Author: Jiang Haibo, LianGuaiNews

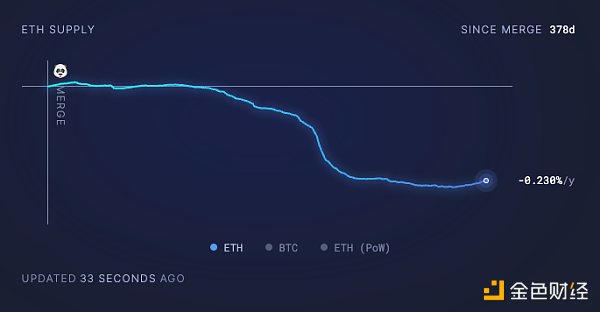

After the implementation of EIP-1559, there was an expectation of deflation in ETH, especially in the case of the overall market rebound this year. The maximum issuance of ETH has decreased by 300,000 coins compared to when EIP-1559 was implemented. However, in the past month, the situation has reversed. Gas prices on the Ethereum mainnet have dropped to single digits (within 10 Gwei). In contrast to the quietness of the Ethereum mainnet, the transaction volume on Layer 2 solutions such as zkSync and Base is high. Is it because transactions on the Ethereum mainnet have been migrated to Layer 2? LianGuaiNews has compared the on-chain situation of the Ethereum mainnet with several Layer 2 solutions including Arbitrum, Optimism, zkSync Era, StarkNet, Base, Linea, and Polygon zkEVM.

Ethereum Data

Gas Price

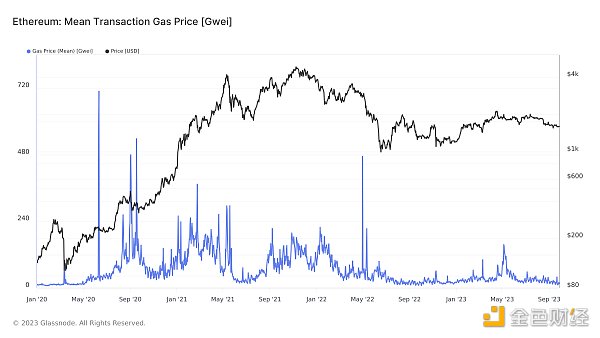

According to Glassnode data, as of September 28th, the average Gas Price for Ethereum in the past few days has been between 10 Gwei and 20 Gwei, close to the lowest value in over three years, which is comparable to the data from May 2020 before the “DeFi Summer” when the ETH price was only around $200.

- Will the launch of ‘Starknet version of GMX’ by Satoru lead to a resurgence in the derivative market?

- Reviewing MicroStrategy’s 28 BTC purchases Is each announcement a signal for a decline?

- Messari 3 on-chain indicators send out Bitcoin bottom signal

Active Addresses

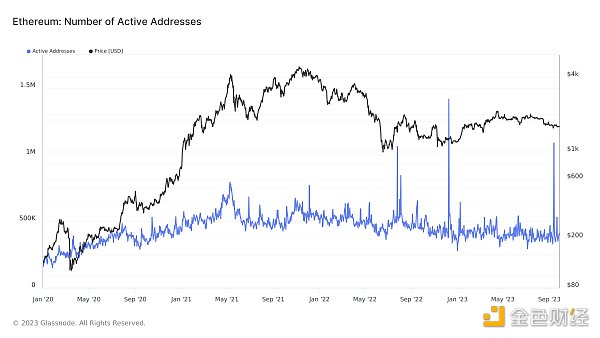

The number of active addresses on Ethereum has shown a similar trend, declining since the market peak in October 2021. Currently, there are about 400,000 active addresses per day, which is almost the lowest value in over three years.

New Addresses

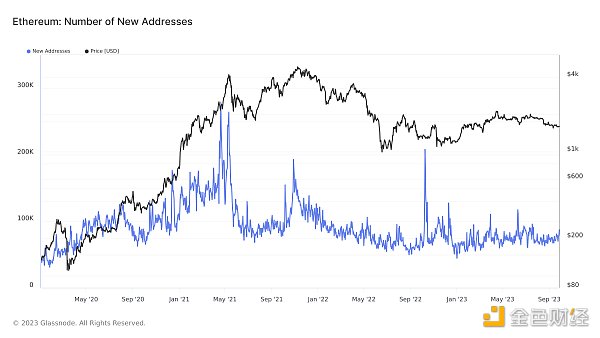

The performance of new addresses on Ethereum is better than the lowest level. Currently, there are about 77,000 new addresses per day, compared to about 50,000 new addresses per day at the beginning of this year.

