Authors: @Tonantzin_LC, markmuro1, Sifan_Liu; Compilation: Block unicorn

Just last year, it seemed like everybody was talking about cryptocurrency—from celebrities to athletes, news anchors to investors. Even elected officials got in on the act, as local governments touted cryptocurrency as a solution to issues like job growth and income inequality.

But now the hype cycle around cryptocurrency has ended (though Bitcoin has seen a recent surge). Entrepreneurs and venture capitalists have turned to generative AI tools, like those powering ChatGPT and other systems, in the wake of a major collapse in the cryptocurrency industry.

This raises some questions: What is the state of the cryptocurrency frenzy as new AI systems dominate the headlines? Where has job and entrepreneurship growth related to cryptocurrency recovered since the recent crash, and where has it not? And what lessons can state and local officials learn from it to prepare for the next big tech opportunity?

- Cryptocurrency crash and layoffs: Interpreting lessons for local leaders in building innovation ecosystems.

- Deep analysis of data on the Blur blockchain

- A comprehensive analysis of Balancer’s innovation in DEX: 7 liquidity pools and architectural logic

To explore these questions, this piece uses new data to examine the level and location of cryptocurrency activity in the United States. The overall business activity is tracked by analyzing cryptocurrency and blockchain industry job postings. Entrepreneurial vitality is measured with data from the startup field, and these signals are discussed to evaluate what the wisest next policy steps are for state and local legislators.

In recent years, cryptocurrency trends have fluctuated wildly

Even compared to the industry’s long history of instability, the past several years have seen cryptocurrency trends roiled. At the peak of the most recent hype cycle, some state and local government leaders began embracing cryptocurrency. These officials vied for cryptocurrency-related jobs by introducing bills or staging PR stunts, such as announcing they would receive their salaries in cryptocurrency or promoting a city-branded cryptocurrency. In other cases, they explored ways to allow residents to pay for government services with cryptocurrency or to allow governments to mine Bitcoin.

However, by the end of 2022, a spectacular collapse by Sam Bankman-Fried (SBF, founder of FTX) and his cryptocurrency exchange FTX triggered a catastrophic tide that sent cryptocurrency values tumbling. Some cryptocurrency companies filed for bankruptcy, many individual investors lost their life savings, and a few groups of investors were hit especially hard. The collapse caused many local leaders to abandon their earlier “gold rush” efforts, while regulators and other officials intervened and have since shifted the focus to protecting consumers.

