Why now?

As early as 2018, STO (Security Token Offering), a subset of RWA, had caused a frenzy in the market, but it ended up with nothing. Today, the narrative of RWA is gradually heating up. Why is this time point? What is the driving force behind the development of the track?

- From the perspective of infrastructure: the DeFi infrastructure is gradually improving. Relevant token standards, oracles, and peripheral development tools are more complete and have the ability to connect on-chain and off-chain;

- From the perspective of assets and income: Web3 native assets have reached a bottleneck, and assets are basically homogenized; in the bear market, on-chain activities are low and there is a lack of stable sources of income native to Web3;

- From the perspective of narrative: After CeFi’s bankruptcy, investors are more concerned about risk control and compliance; the traditional financial industry is highly compliant, and RWA assets provide investors with more protection compared to Web3 native assets;

- From the perspective of regulation and law: Regulation is constantly expanding its boundaries, and laws and regulations related to cryptocurrencies are gradually improving;

In the last round of market, RWA platforms with similar models have taken shape, such as Maple Finance, Clearpool, TrueFi, etc. The basic mode of these platforms is to open up lending capital pools for some institutions through community governance. Users invest in capital pools to obtain pre-agreed interest rates. Institutions can use the funds for relevant investment operations and pay interest and principal back according to the agreement. However, early RWA platforms lacked compliance procedures and risk management. After the Luna and FTX incidents, some borrowers went bankrupt and were unable to repay the borrowed assets, resulting in serious losses to investors.

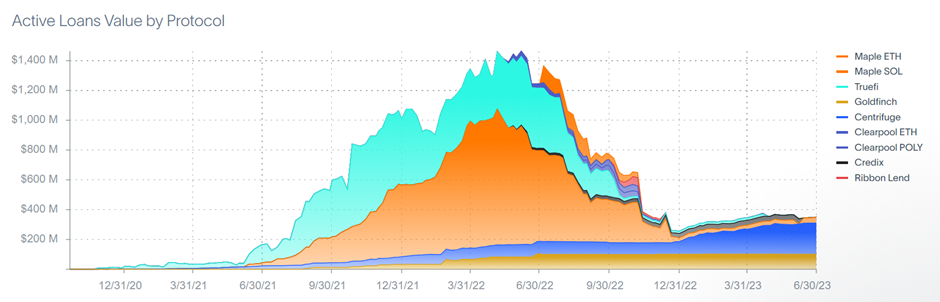

Figure 1: Active loan amount of RWA lending agreement, source: rwa.xyz, data as of July 6, 2023

From the above figure, it can be seen that before the Luna incident in 2022, the amount of loans reached its peak, and the amount of loans decreased sharply thereafter. In the second half of 2022, due to the Luna and FTX incidents, Clearpool and TPS Capital suffered the heaviest losses, both of which had major mistakes in their compliance procedures.

- RWA.xyz: Tokenized Government Bond Industry Research Report

- The five new rising stars of LSD are coming on strong, can Lido maintain his position?

- The five newcomers of LSD are coming on strong. Can Lido still hold onto his leading position?

TPS Capital and Clearpool started cooperation in the second quarter of 2022 and opened a lending capital pool on Clearpool. TPS Capital claimed to be independent of Three Arrows Capital (which went bankrupt after the Luna incident). However, the court documents prepared by the liquidator of Three Arrows Capital showed that the two were closely related and complex, and Three Arrows Capital was actually the guarantor of TPS Capital, providing guarantees for the later defaulted loans of TPS Capital.

In June 2022, Clearpool removed TPS Capital’s lending pool, and Clearpool’s data partner X-Margin downgraded TPS Capital’s rating to B, lowering the borrowing limit to $0. Clearpool and X-Margin announced that they would work together to ensure that TPS Capital repaid the loan funds and that users did not suffer losses.

Before the avalanche, the world was quiet until the last snowflake fell. These tens of millions of dollars in losses are a heavy lesson, and they also make developers who want to participate in the RWA track pay more attention to risk control, compliance processes, and legal frameworks.

What is RWA?