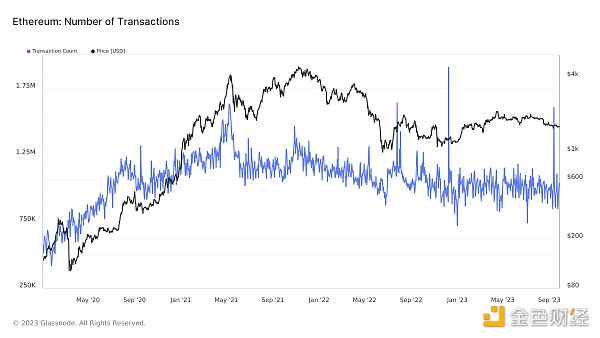

Number of Transactions

The number of transactions per day on Ethereum is also at its lowest point in over three years, with an average of 1 million transactions per day.

All of the above data indicates that there is low transaction volume, few users, and low gas fees on Ethereum at the moment. Even Ethereum co-founder Vitalik has been continuously transferring ETH to exchanges. Which projects are consuming gas and how are they changing?

Sources of Gas Consumption on Ethereum

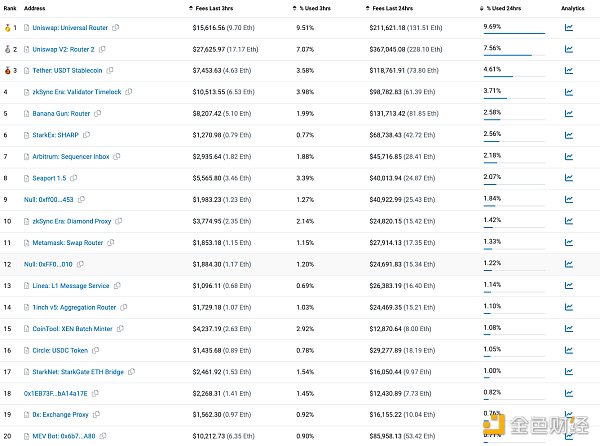

According to Etherscan data, on September 28th, in the past 24 hours, the smart contracts that consumed the most gas were: Uniswap, Tether’s stablecoin USDT, zkSync Era, and the Telegram bot Banana Gun. Among the top 20 smart contracts in terms of gas consumption, there are contracts from 7 Layer 2 projects, including zkSync Era, StarkEx: SHARP, Arbitrum, Base, Optimism, Linea, and StarkNet.

According to Artemis data, when categorizing these contracts, Layer 2 solutions consumed approximately $594,000 worth of gas in the past 24 hours, accounting for 12.5% of all categories. It ranks second only to DeFi and wallet transfers, higher than stablecoins, NFT Apps, infrastructure, cross-chain bridges, games, and other categories.

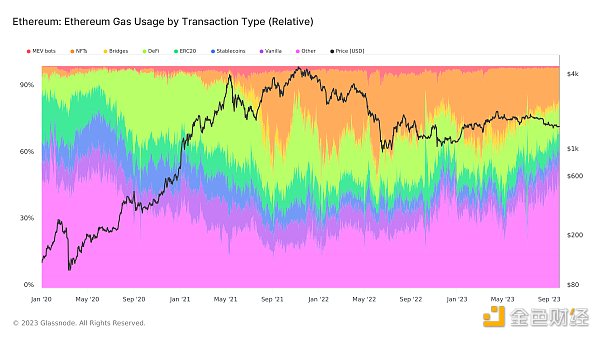

In terms of the changes in the proportion of Gas consumed by various types of transactions, according to Glassnode data, the NFT market has experienced the most severe contraction, with the proportion of Gas consumed dropping from over 30% in early March to the current 15%. The proportion of other categories has increased from 30% to 45%, with Layer 2 included in the other categories.

Comparison of 7 major Layer 2 data

It is evident that Layer 2-related transactions on Ethereum cannot be ignored. Due to lower Gas fees for transactions on Layer 2, is the decrease in Gas on the Ethereum mainnet due to the migration of transactions to Layer 2? Next, LianGuaiNews will compare the changes in Ethereum and several Layer 2 solutions including Arbitrum, Optimism, zkSync Era, StarkNet, Base, Linea, and Polygon zkEVM.

