Author: TapiocaDao

Time: October 20, 2022

Article Source: https://mirror.xyz/tapiocada0.eth/CYZVxI_zyislBjylOBXdE2nS-aP-ZxxE8SRgj_YLLZ0

Liquidity Mining Obituary

June 16, 2020 – October 19, 2022

- Weekly Featured Special | SEC Goes All Out, Cryptocurrency Industry Faces Crisis?

- Analysis of Curve War: Torus, a new player that changes the track pattern of the whole-chain LSD omnipool

- Research on Canto, a new DeFi public chain

Liquidity mining is a mechanism that incentivizes users to provide liquidity and receive reward tokens. TapiocaDAO officially announced the end of liquidity mining today. We offer a novel and brand new DeFi monetary policy that has sustainability, permanent value capture, and economic consensus among participants. These features address the “trilemma” problem encountered by liquidity incentive mechanisms, which TapiocaDAO solves with DAO Stock Options (DSOs). We invite you to read the following liquidity mining obituary as well as details about this disruptive mechanism.

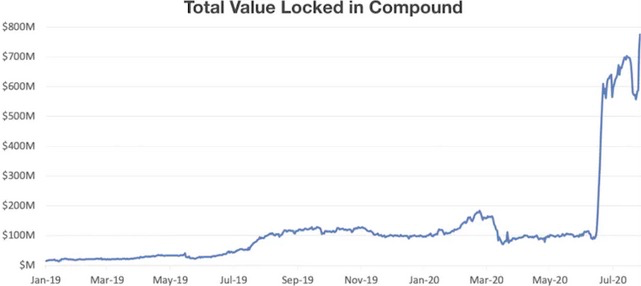

Liquidity mining began on June 16, 2020, introduced by the decentralized lending protocol Compound. Participants who either borrowed from or lent to the Compound protocol received COMP tokens as rewards. These tokens were used to increase the borrowing rate for borrowers and subsidize the interest rate for lenders.

Compound’s “TVL” (Total Value Locked) increased by 600% immediately after the liquidity mining program was launched. However, this had an unexpected adverse effect on Compound’s rapid growth. Few “miners” ended up holding the COMP tokens they earned. According to reports, only 19% of accounts held onto 1% of the COMP tokens they received, selling 99% into the market.

Second, the cost of issuing and circulating new tokens that Compound incurred by leasing liquidity often resulted in huge operational losses compared to the revenue generated by leasing liquidity. In this case, operational losses refer to the difference between the protocol’s operating expenses (issuing reward tokens) and revenue (fees). In addition to serious dilution of COMP token holders, this huge operational loss is its main negative impact.

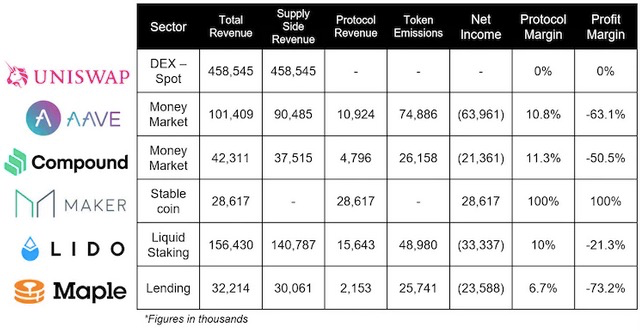

As shown in the above figure, almost all DeFi projects have experienced huge losses. This is not because of insufficient revenue. DeFi protocols generate relatively high revenue. For example, AAVE’s annualized revenue reached $101.4 million. The problem seems to lie in allocating 90% of its revenue to borrowers, leaving about 10% or $10.92 million of profit margin for the protocol, but this is not the core problem. The protocol still has millions of dollars in revenue. The problem is entirely due to the role of liquidity mining. AAVE paid out $74 million in liquidity incentives, resulting in a net loss for the largest DeFi protocol of $63.96 million. Does AAVE need to give AAVE tokens to liquidity providers for free? No, but that’s the reality.

However, the only profitable project is Maker. It has created a total revenue of $28.61 million, all of which belongs to the DAO. Without reward tokens and dividends, it proves that not every protocol needs tokens. In fact, many DeFi enthusiasts prefer protocols that do not offer tokens. No reward tokens, no operating losses, and no dilution. But it is undeniable that a well-designed and balanced token economy can create miracles.

Some people may say, “These incentive plans attract liquidity, what’s wrong with that?” “Liquidity is king.” In fact, what is attracted is not liquidity, but liquidity locusts; those disloyal liquidity miners who take rewards and leave, turning to the next exciting token project, or waiting until the rewards of the current project are exhausted. Because these liquidity “locusts” use the single function provided by liquidity mining token rewards-governance, Compound cannot even turn off the liquidity mining faucet. This has led to a serious problem, that is, in a token economy, there is a gap between financially invested participants and loyal token holders. Loyal token holders have actually contributed to the growth of the protocol, while liquidity miners hope to obtain benefits at any cost. They will vote to continue to pursue the maximum benefit, and all of this is our fault. We did not guide and design the token economy correctly, which led to this imbalance. We should take responsibility for this problem and find solutions to restore the healthy development of the token economy.