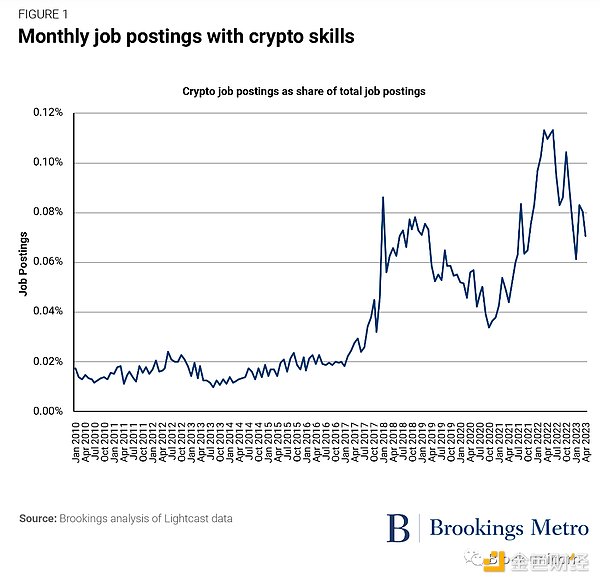

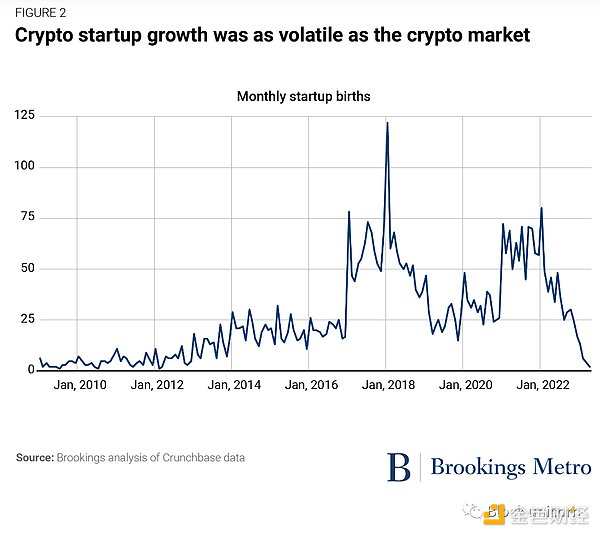

In short, the overall business and entrepreneurial activity in the cryptocurrency industry has undergone a wild and varied process, with impacts varying greatly by location. We can get a sense of the industry’s volatility by looking at job postings that require cryptocurrency and blockchain skills (an indicator of overall hiring and employment activity) as well as the number of cryptocurrency and blockchain startups.

In the mid-2010s, as cryptocurrency became increasingly popular, industry job postings trended upward overall. However, like the price of cryptocurrency, this trend was not without fluctuations. Recruitment information also changed with the fluctuation of Bitcoin value, with the most dramatic increase occurring in early 2021 and 2022.

Then, a significant decline occurred in the second half of 2022 as cryptocurrency projects such as TerraUSD, Three Arrows Capital, Celsius, and Voyager failed, as well as FTX’s collapse at the end of the year. This decline was very sharp, but it is worth noting that even at the peak, the number of job postings in the cryptocurrency industry was extremely low: less than 0.15% of all job postings, and now less than 0.08%.

In the cryptocurrency field, entrepreneurial activity has also been full of fluctuations, with the growth and decline of startups closely related to the value of Bitcoin. For example, the number of cryptocurrency startups increased until January 2018 and then plummeted, which coincided with the sharp fall in the value of Bitcoin and cryptocurrency at that time.

During the pandemic, the number of cryptocurrency startups slowly began to rise again, then began to decline again in January 2022, which again closely reflected the gradual decline in Bitcoin prices from January to May 2022, as well as more severe declines due to the failures of various cryptocurrency projects (as described above) and FTX’s disastrous failure.

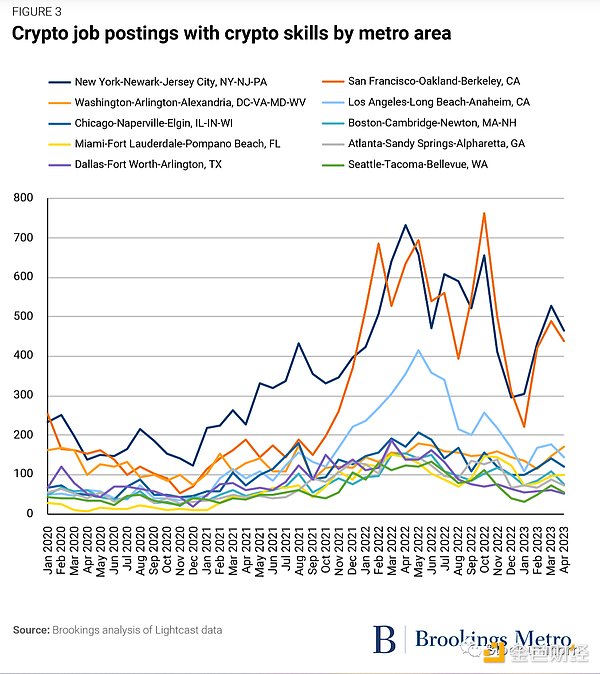

These trends have not been evenly distributed across major urban areas. Instead, although cryptocurrency consumption activity and disruption are widespread, some pre-existing technology and financial centers have seen heavy concentration of business and entrepreneurial activity, some of which are also places where cryptocurrency-related job postings (and possible employment) have rebounded at least in part.

In this regard, from January 2020 to April 2023, only a very small number of metropolitan areas in the United States dominated cryptocurrency activity. For example, the most prominent places for cryptocurrency activity include the metropolitan areas of New York, San Francisco, and Los Angeles – all of which were large tech or financial centers from the outset. In contrast, in most other places, the number of job postings related to cryptocurrency plummeted shortly after the Bitcoin price drop in 2022, following the collapse of the TerraUSD stablecoin. After this cryptocurrency crash, with the exception of the metropolitan areas of New York, San Francisco, and Los Angeles, as well as Miami and the Tampa metropolitan area in Florida, few places saw a rebound in employment after this crash, which had attracted a large number of remote workers during the pandemic.