RWA refers to various assets that exist outside the blockchain but can be tokenized and combined with existing DeFi protocols in a certain way. Currently, the main RWA projects are mainly concentrated in the following types: bonds, including private bonds, corporate bonds, and government bonds.

- Equity

- Real Estate

- High-value collections

- Carbon credit points

We believe that the earliest bond-type products that can enter DeFi, including government bonds and corporate bond products, are mainly demand-side adoption of RWA by DeFi protocols and Web3 protocol treasury management. According to DefiLlama data, the US bond tokenization platform (OpenEden and MatrixDock) ranks among the top two TVLs in RWA projects, followed by real estate-related RWA platforms (Tangible and RealT). However, the total volume of tens of millions of dollars is still relatively small compared to both DeFi and the entire Tradfi field, and there is huge room for growth.

Figure 2: RWA project TVL, source: DefiLlama, data as of 2023.07.10

Driving force of RWA

In general, existing DeFi protocols mainly apply RWA assets in three ways: 1) treasury fund management, some of MakerDAO’s demand for RWA comes from this; 2) used as collateral, such as MakerDAO and Solana’s stablecoin protocol UXD Protocol; and 3) introducing new asset types for DeFi scenarios, such as Curve (MatrixDock STBT) and Flux Finance (Ondo Finance OUSG).

DeFi protocols introduce RWA from multiple sources, including:

- On-chain asset management demand

- On-chain asset management seeks stable returns and good liquidity. Products in the real world, such as government bonds, are widely recognized investment targets, with relatively stable returns and very good liquidity, belonging to the category of assets with a market value of trillions of dollars.

- Alternative sources of income

- Native on-chain revenue mainly comes from Staking/Trading/Lending. When the cryptocurrency market is highly volatile, when the market is in a downturn, the decrease in on-chain financial activities will lead to a decline in revenue. For example, in the current market state, the income of mainstream on-chain platforms is even lower than that of US government bonds. If seeking alternative income that has low correlation with on-chain native assets, introducing RWA-related assets is undoubtedly a good choice.

- Diversified investment portfolio

- Chain assets have relatively single types and high correlation and volatility. Introducing more stable RWA assets that are not highly correlated with on-chain native assets can achieve hedging purposes and form richer and more effective investment portfolio strategies.

- Introduction of diversified collateral

- The high correlation of on-chain assets makes loan agreements prone to runs or large-scale liquidation, which further exacerbates market volatility; introducing RWA assets that are less correlated with on-chain assets can effectively alleviate such problems.

In this article, we will use MakerDAO as an example to analyze how DeFi protocols apply RWA (as collateral).

In-depth analysis of MakerDAO RWA application

MakerDAO is a decentralized autonomous organization (DAO) that aims to create and manage the Ethereum-based stablecoin Dai. Users lock Ethereum (ETH) as collateral to generate Dai stablecoins. The goal of Dai is to maintain a 1:1 anchor relationship with the US dollar and stabilize its value through smart contracts and algorithms. Due to the high volatility of the cryptocurrency market, a single collateral can easily lead to large-scale liquidation. Therefore, MakerDAO has been trying to diversify its collateral, and the introduction of RWA is one of the important means, even written into the Endgame plan proposed by MakerDAO Co-founder Rune Christensen.

