Author: TaxDAO

In addition to income tax issues, cryptocurrency transactions may also involve turnover tax issues. This article will analyze the current and future tax situation of cryptocurrencies from the perspective of turnover tax, aiming to provide relevant reference information for cryptocurrency investors. This article believes that compared to turnover tax, more countries in the future will still prefer to levy cryptocurrencies through income tax or other forms of taxation.

1. Turnover Tax and Its Main Types

- Severe Lag Analysis of India’s Cryptocurrency Tax System, Regulatory Status, and Trends

- The PEPE Sell-off Unequal Distribution of Profits or Planned Escape?

- Spanning a 10-year cycle, 6 charts to understand the correlation between Bitcoin price and mainstream assets such as US stocks.

1.1 Overview of Turnover Tax

Turnover tax is a type of tax that is levied based on the turnover or quantity of goods or services. Turnover tax is an indirect tax that is levied during the circulation of goods.

Based on the method of collection, turnover tax can be divided into ad valorem tax and specific tax. Ad valorem tax is levied based on the value or price of goods or services, such as value-added tax and sales tax. Specific tax is levied based on the quantity or weight of goods or services, such as customs duty and resource tax.

1.2 Main Types of Turnover Tax

The main types of turnover tax include value-added tax, sales tax, consumption tax, business tax, and customs duty.

-

Value-added tax (VAT) is a type of turnover tax that is levied based on the value added at each stage of production, circulation, and consumption of goods or services, reflecting the true value added of goods or services.

-

Sales tax is a type of turnover tax that is levied on the sales amount or price of goods or services. It is levied only at the final stage of sales and only involves the final consumers. The United States is a typical representative country that levies sales tax. In the United States, whether to impose sales tax and how to set the tax base and tax rate are determined by individual states and local governments.

-

Consumption tax is a type of turnover tax that is levied on specific goods or services at the stages of production, import, or sales. Unlike value-added tax, consumption tax is usually targeted at specific goods such as cigarettes and luxury goods, with the aim of adjusting consumption structure and promoting conservation and environmental protection.

-

Business tax is a type of turnover tax that is levied on the turnover derived from providing services, transferring intangible assets, or selling real estate. Business tax was the old turnover tax in China and was replaced by value-added tax in 2015.

-

Customs duty is a type of turnover tax that is levied on goods and articles imported and exported, and is only levied during the entry and exit of goods.

Specifically, capital gains tax is not considered turnover tax because it is not levied at each stage of production, circulation, and consumption of goods or services, but rather levied when assets are transferred or traded.

2. Cryptocurrency Turnover Tax

2.1 Taxes that may arise during the circulation of cryptocurrencies

Cryptocurrency turnover tax refers to the tax levied on transactions or activities conducted using cryptocurrencies. Generally speaking, cryptocurrencies are not subject to consumption tax due to their lack of luxury or “harmful” nature, and they are not subject to customs duty because they are digital assets rather than physical goods. The discussion on cryptocurrency turnover tax in a working paper titled “Taxing Cryptocurrencies” published by the IMF in July 2023 is also limited to this scope. Therefore, cryptocurrency turnover tax mainly includes value-added tax and sales tax. This article attempts to provide a brief analysis of the tax situation regarding cryptocurrency value-added tax and sales tax in major countries around the world.

Different countries or regions may have different definitions, classifications, and taxation methods for cryptocurrencies, so cryptocurrency investors need to consult the relevant circulation tax regulations according to their jurisdiction.

2.2 Countries and regions that levy circulation tax on cryptocurrencies

Currently, most countries and regions do not levy circulation tax on cryptocurrencies, which is related to their legal definition of cryptocurrencies. Only when cryptocurrencies are defined as “commodities” or “assets” can circulation tax be levied. Countries and regions that consider cryptocurrencies as “currency” do not impose circulation tax on cryptocurrencies.