Compound is not the originator of the concept of “liquidity mining” (even smart contract-based liquidity mining is not). This honor should be attributed to Synthetix’s “StakingRewards” contract, which was co-written by Anton from 1inch. Like many things, “liquidity mining” is just an old idea with a new name. In the field of cryptocurrencies, the concept of liquidity mining can be traced back to FCoin in 2018, a platform known for severely dragging down the Ethereum network. In fact, FCoin was the first cryptocurrency product to offer a liquidity mining concept similar to what we know today, which they called “transaction fee mining” (the name is a bit bad, isn’t it?).

FCoin’s founder is none other than Huobi’s former CTO, Zhang Jian. FCoin offered its traders a large amount of token incentives, hoping that this liquidity would attract more users. FCoin was essentially betting that users would continue to stay on the exchange after the liquidity incentive program ended. However, this was not the case. Users did not stay.

A token model with a decent liquidity incentive design also needs a sound monetary policy, including addressing token supply (dilution), token demand, token circulation, and other issues. This is crucial because it will affect token prices, and token prices will affect the effectiveness of incentive plans, which in turn will affect how much liquidity the protocol can attract.

The current goal of liquidity mining is to rent liquidity. Let’s ask a question: would you rather receive $1 million or $100,000? If you answer “of course $1 million,” then you, like almost every existing DeFi protocol, have not properly evaluated this question. How long will you have this $1 million? When time is factored in, it will reveal the key details that provide true value for the evaluation. If the question becomes “would you rather have $1 million for 1 second or have $100,000 for 1 year,” your answer is likely to be different. In one second, you can hardly do anything, but in one year, you can do a lot of things; the protocol is the same.

These “liquidity leasing incentive plans” attract speculative liquidity providers, but are completely unsustainable and have extremely limited effects on their core goals. According to a study by Nansen, “up to 42% of liquidity mining participants withdrew from the project within 24 hours of its launch. By the third day, 70% of participants had withdrawn from the contract and never returned.”

Based on this data, liquidity speculators enter these projects simply to maximize their returns, and the protocol has created no real long-term value except for negligible fee income, which is insignificant compared to the cost of incentivizing liquidity. In order to incentivize these liquidity mining participants, the protocol typically allocates most of the token supply to liquidity providers, as they have no loyalty to the protocol itself and only exist to grab profits. In other words, these token rewards are nothing more than protection fees from the mafia, “as long as you keep paying me, your DefiLlama ranking will remain high, understand?” In the end, what does the protocol actually have through liquidity mining? Absolutely nothing. Once the protocol stops paying rewards, liquidity will quickly disappear.

Whoever controls liquidity controls DeFi.

Welcome to Olympus

Olympus rethinks this broken model; they didn’t try to create a model that could perpetually pay for liquidity provision (which seems impossible), but instead they correctly recognized that a protocol should create permanent value for itself and add to its balance sheet. They leveraged the demand for OHM tokens to create POL (Protocol Owned Liquidity). They were the first to realize that you don’t need to negotiate with liquidity providers, but can beat them at their own game and create permanent value for a DAO’s balance sheet in a gamified way, letting the mafia think they won.

Although some may say that Olympus was an experiment that failed, Olympus was the first to release a project that perpetually paid for liquidity provision. POL became an important mechanism in the “DeFi 2.0” space. So, if Olympus succeeded in identifying the key monetary policy oversight in DeFi – the lack of true value creation – why did they ultimately “fail”? The 3,3 mechanism, like other liquidity mining projects, led to OHM bubble inflation by offering unreasonable high yields. (Remember: if you don’t know where the yield comes from, you are the yield).

Ultimately, the economic inconsistency of the protocol participants reached a critical point, and liquidity miners who controlled the majority of OHM supply felt they had extracted as much value as possible and left, causing OHM prices to spiral out of control. Olympus was in panic mode and offered inverse bonds. Inverse bonds allowed users to sell their OHM tokens back to POL assets. This move caused OHM’s POL (the only true value created) to be lost, left the treasury with a lack of diversity, and reduced investor confidence. Redacted became the only winning participant in Olympus because it quickly adjusted strategy to maintain POL once dilution was too high.

However, even though Olympus “failed,” that shouldn’t negate the significance of Olympus and POL.

Enter the ve Era

ve, or “voting escrow,” was pioneered by Curve and is embodied in veCRV. Curve places a great emphasis on protocol loyalty and requires that liquidity rewards be locked up so that potential liquidity providers can get the highest return from the liquidity incentive program. Curve has created a layered incentive structure: the higher your loyalty to Curve, the more rewards you will receive.