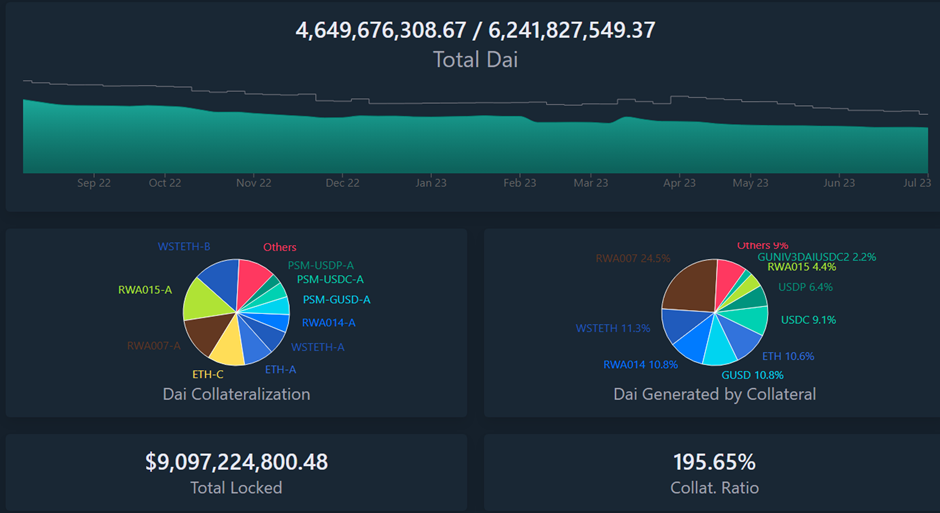

Figure 3: Current status of Dai, source: daistats.com, data as of July 10, 2023. The figure shows the current total amount of Dai (about 4.65 billion), and the upper limit set by MakerDAO is 6.2 billion. Currently, the collateral composition of Dai has achieved relatively diversified, including some RWA and various stablecoins.

Risk of a single collateral

On March 12, 2020, due to the financial crisis caused by the epidemic, the financial market collapsed, and the US stock market continued to crash. As a marginal sub-segment of the financial market, the cryptocurrency market also plummeted rapidly. As one of the top DeFi protocols on the Ethereum chain, MakerDAO also suffered a huge impact. On the one hand, due to the limited capacity of the Ethereum network and network congestion, liquidators cannot timely liquidate risk accounts; on the other hand, some borrowers of stablecoin Dai need to buy Dai to repay their debts and withdraw collateral assets, which increases the market demand for Dai and further increases the difficulty of liquidation. Under multiple factors, MakerDAO suffered bad debts of up to 5.67 million US dollars. In the end, MakerDAO had to issue an additional 20,980 MKR tokens to raise 5.3 million US dollars to make up for the bad debts.

MakerDAO Endgame plan

After experiencing such events, MakerDAO also continuously tried to diversify its collateral. The goal of the MakerDAO system is to gradually establish a decentralized stable currency, and building a currency system requires using assets that currently have consensus as collateral and borrowing their credit. Native cryptocurrencies are naturally an important component of collateral, but fundamentally, native crypto assets have high correlation, and it is difficult to achieve collateral diversification through crypto assets alone. To diversify the risks of the current cryptocurrency market, MakerDAO introduces some RWA assets as collateral for the stablecoin Dai.

MakerDAO Endgame is a series of future plans and ideas proposed by MakerDAO co-founder Rune Christensen in May 2022, outlining a path to building a decentralized stablecoin. This ultimately requires two types of collateral: decentralized assets that can be physically guaranteed to be fair, and real-world assets that can provide reliable liquidity and stability. It also aims to demonstrate the benefits that DeFi, Maker, and the Dai stablecoin can bring to the world, gradually integrating the world economic system with DeFi and adopting Dai as a payment and settlement tool.

The Endgame plan is divided into three phases, each characterized by its collateral composition, with the ultimate goal of turning Dai into a stablecoin:

- Bearish phase (current state): No restrictions on RWA collateral, Dai stablecoin anchored to the US dollar

- Bullish phase: Target interest rate for Dai is negative, free-floating

- Phoenix phase: No other type of RWA collateral in Dai’s collateral composition besides RWA with physical elasticity

Specific plans are designed for each phase’s corresponding collateral ratio, which can be found in the original article and will not be described here in detail.