However, the number of job postings related to cryptocurrencies in these Florida metropolitan areas – whether activity increased or rebounded – was significantly lower than in New York and San Francisco. Moreover, even in metropolitan areas that already had tech or financial centers, the number of job postings fell again after the November 2022 FTX crash, as the cryptocurrency market fluctuated again with the drop in Bitcoin prices.

Cryptocurrencies Concentrated in “Super” Cities, Lagging Elsewhere

As local leaders strive to attract economic growth to their areas, the volatility of cryptocurrency business activity – and its geographic patterns – presents important considerations.

Although some state and local governments are working to attract cryptocurrency activity, the startups and jobs associated with it are rarely stable or sustainable. While the above-mentioned large, established markets saw most of the work activity recover after the cryptocurrency market crash, recent statistics show that in most cases, the long-term job or entrepreneurial benefits of cryptocurrency-related business booms are few. Instead, in many cases, they create troubling pollution and energy costs, failed business projects, significant consumer and investor losses, and outbreaks of fraudulent behavior that local law enforcement agencies struggle to contain.

Given this, local and state leaders looking to build their regional economy should carefully consider whether the current cryptocurrency industry is worth their time, resources, and taxpayer dollars. At the same time, leaders may also want to consider whether they can develop other advanced emerging industries to stimulate economic growth.

On the first point: The significant cryptocurrency booms and relatively persistent activity witnessed in New York, San Francisco, and Los Angeles underscore how disruptive technologies (especially digital ones) concentrate in the largest markets, often leaving elsewhere behind. While many local leaders have tried to attract cryptocurrency business to create or grow tech centers in their regions, the evidence presented here suggests that urban areas that serve as the most important and resilient cryptocurrency hubs developed strong regional advantages in technology or finance before seeing significant cryptocurrency growth. In contrast, most other urban areas struggled with the decline of the cryptocurrency labor market and startup scene following the market’s collapse in the spring of 2022 and have not significantly recovered these losses. In short, the digital rich got richer, while most everyone else held steady.

These dynamics present a warning to regional leaders: It seems more important to have a tech center first than to make explicit efforts to attract cryptocurrency companies.

Also notable: the existence of a large local tech ecosystem appears to be more important than loose regulation. For example, the relatively active New York metropolitan area happens to be one of the few places with significant cryptocurrency regulations. Despite claims to the contrary by cryptocurrency enthusiasts, however, New York’s regulation does not appear to have hindered employment growth related to cryptocurrency as it remains one of the few places with ongoing job-posting activity. Meanwhile, “crypto-friendly” environments have not seen faster rebounds.

How Local Leaders Can Prepare for the Next Big Tech Opportunity

As far as thinking about future economic development goes, the brief cryptocurrency frenzy may have faded, but the past few years can still provide lessons for local leaders on how to capitalize on other emerging technologies, particularly given current interest in generative AI.

Local leaders face enormous pressure to innovate, adapt to new technologies, and stimulate economic growth. In most (if not all) places, the collapse of the cryptocurrency bubble should prompt local leaders to turn to other strategies for regional economic development. This should also be seen as a useful warning: not all emerging technologies are promising, no matter how fervently they are hyped. Local leaders should do due diligence to ensure that emerging technologies are both validated and suitable for their economic development goals.

Furthermore, local leaders should consider building more robust innovation ecosystems instead of relying on the development of a single industry or technology. This includes cultivating local education and training resources to meet evolving workforce needs, encouraging and supporting business innovation, and enhancing community attractiveness through intelligent urban planning and infrastructure investment. Ultimately, the success of economic development will depend on a diverse economic structure that can adapt and leverage various technological opportunities, rather than simply chasing a single, possibly fleeting, hot trend.

In summary, the collapse of the cryptocurrency frenzy provides a valuable lesson: local leaders need to be cautious, wise, and visionary when deciding how best to use limited resources to attract and develop emerging industries. While emerging technologies may bring enormous economic potential, they also bring risks and challenges. To achieve sustainable economic development, leaders need to focus on building strong, diverse economic ecosystems, rather than chasing potentially short-lived hot trends.

Like what you're reading? Subscribe to our top stories.

We will continue to update Gambling Chain; if you have any questions or suggestions, please contact us!