Although the method of considering loyalty (now borrowed liquidity + time) greatly enhances Curve’s ability to maintain consistency among economic participants and create more loyal protocol users, problems still exist: Curve does not own liquidity; investors will still be affected by the dilution brought about by token distribution, and liquidity providers can still obtain valuable CRV with almost no cost (withdraw provided liquidity at any time). Imagine how much value Curve’s POL could create if it wanted to, and how much of that value is left on the table while Tapioca can capture it.

When the value of CRV decreases, CRV incentives also become less valuable, so these token issuances also become less valuable. The protocols compete for veCRV in the Curve War, creating a mechanism of “embedded incentives”; Protocol X casts and circulates their tokens through incentive plans to have veCRV and thus control CRV incentives. This is a good mechanism, but as a protocol, all you do is dilute shareholders’ interests by casting new tokens to obtain veCRV, a less liquid asset. Add in Redacted and Convex, and you have an internal mechanism within an internal mechanism. These features should have been built into Curve from the beginning. The inefficiency of ve actually spawned the entire industry. You may attract more liquidity through veCRV incentives rather than your own tokens, so why not focus on increasing the value of incentives themselves?

This is not to emphasize criticism of Curve, because ve is obviously the best pledge method ever, as it can achieve economic alignment of participants. However, at the protocol level, Curve War is a bit illusory. As a protocol, why give up valuable assets to obtain a less liquid asset, which may not have valuable incentives at any given time? In fact, services such as Yearn, Badger, and StakeDAO that provide leasing of veCRV are actually more attractive – using its intrinsic value when it exists to attract liquidity. Attract liquidity through “leasing” veCRV and try to permanently trap these liquidity in the protocol as much as possible.

Finally, for Curve, the only way to create permanent liquidity is to become part of the “mafia.” The protocol needs Curve to stabilize their stablecoins, not to earn fees. What if you don’t try to lease more liquidity, but use the fees generated by the Curve pool to directly own more liquidity? This is exactly what Tapioca is doing. We have left the virtual world, accepted the “red pill,” and are trying to own the only real thing in DeFi-liquidity. Or you can choose to take the “blue pill” and pretend to permanently incentivize liquidity by gamifying these mechanisms. I will show you how deep the rabbit hole goes, Neo.

André Cronje Enters the Scene

Before creating Solidly Exchange and ve3,3 – two initiatives aimed at addressing long-standing issues in ve liquidity mining – André created OLM – Options Liquidity Mining – for his experimental automated network, Keep3r Network.

André (in his typical fashion) pioneered an initiative that would ultimately change DeFi. What happens when you provide liquidity to Curve and receive CRV as your liquidity mining reward? Liquidity providers exercise a call option on CRV with a strike price of $0 and no expiration date. When you start to view liquidity mining programs as American call options, the protocol suddenly has a power it did not have before.

André’s OLM has one problem, though – the protocol still does not capture any POL (protocol-owned liquidity). The redemption of options is key to DSO. oKP3R distributes option redemption to vKP3R holders, a noble and simple way to incentivize locking. But we come back to a core question: “Why are we providing liquidity incentives to our protocol?” The goal is to generate enough liquidity depth to sustain the core functionality of the protocol, but these services are intended to generate revenue to maintain the entire organization. By holding your own liquidity, you no longer need to provide incentives for it. Choose to take the red optionality “red pill” and exit the liquidity mining matrix world.

Shut Down the Money Printer

Kain Warwick’s Synthetix Improvement Proposal SIP-276 addresses the severe inflationary problem in DeFi summer protocols. These protocols heavily incentivize (rent) liquidity, and Synthetix hopes (as usual) to be the first to stem further supply expansion. When Synthetix’s revenue has at times surpassed that of Ethereum, it is hard to argue it has not successfully launched its ecosystem.

As Compound has seen, it may be very difficult to turn off these incentives, as liquidity providers often control governance power. If the proposal passes, liquidity, which is rented, may immediately leave the protocol, making it difficult to sustain the ecosystem in the future due to reduced liquidity depth and lowered fees. While Tapioca will follow a similar path, Tapioca will strive to acquire as much POL as possible during the expected inflation process. Once the supply reaches the predetermined peak, the protocol will rely on its own POL to sustain itself. The cost and returns of these POL will form a virtuous cycle (acquire POL > create returns on POL > acquire more POL > repeat). Tapioca will be able to cautiously inflate the supply of TAP using American options, which will themselves create permanent value.

The selection contains an HTML code that is empty and consists of a paragraph element with a strong element inside that is also empty.

Like what you're reading? Subscribe to our top stories.

We will continue to update Gambling Chain; if you have any questions or suggestions, please contact us!