Endgame Plan v3 complete overview – Legacy / Governance – The Maker Forum (makerdao.com)

Current MakerDAO RWA Composition

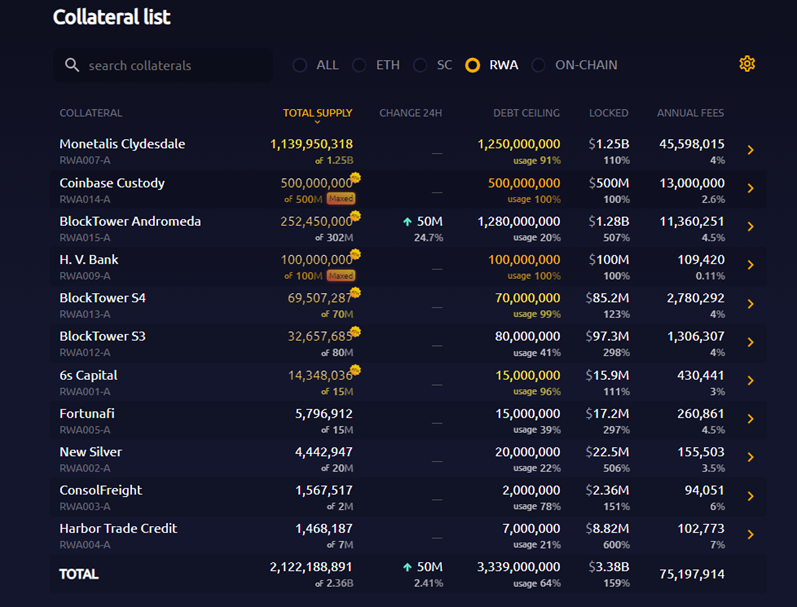

Throughout monetary history, humans have adopted currencies that use consensus-based scarce resources as equivalents, such as shells or gold, and later issued paper money backed by collateral in the form of scarce resources with consensus. This development eventually led to credit money issued based on military power, such as the US dollar. While Dai from MakerDAO has billions of dollars in circulation, it is still relatively small in the grand scheme of things and needs to borrow credit from other assets to gradually consolidate its position and demonstrate its advantages. In the Endgame plan proposed by MakerDAO’s co-founder, RWA is also introduced as a transition: in a world of crypto assets that are not yet solid enough, real-world assets are needed as anchors. According to MakerBurn data, there are currently a total of 11 RWA projects with $2.12 billion in assets serving as collateral for MakerDAO.

Figure 5: MakerDAO RWA collateral data, source: MakerBurn.com, data as of 2023.07.10

