Author: BitAns, Krypital Group

This article is for communication and learning purposes only and does not constitute any investment reference.

After the bankruptcy of FTX, the trading volume and attention of decentralized derivative exchanges have significantly increased. In recent years, with the improvement of L2 and various open-source Appchain architectures, the reliability and concurrency performance of Dex have greatly increased. Dex PERP has become the best-performing product in the bear market. As the industry continues to explore decentralization, these types of products will undoubtedly become an important part of the industry in the future.

Currently, mainstream decentralized derivative designs mainly include the Orderbook model represented by Dydx and the Point-to-Pool (Pool and Vault) model represented by Snx. Snx, which was originally an asset synthetic platform in 2017, has been reconstructed and upgraded into a modular liquidity protocol, aiming to become a universal liquidity layer for on-chain financial products. New features and improvements are expected to bring new business increments and valuations. In this article, we will interpret Snx V3 based on data and application scenarios.

- Financing Weekly Report | 24 public financing events; Zero-knowledge proof company RISC Zero completes $40 million Series A financing, led by Blockchain Capital.

- OpenAI releases new feature now you can customize the personality of ChatGPT.

- Inspired by Arthur Hayes and supported by multiple CEX, what are the innovations of the decentralized stablecoin protocol Ethena?

TOC:

I. Existing Mechanisms and Issues of Snx V2

II. New Feature Modules of Snx V3

A. Liquidity as a Service

B. New Debt Pool and Collateral Mechanism

C. Perps V2 and Perps V3 Engines

D. Oracle Improvement Plan, Anti-Oracle Delay Arbitrage

E. Cross-Chain Liquidity Solution

III. Economic Model + Revenue Data

Snx V2 Operating Mechanism

To better understand V3, we need to briefly review the existing design of Snx and the various problems that exist.

There are two types of core users in the Snx ecosystem:

1. Stakers – Pledge Users

Stakers pledge Snx to receive system inflation rewards and trader transaction fees.

2. Traders – Trading Users

Users who use atomic swaps or trade Perps within the Snx protocol.

Principle of Synthetic Assets

The principle of pledging stablecoins is to generate tokens equivalent to the value of the US dollar by pledging assets. Similarly, users can also pledge assets and generate tokens anchored to the price trends of stocks, gold, and other assets through the price data of oracles.

The Snx ecosystem currently has sUSD anchored to the USD price, sBTC anchored to the Bitcoin price, and sETH anchored to the Ethereum trend. They are collectively referred to as Synths synthetic assets.

The entire system’s debt is settled in sUSD. In Snx V2, only Stakers are allowed to Mint sUSD by pledging Snx. Essentially, Snx is pledged to borrow sUSD. Therefore, the minted sUSD is the debt of the users and the entire system.

When the collateralization ratio reaches 400% or above (this ratio will be determined by DAO voting based on market conditions), SNX holders will receive inflation rewards and transaction fee rewards. If the collateralization ratio falls below 160% and the collateral is not replenished with SNX within a 12-hour buffer period, or if the sUSD debt is not repaid to increase the collateralization ratio to 400% or above, the Staker may face the risk of liquidation. If you need to unlock the collateral, the Staker needs to repay all sUSD debt to withdraw.

Atomic Exchange Process

The transaction between SNX synthetic assets is completed by smart contract, which destroys one token and mints another token. So, except for price fluctuations caused by price delay, there will be no slippage when TVL is met.

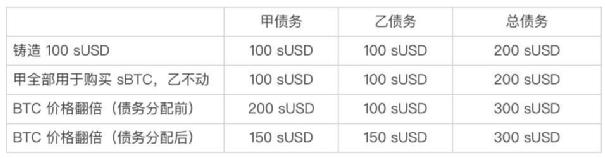

Principles of the Dynamic Debt Pool

The total value of all Synths assets in the entire system = total issued debt of the system

If a trading user Trader exchanges sUSD for other Synths assets, such as sBTC, the overall debt will increase or decrease with the fluctuation of the corresponding Synths price. Therefore, the overall debt of the system is not fixed, hence it is called a dynamic debt pool. And the total debt of the system is shared proportionally by all SNX collateral holders. So, a Staker who only participates in minting sUSD without any other operations will also have dynamic debt.

Case:

Assume that there are only two participants in the system, A and B, and they each collateralize SNX to mint 100 sUSD. Assuming the current price of BTC is 100u, when A purchases sBTC with sUSD, the SNX protocol will destroy 100 sUSD in the debt pool and mint 1 sBTC in the debt pool.

