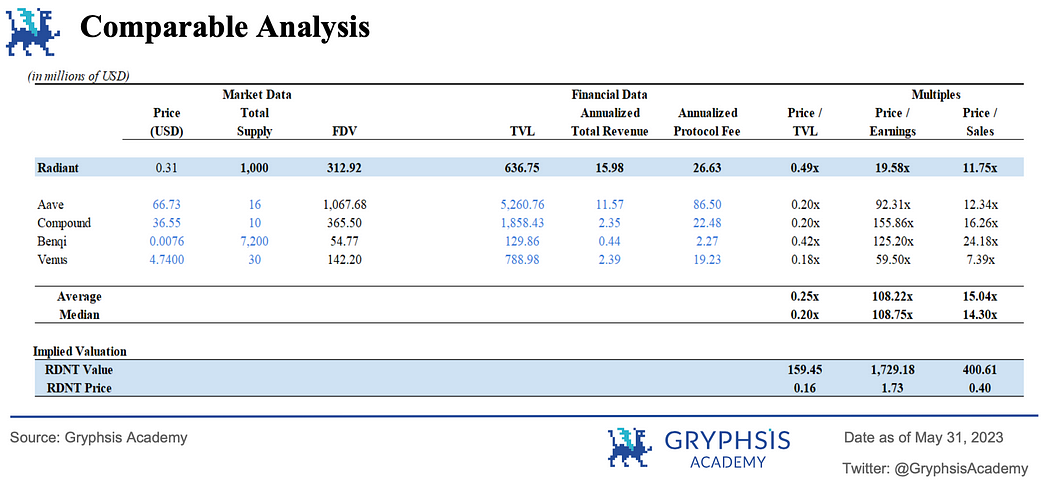

According to the figure below, Radiant’s TVL as of May 31, 2023 was $636.75 million, ranking between Benqi and Venus. The fully diluted valuation is $312.92 million, which is smaller than Aave and Compound, but larger than Benqi and Venus.

Radiant’s fully diluted valuation/TVL ratio is 0.49, which is relatively high compared to other protocols, indicating that Radiant’s valuation may be overestimated relative to its capital locked in the protocol. This may mean that the market’s pricing of Radiant may be higher than its potential value. However, Radiant’s estimated annualized total revenue is $15.98 million, and the annualized protocol fee is $26.63 million, which proves that Radiant has good revenue generating ability. In addition, the price-to-earnings ratio (P/E) and price-to-sales ratio (P/S) are relatively low compared to the average ratios of the selected decentralized lending protocols, indicating that there may be potential for undervaluation. Finally, based on these three valuation multipliers, potential prices for RDNT are derived to be $0.16, $0.40, and $1.73, respectively.

Note that the establishment and derivation of the valuation model and token price is based on the current data and market conditions provided. The actual market dynamics and performance of the Radiant protocol in the future will ultimately determine its true market value.

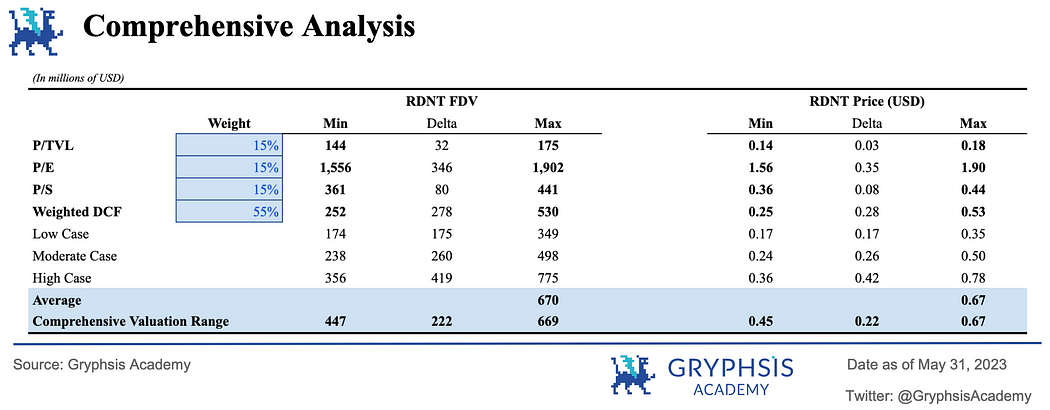

9.3 Comprehensive Analysis

Finally, we conducted sensitivity analysis and obtained the final valuation range.