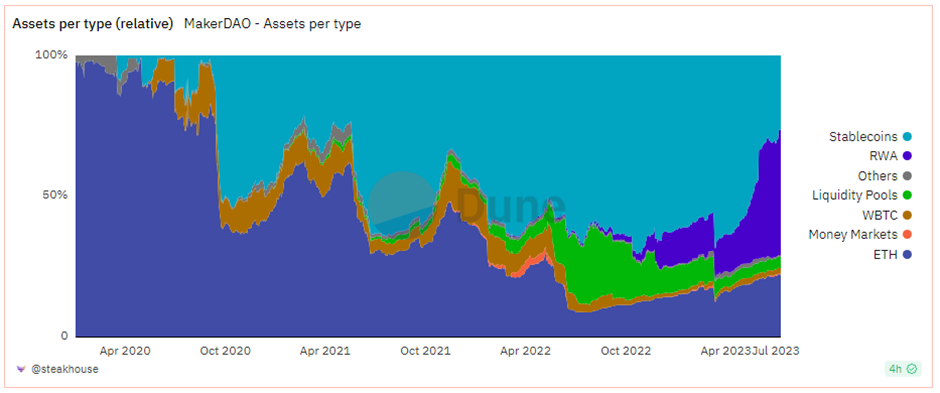

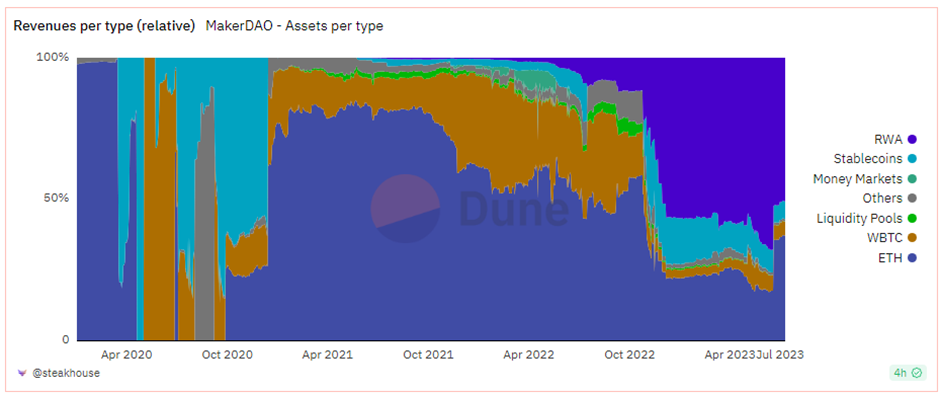

According to the Dune data panel, the income generated by these RWA assets has significantly increased MakerDAO’s profits. Currently, RWA accounts for about 40% of MakerDAO’s total assets, contributing over 50% of the profits.

Figure 6: MakerDAO asset composition, source: Dune.com, data as of 2023.07.10

The blue portion in the middle right represents the proportion of RWA, currently accounting for 41.5%.

Figure 7: MakerDAO protocol profit, source: Dune.com, data as of 2023.07.10

Among the composition of MakerDAO’s protocol profits, the upper right portion represents the profit from RWA, accounting for 51.1% of the total. As a result, in June 2023, MakerDAO proposed to raise the Dai Saving Rate (the risk-free rate of return for Dai) from 1% to 3.49%, providing attractive returns for Dai holders.

Divided by type, MakerDAO’s RWA mainly includes four parts:

- RWA 001, 6s capital, providing real estate loans.

- MIP81, RWA014, a proposal put forward by Coinbase Institutional in September 2022, which invests some of MakerDAO’s USDC in Coinbase USDC Institutional Rewards, providing a 1.5% APY based on USDC.

- Assets tokenized by decentralized lending platform Centrifuge, which MakerDAO purchases related tokens, including New Silver (real estate lending), BlockTower (structured credit), etc.

- MIP65, named Monetalis Clydesdale, RWA007, proposed by Monetalis, uses MakerDAO’s stablecoin to purchase short-term bond ETFs. It was first passed by proposal (US$500 million) in October 2022, and the debt ceiling was increased (to US$1.25 billion) through a proposal in May 2023.

Among them, 6s capital and Coinbase are separate cooperation cases, and this article will focus on the Centrifuge and Monetalis Clydesdale sections to explore how DeFi protocols integrate RWA. The related issues involved are not only technical solutions and business models but also governance architecture, legal frameworks, and asset ownership.

How to Purchase National Debt with DAO? MakerDAO’s Monetalis Clydesdale Project

MIP65, named Monetalis Clydesdale, was proposed by Allan Pedersen, the founder of Monetalis, in January 2022 and was passed and executed in October 2022. The goal is to invest part of MakerDAO’s stablecoins in high liquidity and low-risk bond ETFs. The initial debt limit is $500 million, and the limit will be raised to $1.25 billion through subsequent proposals in May 2023.

In MIP13 proposed in February 2022, the community discussed that about 60% of MakerDAO’s balance sheet assets were various stablecoins (with the Peg Stability Module (“PSM”) mechanism to ensure the value stability of Dai, and reserves mainly in USDC), and for the past 18 months, over 50% of the assets were stablecoins, but they did not generate profits for MakerDAO. The counterparty risk mainly comes from Circle (the issuer of USDC). The community hopes to invest stablecoins in some way, earn profits, and diversify risks, including the idea of investing in short-term US treasuries.

Later, among the MKR token holders who participated in the MIP65 proposal vote, 71.19% supported the proposal, and it was finally passed. MIP65 will launch an RWA-related vault, and the funds in the MakerDAO PSM mechanism will be invested in high liquidity bond strategies through a trust.

Monetalis is a consulting company founded by Allan Pedersen and Alessio Marinelli, providing consulting services and solutions for traditional finance and DeFi institutions. Both founders have extensive experience in traditional finance, consulting, and venture capital institutions. Monetalis’ investors include UDHC, Dragonfly, and MakerDAO co-founder Rune Christensen.