If B does not take any action. As shown in the figure above. When the price of Bitcoin doubles, the debt of both A and B becomes 150 sUSD, but the asset value of A is 200 sUSD and the asset value of B is still 100 sUSD. At this time, A sells sBTC and obtains 200 sUSD, and only needs 150 sUSD to redeem SNX, while B needs to purchase an additional 50 sUSD to redeem the collateralized SNX.

Therefore, when a trader suffers losses, their losses will reduce the total value of the global debt pool, thereby reducing the average debt level of all collateral holders and allowing each collateral holder to share benefits proportionally, that is, reducing debt. Conversely, when a trader makes a profit, it will increase the pool’s debt. Each Staker will share the loss, which means they need to purchase additional sUSD to redeem their SNX.

SNX supports spot atomic exchange and perpetual trading. When the pool size is large enough, the impact of a single transaction on the pool will tend to stabilize, and Stakers can earn transaction fees for each transaction. According to the Kelly formula, in the long run, Stakers will be in a profitable mode.

However, if the long and short positions in the system are not balanced, Stakers may face situations where others profit while they suffer losses in extreme or one-sided market conditions. In order to further reduce the risk for Stakers, V3 provides more mechanisms to maintain system Delta neutrality.

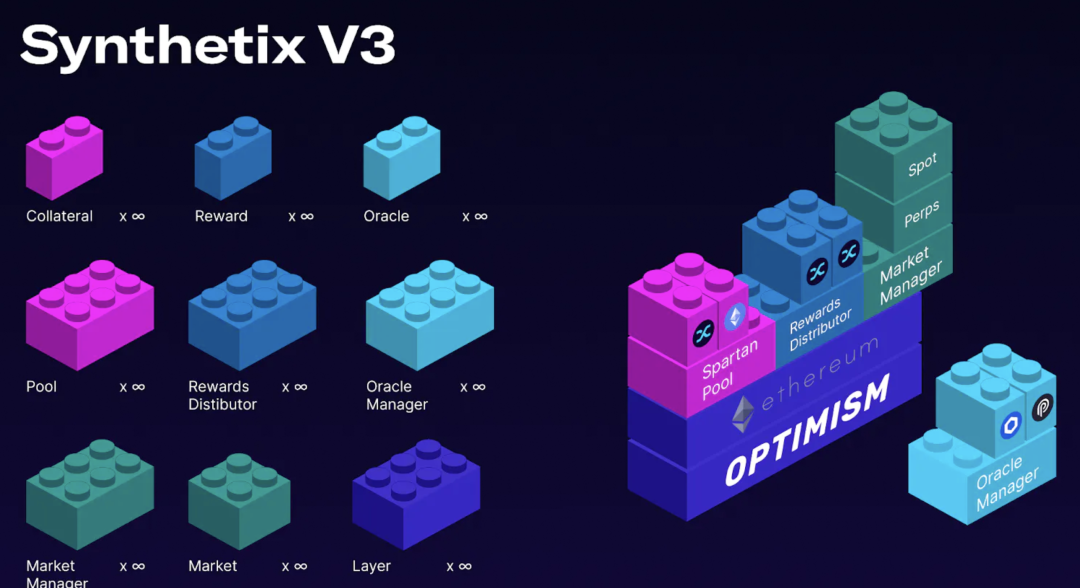

What does Snx V3 bring?

Liquidity as a Service

Liquidity as a Service

After two years of redevelopment, Synthetix V3 positions itself as the liquidity layer of decentralized finance. Synthetix V3 will be launched in stages in the coming months, and in the plan, the existing functions of V2 will become a subset of V3. After the final version is launched, developers can directly integrate the Snx debt pool to obtain liquidity when developing new derivative markets, including perpetual futures, spot, options, insurance, exotic options, and other derivative markets, without starting from scratch.