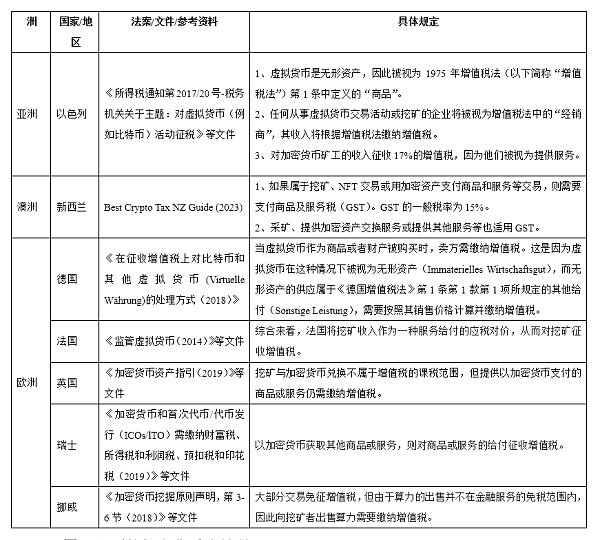

This article briefly summarizes the representative countries and regions that levy circulation tax on cryptocurrency-related transactions, as shown in the following table.

2.3.1 Cryptocurrency circulation tax in the European Union

The regulation of cryptocurrency circulation tax in the European Union is leading internationally. As early as the Hedqvist case in 2015, the European Court ruled that the exchange service between legal tender and Bitcoin constitutes a taxable value-added service.

The Hedqvist case is roughly as follows: Swedish resident Hedqvist intended to provide exchange services between legal tender and Bitcoin. The Swedish Administrative Court submitted this case to the European Court to determine whether the value-added obtained by Hedqvist in this exchange service needs to pay value-added tax. The European Court believes that since Bitcoin is not a tangible asset, the exchange of legal tender and Bitcoin does not belong to the payment of goods, but the payment of services, and Hedqvist and the exchange party have formed a “consideration” in the transaction. Therefore, the European Court determined that the exchange service between legal tender and Bitcoin belongs to the taxable service under Article 2(1)(c) of the EU VAT Directive.

At the same time, the European Court believes that the spirit of Article 135(1)(e) of the VAT Directive applies to cryptocurrency exchanges, so it can be presumed that exchanging legal tender for cryptocurrencies is exempt from value-added tax.

Therefore, in cryptocurrency exchanges, EU countries are influenced by this precedent and include the exchange between cryptocurrencies and legal tender, as well as the exchange between cryptocurrencies, in the scope of value-added tax, but applicable exemptions can be used. However, regarding mining operations, the situation is different: except for France, most countries (such as Germany, Ireland, Sweden, etc.) believe that mining operations are not subject to value-added tax.

2.3.2 General practices in other countries

European countries outside the European Union have generally adopted the relevant spirit of the European Court’s ruling on the Hedqvist case, such as the United Kingdom, Norway, etc. Countries outside Europe generally adopt a similar approach to Israel, excluding the exchange of virtual currencies from the scope of value-added tax. At the same time, these countries treat the act of purchasing goods or services with virtual currencies as taxable sales (i.e., levying value-added tax). As for the treatment of value-added tax for “mining”, it is more diverse and has not formed a mainstream policy opinion yet.

Another design idea for taxing cryptocurrencies is to completely exempt them from transaction taxes and instead regulate them from the perspective of income tax. Typical examples include Singapore, Japan, South Africa, and Hong Kong, China.

3 Future Prospects of Cryptocurrency Transaction Taxes

There is currently no unified standard or specification for cryptocurrency transaction taxes worldwide. Different countries and regions have significant differences in the definition, classification, recognition, tax basis, and tax rates of cryptocurrencies, resulting in the complexity and uncertainty of cryptocurrency transaction taxes.

Currently, most countries and regions tend to include cryptocurrencies in the scope of income tax and tax the income generated from buying, selling, exchanging, gifting, and donating cryptocurrencies. This article believes that compared to transaction taxes, more countries will still tend to use income tax or other forms of taxation to levy cryptocurrencies in the future. This is because income tax collection and accounting are more convenient compared to transaction taxes. It can not only adapt more flexibly to the fluctuations and innovations of the cryptocurrency market, avoiding tax losses or excessive taxation caused by price uncertainty or product diversity, but also coordinate tax system differences between different countries and regions, avoid international double taxation, and promote cross-border transactions. Therefore, income tax, compared to transaction taxes, can better reflect the value changes of cryptocurrencies and the taxpayers’ ability to bear tax burdens. In contrast, transaction taxes have some problems and challenges in terms of collection costs, effects, and fairness.

Like what you're reading? Subscribe to our top stories.

We will continue to update Gambling Chain; if you have any questions or suggestions, please contact us!