The overall business architecture of the proposal is as follows:

- MakerDAO delegates Monetalis to design the overall architecture through voting, and Monetalis needs to report periodically to MakerDAO

- Monetalis, as the project planner and executor, designs the overall trust architecture, in which:

- Riverfront Capital (SHRM Trustee (BVI) Limited) is the sole director.

- Hatstone (Fiduciary Group Limited) serves as the trading manager, and the trust’s transactions need to be approved by the company.

- Belvaux Management Ltd serves as the trust executor and ensures that the trust operates according to its objectives.

- The MakerDAO MKR token holders are the overall beneficiaries and can instruct the trust assets’ purchase and disposal through governance.

To achieve DAO-held RWAs, MakerDAO has designed a complex trust structure and new legal regulations, which come with high expenses, including an initial $950,000 for various expenses and ongoing payments to Monetalis, the trust’s related institutions and project managers.

In addition, the latest community proposal by MakerDAO, Project Andromeda, was proposed by community members at the end of May, with BlockTower as the project manager, to purchase short-term U.S. Treasuries, with debt limit of $1.28 billion Dai, further increasing MakerDAO’s investment in RWA. BlockTower has worked with Centrifuge and MakerDAO several times, and the team has extensive experience in traditional finance. With Monetalis’ established processes and procedures, if the MakerDAO community only wishes to increase its investment in RWA, this proposal is likely to be approved.

Tokenized Assets in DeFi Protocol – MakerDAO <> Centrifuge

Centrifuge is a decentralized lending platform that provides a series of smart contracts to create a transparent market for RWA assets without unnecessary intermediaries, enabling decentralized financing of RWA assets on the chain. The ultimate goal of the protocol is to reduce the cost of borrowing for businesses while providing stable RWA collateral returns for DeFi users.

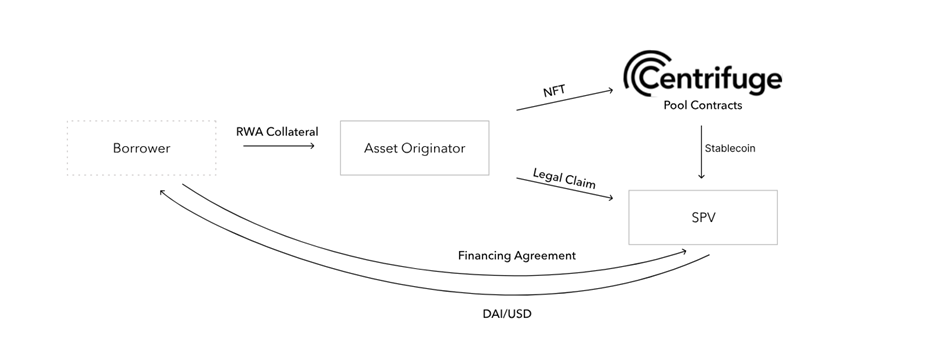

Figure 10: Centrifuge Fund Flow Chart, Source: Centrifuge Document

In fact, the process of issuing assets on Centrifuge is similar to the process of issuing Asset-Backed Securities (ABS). The fund flow process is as follows:

- The asset originator (such as BlockTower) creates a special purpose entity (SPV) as the issuer for each fund pool, as an independent legal entity to maintain the independence of each fund pool. Centrifuge’s contracts will create corresponding fund pools on Ethereum and associate them with the corresponding SPVs.

- Borrowers decide to use some real-world assets as collateral for financing, which can be invoices or real estate.

- The asset originator issues RWA tokens corresponding to the collateral, verifies them, and mints corresponding NFTs as on-chain collateral.

- The borrower and the SPV agree on the financing terms; the asset originator locks the NFTs in the relevant Centrifuge fund pool associated with the SPV and withdraws Dai from the pool’s reserves; Dai can be transferred directly to the borrower’s wallet or converted to dollars by the SPV and transferred to the borrower’s corresponding bank account.

- The borrower repays the financing amount and fees on the NFT maturity date and can choose to repay directly with Dai on the chain or through bank transfer, which will be converted to Dai and paid to the Centrifuge fund pool by SPV. Once all NFTs are fully repaid, they will be unlocked and returned to the asset originator and can be destroyed.