Current products in the Snx ecosystem

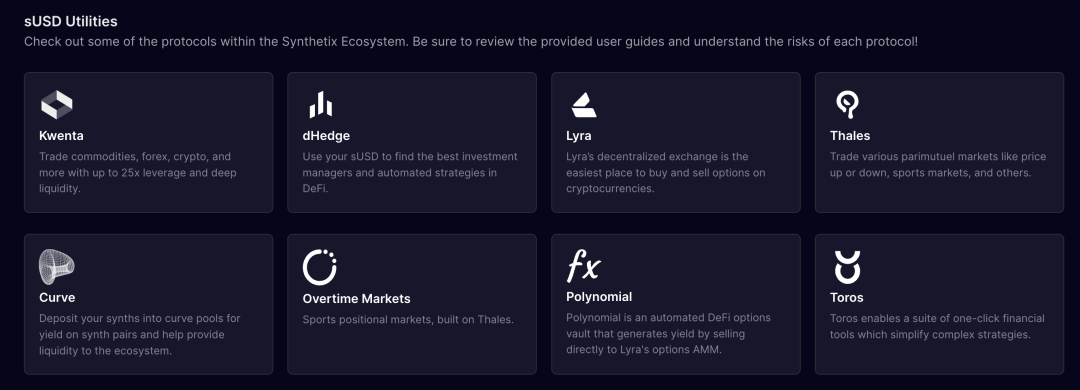

Examples of applications proposed by Snx include:

-

Perpetual futures/options/structured products: Supports perpetual futures trading, leveraged positions, including basis trading and funding rate arbitrage.

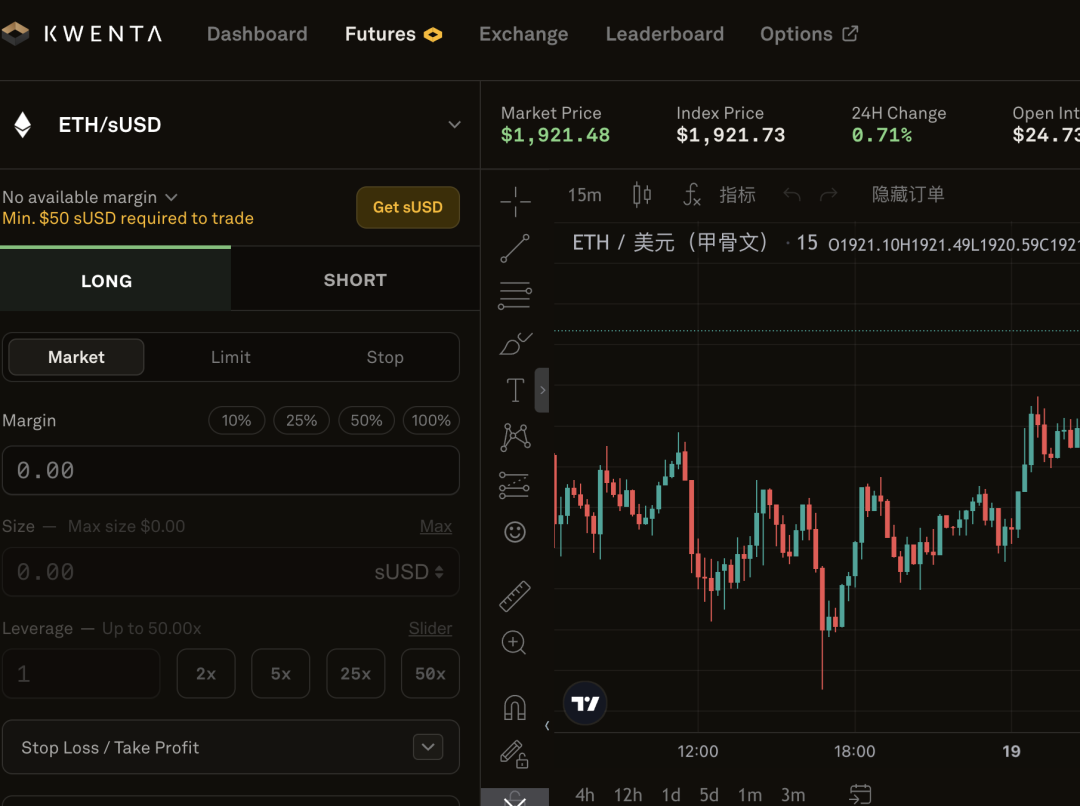

Example: Currently launched Kwenta, Polynomial exchange, and GMX can also be built on Synthetix V3.

-

NFT-Fi lending/perpetual contracts: Users can borrow synthetic assets anchored to the trend of NFTs or create markets for perpetual contracts speculating on the future prices of NFTs.

For example, nftperp.xyz can be built on Synthetix V3.

-

Insurance market: Users can purchase insurance contracts for various risks, collateralize them in the pool, and manage them through smart contracts.

For example, Nexus Mutual can be built on Synthetix V3.

-

Prediction markets/binary options/sports betting: Users can make predictions based on the outcomes of events.