For comparative analysis, we selected three values, P/TVL, P/E, and P/S ratios. At the same time, we selected the maximum and minimum probability-weighted DCF valuations (cash flow valuations) under different terminal P/E and discount rates from the sensitivity analysis. Based on the above data, the weightings of the three comparative analysis multiples are 15%, and the weighted DCF is 55%. The price range obtained from comprehensive analysis is $0.45-$0.67.

10. Risks

10.1 Smart Contract Risk

Although the Radiant v2 smart contract has been audited by well-known companies such as BlockSecTeam, Peckshield, and Zokyo_io, and is pending review by OpenZeppelin, there are still inherent smart contract risks. In addition, the reliance on external components such as Stargate and LayerZero introduces potential additional risks. As Radiant will be launched in 2022 and the maturity period is less than one year, there may be some technical risks due to the lack of long-term testing.

10.2 Inflation risk

Radiant faces high inflation rates, which could potentially impact the value and purchasing power of the native token, or affect the overall stability and sustainability of the lending ecosystem.

10.3 Competition risk

There is a large number of competitors in the lending space where Radiant operates, and the existence of more mature lending protocols that support cross-chain lending further increases the competition, which could impact the growth and user base of the Radiant protocol. For Radiant, being able to provide unique value is crucial in attracting users and maintaining market share.

10.4 Governance risk

Radiant is governed by Radiant DAO, which makes the protocol vulnerable to potential governance-related risks. This includes potential challenges in quickly implementing change proposals or responding to market demands, as well as vulnerabilities to governance attacks or manipulation. Sound governance procedures and transparency are crucial in mitigating these risks and ensuring the long-term success and stability of the protocol.

Potential investors and users should be aware of these risks and conduct their own due diligence. Evaluating and understanding the relevant risks of decentralized lending protocols like Radiant is especially important for making informed investment decisions and risk management.

11. Conclusion

Recently, Radiant has demonstrated an impressive performance in the cross-chain lending space. However, there is still a long way to go to achieve a fully-chain currency market. Depending heavily on Stargate and LayerZero to achieve the goal of cross-chain may limit its development. Radiant can further develop by integrating more omnichain technology solutions to optimize the user experience.

In addition, Radiant can further expand its business lines in the currency market, not just limited to lending. Some possible ways to improve the protocol:

-

Risk management framework: One of the challenges faced by decentralized lending protocols is the lack of diversified collateral and corresponding mature risk management frameworks. Implementing a strong risk management framework can help mitigate a range of risks, and Radiant can improve the overall stability of the protocol by continuously improving dynamic collateral ratios, liquidation penalties, and risk-based interest rates.

-

Inclusion of more asset types: Decentralized lending protocols currently primarily support cryptocurrencies as collateral. However, incorporating more asset types, such as real-world assets and LSD, can help increase the diversity of the currency market and attract new users who may not be accustomed to cryptocurrencies.

-

Integration with other DeFi protocols: Radiant lending protocols can also integrate with other DeFi protocols such as decentralized exchanges, yield aggregators, etc., to create a more comprehensive financial ecosystem.

-

Expansion of other Defi products: Radiant Capital can explore opportunities beyond lending and use its omnichain capabilities to expand its business to other DeFi products, such as LSD and collateral debt positions (CDP), to increase a wider range of token utility use cases. Leveraging the advantages of its RDNT’s OFT-20 token standard to create more token scenarios and achieve seamless cross-chain token transfers, making it easier for users to exchange and use any dApp on any chain, thereby attracting more users to the platform. As Radiant gradually integrates more cross-chain currency market businesses, it can create more empowering scenarios for its tokens and become a financial platform with a variety of DeFi products. With the improvement of the platform’s value and user experience, it can help boost the price of the token.

Overall, RDNT’s future prospects are bright, with many opportunities for growth and innovation. By implementing a robust risk management framework, incorporating new asset types, and integrating with other DeFi protocols to expand into more DeFi yield farming applications, Radiant Capital can continue to thrive and attract new users to its all-chain currency market.

Like what you're reading? Subscribe to our top stories.

We will continue to update Gambling Chain; if you have any questions or suggestions, please contact us!