SPV is created by the asset initiator, and the borrower is usually connected to the asset initiator’s business.

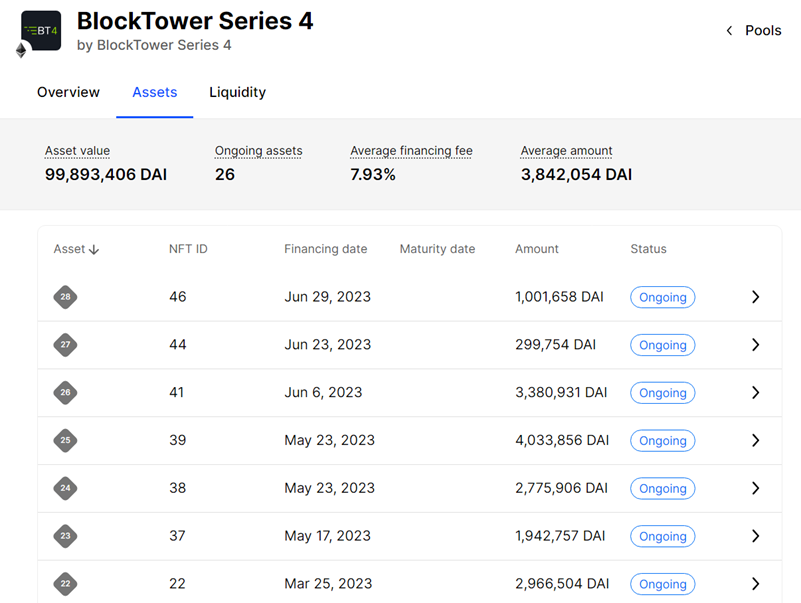

Figure 11: Centrifuge BlockTower series 4 asset, source: Centrifuge

The picture shows the Centrifuge App page, with a screenshot of BlockTower Series 4, and a list below of NFTs that serve as on-chain collateral, with each NFT corresponding to an off-chain real-world asset verified by the asset initiator. In this case, the asset is a structured loan.

Centrifuge provides a tool and market for projects/users who need to purchase RWA, enabling them to embed assets in the DeFi world while offering higher yields than the market average. However, there is also some risk, which comes from the borrower as the counterparty.

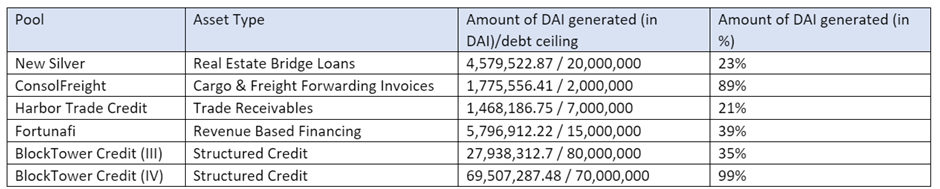

Data: Types and quantities of Centrifuge platform assets purchased by MakerDAO, as well as the amount of Dai issued with them as collateral, source: Daistats, data as of July 10th, 2023

The table shows several borrowing data from Centrifuge currently accepted by MakerDAO. Compared with government bond projects, the RWA tokenized through Centrifuge has a relatively small overall volume, and the largest BlockTower as a whole has just reached over 100 million US dollars. Compared with MakerDAO’s direct purchase of government bonds, the advantage of this solution lies in its simple process and the fact that MakerDAO itself does not need to build complex legal structures. In recent community discussions, Centrifuge will extract 0.4% of the fee to help these projects obtain loans; MakerDAO does not need to bear additional costs. However, due to the higher default risk of these projects compared to government bonds, there is greater counterparty risk as a whole.

Conclusion

MakerDAO, as one of the largest DeFi projects by volume, has tried two forms in several years of community operation related to RWA: directly purchasing and holding assets (MIP65) through DAO + trust and purchasing tokenized RWA (through Centrifuge), which is currently the best case of combining Tradfi and DeFi.