Examples: Election results or sports games. Currently launched Lyra and dhedge in the Snx ecosystem.

-

RWA market: With reliable oracles and trusted entity verification, trading markets for synthetic assets of off-chain assets such as artworks, carbon credits, or other off-chain assets can be developed on-chain.

New debt pool and collateral

As mentioned above, in the Pool and Vault model of Snx, Stakers need to temporarily act as counterparties for Traders, and the size of the Staker debt pool determines the liquidity limit.

Currently, having a single collateral may lead to the following issues:

-

It can result in the maximum open interest in the system being limited by the market value of Snx itself, which means limited liquidity for traders.

-

Different synthetic assets have different price volatility. The returns and risk-reward ratio for Stakers may not align.

-

In extreme conditions, there may be a potential danger of spiral liquidation.

From Kwenta, we can see the total position of Snx held by the entire network. Under the incentive program with OP, the short and long positions of BTC and ETH have repeatedly approached the system’s capacity limit.

To address the above issues, V3 has introduced the following features:

Isolated Debt Pools

In the existing Synthetix V2, all transactions go through a single Snx debt pool. However, different synthetic assets have different volatilities, risks, and returns. This problem is addressed in order to prevent oracle delay attacks. (This article will list relevant cases in the section on oracle delay attacks.)

Synthetix V3 has passed SIP-302: Pools (V3) proposal, allowing stakers to decide which markets to support liquidity for based on their risk preferences. Through voting governance, stakers can determine the types and limits of collateral for each pool, thereby limiting the risk to a small range. It also provides stakers with the opportunity to take on higher risks for higher returns. This gives stakers more control over their exposure. For example, they can decide to only provide exposure to mainstream assets like ETH and BTC, and not participate in the market debt pool for long-tail assets like NFTs.

Multi-Collateral Mechanism

V3 has created a universal collateral treasury system that is compatible with various types of collateral. This means that in addition to $Snx, Synthetix will also support other assets as collateral for Synths, in order to expand the market size of Synths.

Through voting governance, it will be decided which assets, in addition to the current Snx, will be supported as collateral. For example, a vote can be cast to allow ETH as collateral. Eight proposals SIP-302 to SIP-310 related to this have already been passed.

Therefore, the new pool and treasury system have three main advantages:

-

Better risk management: The pool is connected to specific markets, so it has specific exposures.

-

Better hedging capability: The pool is connected to specific markets, allowing for precise hedging.

-

Greater range of collateral: Stakers can pledge any assets accepted by the pool, addressing the risk of a single asset.

Perps V2 and V3 Engine

Perps is a decentralized perpetual engine launched by Snx based on debt pool liquidity.

The beta version of Synthetix Perps V1 was released in March 2022 and generated over $5.2 billion in trading volume and provided $18.1 million in transaction fees to stakers without any trading incentives.

The Synthetix Perps V2 proposal was launched in December 2022 and is the current version in use. It reduces costs, improves scalability, and enhances capital efficiency. It also features isolated margin.

Synthetix Perps V3 is scheduled to be released in the fourth quarter of this year. Synthetix Perps V3 supports all v2x functions, plus some new features, such as cross-margin, new risk management features designed to eliminate market biases. This includes price impact measures and dynamic funding rates.

Founder Kain Warwick stated that Synthetix aims to launch the Perps V3 version and its new decentralized perpetual contract exchange front-end, Infinex, in the fourth quarter of this year.

The team stated that Infinex will focus on making it easy for users to engage in decentralized perpetual contract trading. Compared to other decentralized exchanges, it aims to provide a better user experience and eliminate the cumbersome process of signing for each transaction currently required by DEX.

Maintaining Delta Neutral

Perps V2 can effectively match buyers and sellers, and Snx stakers only need to act as temporary counterparties, temporarily assuming asset risks. Incentives will reward traders for keeping the market neutral.

Synthetix incentivizes long and short open contracts in the market to remain balanced through funding costs and premium/discount pricing. The crowded side of the trade will be charged funding costs, while the other side will receive funding costs.

In centralized trading platforms, funding costs are usually charged every 8 hours, while in Synthetix, funding costs are charged in real-time as positions are held. Similarly, trades that cause a deviation in the long/short ratio will be charged a premium, while trades that maintain balance will receive a discount. This mechanism encourages arbitrage traders to actively arbitrage when deviations occur, reducing the risk for LPs in one-sided markets.

Oracle Improvement Plan

Anti-Oracle Latency Arbitrage

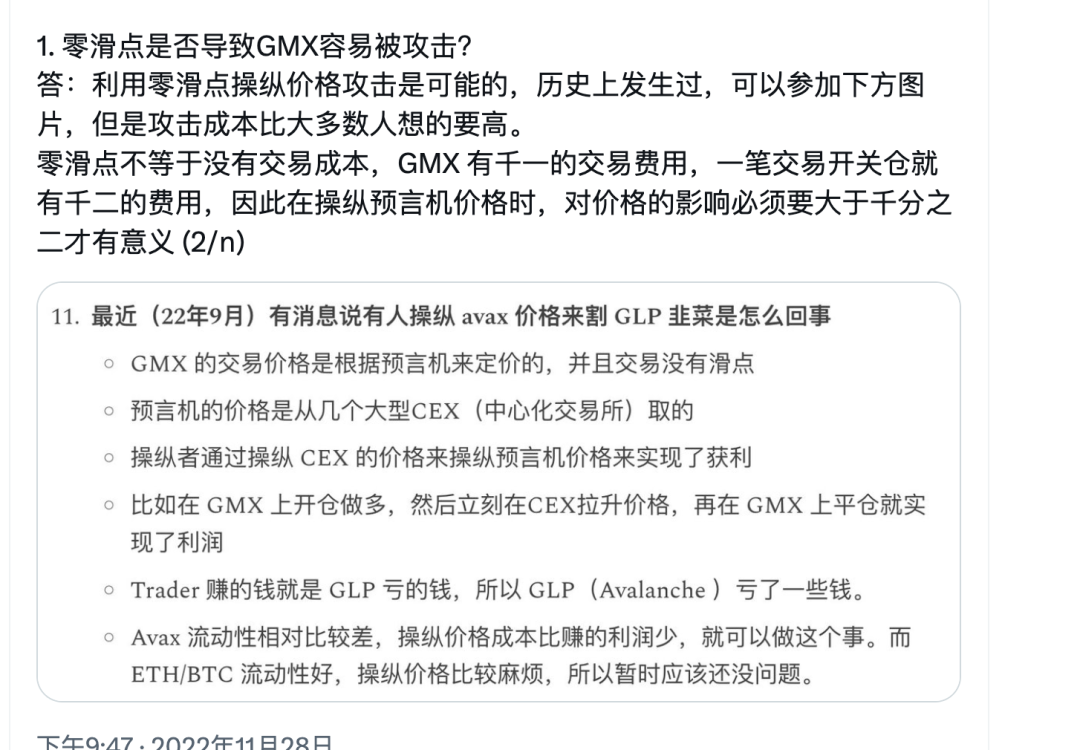

Oracle Latency Arbitrage has been a major reason why previous Dex platforms could not compete with centralized exchanges.

In previous versions of Synthetix, Synths relied on the Chainlink oracle to provide prices. However, the oracle price updates on-chain lag behind the price changes in the spot market, creating the possibility of front-running trades. In the context of zero slippage trading in Synthetix, Snx stakers may face significant losses as a result. For example, if a user observes that the price of ETH rises from $1000 to $1010 in a short period of time, and the Chainlink price is still $1000 at that time, the user can exchange sUSD for sETH at the price of $1000 in Synthetix. After the oracle price updates, without considering fees, each sETH can earn a profit of $10, and the user’s profit comes from the losses suffered by Snx stakers due to front-running trades.

Additional case: GMX, the biggest competitor of Snx, currently adopts this strategy

Source: CapitalismLab

Snx currently provides an oracle management mechanism: market creators can choose from multiple oracle solutions and set custom aggregation, giving integrators more control over the oracles that power the market. The oracle manager provides new opportunities for supporting new markets and assets.

Example: Select the lowest price of spot Bitcoin based on the time-weighted average price (TWAP) of Chainlink, Pyth, and Uniswap.

Synthetix (Snx) has also explored two solutions to address oracle delay arbitrage issues.

1. Hindsight oracle solution: A solution proposed by Synthetix in collaboration with the Pyth team. This solution reduces the possibility of oracle delay arbitrage through asynchronous transactions and configuring delay time. It helps reduce transaction costs for DeFi platforms, making them more competitive.

2. Chainlink’s low-latency data source: Another solution provided by the Chainlink team for Synthetix. This solution aims to provide low-latency data sources to reduce the opportunities for oracle delay arbitrage. This solution has certain advantages over the hindsight oracle solution, such as not relying on third-party executors (keepers) to complete transactions, thereby reducing transaction costs while protecting the data provider’s data privacy.