Compared with smaller DeFi protocols, MakerDAO has sufficient financial strength to achieve direct purchase of government bonds by DAO, but the cost is high. For this purpose, MakerDAO has established an innovative legal structure through a complex trust structure to ensure the safety of MakerDAO’s community assets and bring RWA revenue to Dai and MKR token holders. For this purpose, MakerDAO has paid a prepayment of $950,000 in expenses. In addition, Monetalis needs to charge 0.15% of the total amount as project management fee each year, and the other three participating companies also have corresponding expenses. According to reports, MakerDAO paid about $2.1 million in expenses for the purchase of the first phase of $500 million US government bond ETF in January 2023 for this project. This cost is too high for ordinary DeFi projects.

The reason for the complexity of the legal framework for purchasing national bond ETFs is due to the fact that the holders of MKR tokens cannot be fully mapped to the legal framework of the real world. The anonymity, lack of KYC, and different ownership by countries and regions (which need to comply with different laws and regulations) make it incompatible with the existing legal framework of the real world to ensure the security of the token holders’ assets (especially off-chain assets). Therefore, such a complex legal framework was designed to purchase national bond ETFs. Whether this legal framework will have problems remains to be seen.

For most DeFi protocols and project parties, they do not have the energy, resources, and ability to build a complete system. The second way to directly purchase tokenized assets will be easier. If there is a compliant asset issuer (traditional financial asset issuance requires holding relevant licenses or permits), a simple community vote is required. After the purchase, the assets are stored on the chain through multi-signature and the address is made public and supervised by the community. The risk is more on the counterparty risk of the issuer. The market opportunity for RWA token issuance, as mentioned earlier, in the short and medium term, there will be relatively more demand for bond-type RWA. The first to rise is national bond projects, as mentioned in the previous research report “Exploration of RWA Application Cases: 5 Attempts on US Treasury Bonds on the Chain”. OpenEden, MatrixDock, Maple Finance, Ondo Finance, etc. are all trying to tokenize national bonds. According to DefiLlama data, the two largest RWA TVL projects are also national bond projects.

In the case of DeFi development encountering bottlenecks, the DeFi community has also begun to further consider asset security issues, from only worrying about smart contract vulnerabilities to paying attention to compliant assets; traditional finance is highly compliant, through asset isolation, governance role allocation and isolation, process standardization, institutional restrictions, etc., to avoid small loopholes leading to large-scale system risks.

It is expected that in the future, we will see more protocols and projects incorporating RWA into their asset balance sheets to achieve diversified asset allocation. Here, compliant asset issuers will be indispensable, and better governance structures that combine on-chain and off-chain will also be gradually discovered and explored. Looking forward to the real world of the crypto world.

Reference:

- Overview – Maker Endgame Documentation

- Endgame Plan v3 complete overview – Legacy / Governance – The Maker Forum

Introduction to MakerDAO Collateral Onboarding – Collateral Onboarding

MIP21: Real World Assets – Off-Chain Asset Backed Lender – Legacy / MIPs Archive – The Maker Forum (makerdao.com)

RWA (Real-World Asset) in MakerDAO – Innovation and Strategy in Fintech – MakerDAO (daogov.info)

[RWA 007] MIP65 Monetalis/Clydesdale Legal Assessment – Legacy / Core Units Strategic Finance – The Maker Forum (makerdao.com)

MIP65: Monetalis Clydesdale: Liquid Bond Strategy & Execution – Legacy / MIPs Archive – The Maker Forum (makerdao.com)

[RWA007] MIP65 Monetalis Clydesdale/CES Domain Team Assessment – Legacy / Collateral Onboarding Domain Work – The Maker Forum (makerdao.com)

Real-World Asset Report – 2023-05 – Maker Core – The Maker Forum (makerdao.com)

RWA Case Study – US T-bill Tokenization | DigiFT

4,646,425,045 – Dai Stats

MakerDAO – MIP65 – Monetalis Clydesdale (dune.com)

MakerDAO – Dashboard (dune.com)

Like what you're reading? Subscribe to our top stories.

We will continue to update Gambling Chain; if you have any questions or suggestions, please contact us!