Pyth and Snx Collaboration Introduction:

Off-chain oracles achieve fast on-chain prices with competitive fees, playing an important role in significantly reducing transaction costs. By solving the oracle delay arbitrage problem, the trading fees for the main currency pairs of Synthetix are currently between 0.2% and 0.6%, comparable to Binance’s advanced VIP users.

Interoperability Solution

Teleporters – Stablecoin-oriented

SIP-311 proposes the concept of Teleporters, which, when launched, can burn newUSD on one chain, transfer cross-chain messages, and mint newUSD on another chain.

-

This means that the newUSD stablecoin can be used on any chain deployed by Synthetix without the need for cross-chain bridges or transfer slippage.

-

It allows the sharing of collateral between liquidity layers across all chains.

-

Can move quickly between chains without challenging verification times, as well as return from L2 to L1.

Interoperable Liquidity Pool

Debt Pool-oriented

-

SIP-312 proposal enables markets and pools on all chains to access the current state of combined collateral on all chains.

-

This means that Perps markets can be quickly deployed on new chains and can leverage the collateral of existing debt pools on Optimism and the Ethereum mainnet.

As mentioned above, through Teleporters and Cross-chain Liquidity Pools, the Synthetix liquidity layer can be expanded to any EVM chain, and new chain deployments can directly benefit from liquidity support from other chains.

Economic Model + Revenue Data

The Synthetix protocol’s revenue comes from several different channels. Mainly from fees generated by perpetual contracts and synthetic asset exchanges, fees from perpetual contract and SNX liquidations, and fees from the minting/burning of synthetic assets. All of the protocol’s revenue is distributed to integrators and SNX stakers.

Integrator Revenue Distribution

Integrators, such as Kwenta, which develop products that integrate with the Synthetix protocol, receive a certain percentage of fees as rewards based on trading volume, paid in SNX: 10% for the first $1 million in fees, 7.5% for fees between $1 million and $5 million, and 5% for fees exceeding $5 million. Integrators are free to decide how to use these fees, such as empowering their own platform tokens.

The Synthetix development team no longer operates the frontend themselves, but instead delegates specific business operations to integrators. Adopting an incentive scheme for integrators enhances network effects and increases the potential for integration into more products, becoming an important DeFi component.

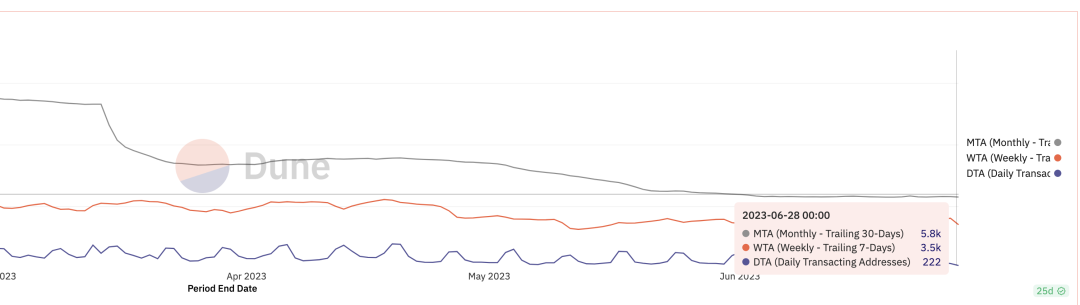

User Growth

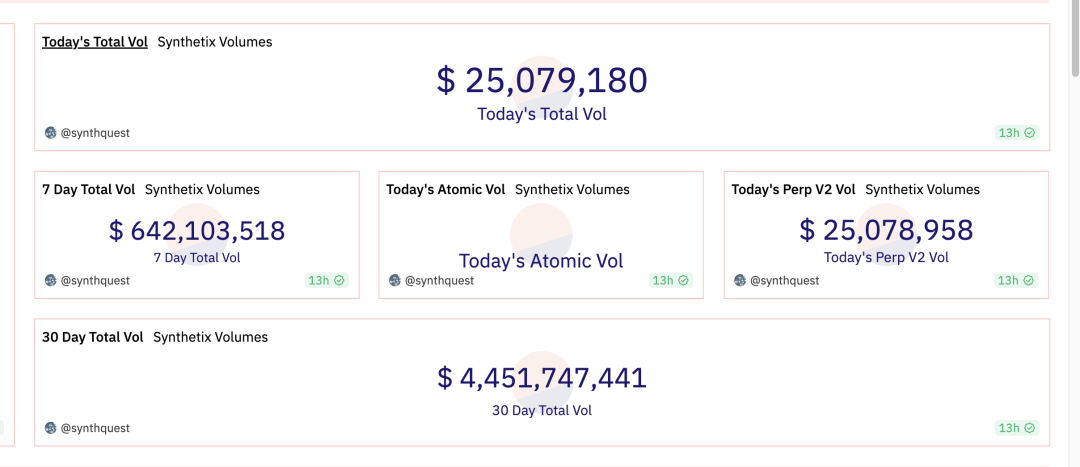

As of the publication date of this article on July 23rd, Synthetix’s Total Value Locked (TVL), monthly trading volume, and fee revenue are comparable to competitors like GMX, but the daily and monthly active user counts are much lower than GMX and Dydx.

PerpV2 Trading Volume

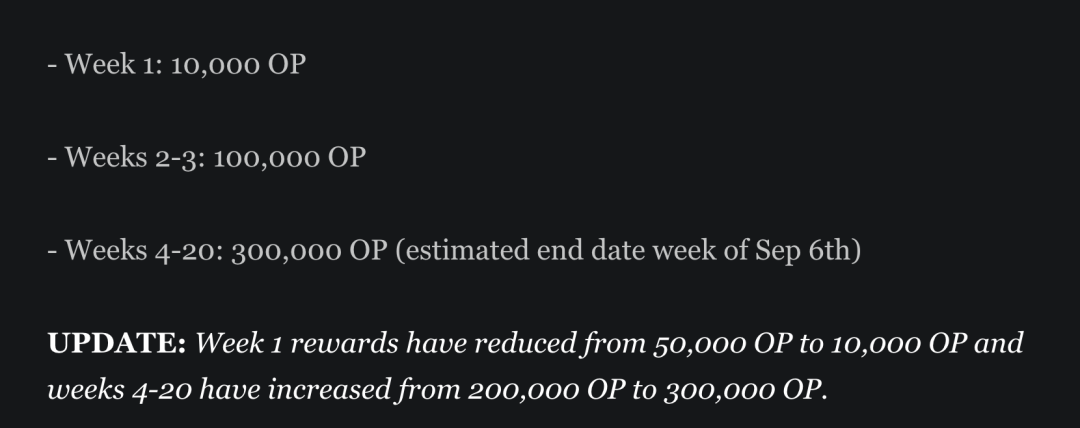

Synthetix Perps received liquidity incentives from the Optimism chain this year, and trading users of Synthetix Perps will receive OP airdrop rewards.

The OP incentives started on April 19th and currently cover approximately 80% of the fees.

According to Messari data, the subsidy incentives have strongly driven trading volume for Perps. The number of user trades and trading volume have experienced rapid growth.

Despite the increase in trading volume, the number of users has not significantly grown according to the trend of on-chain interaction addresses. This means that the largest increase in trading volume comes from increased trading by existing users.

The OP reward program will continue until September 13th, making it easier to understand retention rates after the third quarter.

Trends in Trading User Data

Data Source:

https://dune.com/queries/452148/859385?1+Project+Name_t6c1ea=Synthetix&4+End+Date_d83555=2023-06-28+00%3A00%3A00

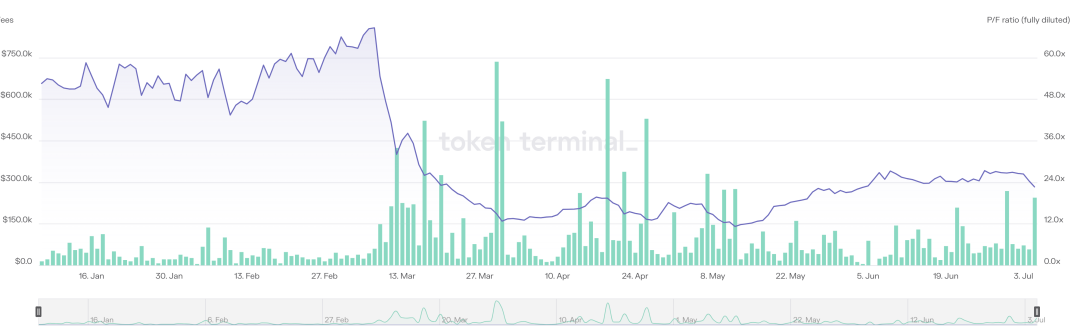

PE Level

As the trading volume increases, it brings about an increase in revenue and an increase in the earnings of stakers. The PE of Snx has returned from the bullish market’s 50X to a more reasonable range of 10x-15x.

Stakers’ weekly fee earnings data

Data source:

https://dune.com/synthetix_community/fee-burn

Exploration of the new token model

Snx is currently in a fully circulating state, with approximately 5% inflation rewards provided to Snx stakers annually.

In August 2022, Kain Warwick, the founder of Synthetix, proposed SIP-276, suggesting that the total supply of Snx be set at 300 million and to stop the issuance after reaching that number. However, the proposal has not been approved yet.

In June of this year, Kain proposed implementing a new Snx staking module in Synthetix V3. This module will simplify the entire staking process, where users only need to deposit Snx without facing market risks or considering hedging needs. Initially, the Treasury Committee will fund this staking pool, but in the future, a portion of Synthetix’s protocol fees may also be allocated to this staking pool. Kain emphasized that this simpler staking method aims to attract more new users to enter the Synthetix V3 system. Currently, this proposal is under discussion and is expected to further increase the Snx staking rate.

Summary:

In the long run, there is a huge space for decentralized derivative trading. The launch of Snx V3 is an important milestone for the Synthetix protocol as it introduces many new features and improvements. These improvements can enhance the protocol’s capital efficiency and security, remove the liquidity cap, and enhance user experience, attracting more users to participate in the Synthetix protocol. After the full launch of V3, it will bring new business increments and valuations. It is expected to be integrated into more products and become an important component of DeFi.

However, the growth of new users is currently slow, and the development cycle required for the full functionality of V3 is uncertain. Under the new token model, the earnings of SNX staking and the retention rate after the third quarter will be important valuation indicators for SNX holders in the short term.

References:

https://blog.synthetix.io/tokenomics-discussion-review/

https://blog.synthetix.io/what-is-synthetix-v3/

Future tokenomics after V3 (in discussion):

– Earn APR without collateralizing SNX (no liquidation risk)

– Still can be used as collateral to provide liquidity to earn extra APR (Risk is optional)

– veSNX?Reference:

SIP-314/315 &https://t.co/amSSmGG8Dp— Jonathan Yuen (@jonathanykh) March 6, 2023

https://www.techflowpost.com/article/detail_11555.html

https://dune.com/synthetix_community/synthetix-stats

Delta

https://www.panewslab.com/zh/articledetails/p4tt0ls1.html

Atomic Swap

https://www.panewslab.com/zh/articledetails/jbyg555d.html

Cross-chain Debt Pool

https://www.panewslab.com/zh/articledetails/tfrnsgg2.html

Dynamic Debt Pool

https://mint-ventures.medium.com/synthetixs-ambitions-a-derivatives-trading-market-with-unlimited-liquidity-a2b79279687b

Multi-collateral

Multi-Collateral Staking: V3 is collateral agnostic, allowing governance to support any collateral to back synthetic assets. This will increase sUSD liquidity and the markets supported by Synthetix. Collateral options will have adjustable variables.

19/28

— Synthetix ⚔️ (@synthetix_io) March 10, 2023

Perps Engine:

https://blog.synthetix.io/what-is-synthetix-v3/

Hindsight oracle:

https://medium.com/@doge_bull/binance-killer-summer-b32cce1c22d3

Cross-chain solution

https://mirror.xyz/cavalier.eth/nOTmVQcole7f0mnqhF93PHO2qbCMm1Y0JAAdiYX9tjU

GMX Oracle Arbitrage Attack Case

1. 零滑点是否导致GMX容易被攻击?

答:利用零滑点操纵价格攻击是可能的,历史上发生过,可以参加下方图片,但是攻击成本比大多数人想的要高。

零滑点不等于没有交易成本,GMX 有千一的交易费用,一笔交易开关仓就有千二的费用,因此在操纵预言机价格时,对价格的影响必须要大于千分之二才有意义 (2/n) pic.twitter.com/MJCro0keQX— CapitalismLab (@NintendoDoomed) November 28, 2022

Earnings data

https://messari.io/report/state-of-synthetix-q2-2023?referrer=all-research

https://mirror.xyz/cavalier.eth/nOTmVQcole7f0mnqhF93PHO2qbCMm1Y0JAAdiYX9tjU

Like what you're reading? Subscribe to our top stories.

We will continue to update Gambling Chain; if you have any questions or suggestions, please contact us!