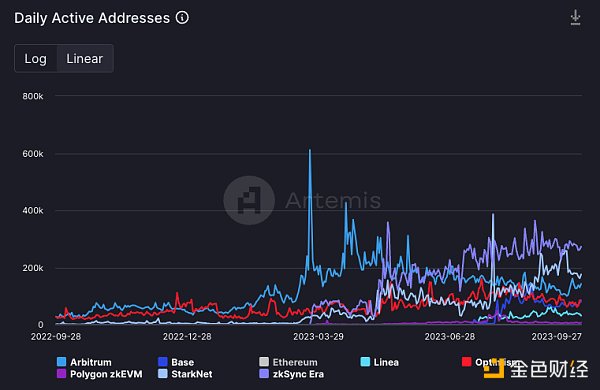

Active addresses

As of September 27, the active addresses on Ethereum and major Layer 2 solutions are as follows: Ethereum – 336,000, zkSync Era – 273,000, StarkNet – 175,000, Arbitrum – 142,000, Optimism – 84,000, Base – 80,000, Linea – 31,000, Polygon zkEVM – 7,000.

Excluding Ethereum, the active addresses are shown in the following chart:

-

The number of active addresses on the Ethereum mainnet still surpasses all independent Layer 2 solutions.

-

zkSync and StarkNet, which have not issued native tokens and have strong expectations for airdrops, have more active addresses than Arbitrum and Optimism, which have issued their own tokens.

-

The number of active addresses on Base has grown rapidly since its launch and now matches Optimism. There are also many applications migrating from Optimism to Base, and the governance and revenue-sharing framework previously agreed upon by Optimism and Base may benefit Optimism.

-

The number of active addresses on Arbitrum surged after the issuance of its native token in March, but experienced a sustained decline starting in April. After Arbitrum announced the issuance of its governance token, the number of active addresses on zkSync Era and StarkNet started to increase and experienced a large-scale growth in May.

-

Although the co-founder of Polygon stated that “there is no rule that projects that have issued tokens cannot conduct large-scale airdrops,” implying the possibility of airdrops on Polygon zkEVM, it seems that it has not attracted enough users, with only a few thousand active addresses per day. Despite Linea’s background with ConsenSys, the number of active addresses is still less than half of Base.

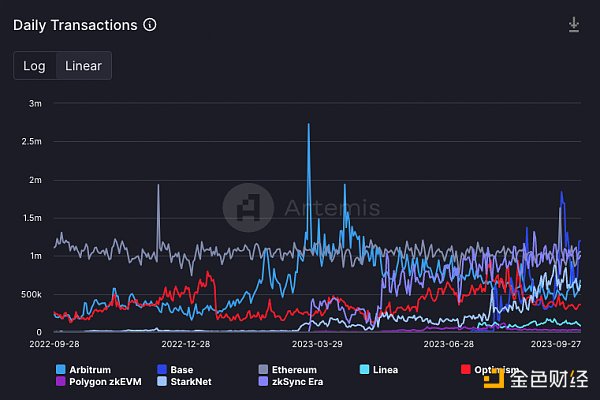

Daily transaction volume

In terms of daily transaction volume, Base has temporarily surpassed Ethereum, with daily transaction volumes as follows: Base – 1.2 million, Ethereum – 1.06 million, zkSync Era – 1 million, Arbitrum – 678,000, StarkNet – 612,000, Optimism – 363,000, Linea – 83,000, Polygon zkEVM – 28,000.

zkSync and StarkNet also show strong performance in daily transaction volume. Base’s transaction volume has consistently exceeded Optimism’s recently, and since its launch in July, Optimism’s transaction volume has shown a downward trend.

The data from Arbitrum and Optimism, which have a richer ecosystem and no airdrop expectations, may better reflect the real demand for Layer 2 at this stage, as both their transaction volumes are declining.

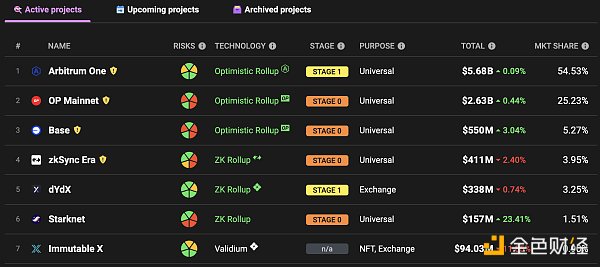

TVL

According to L2BEAT data, the TVL of these 7 Layer 2 solutions are as follows: Arbitrum $5.68 billion, Optimism $2.63 billion, Base $550 million, zkSync Era $411 million, StarkNet $157 million, Linea $61 million, Polygon zkEVM $43 million.

The funds on zkSync and StarkNet are less than 10% of Arbitrum’s, and the on-chain applications are not as rich as Arbitrum and Optimism. However, they have more active addresses, indicating that there may be a large number of active addresses with non-real trading demands on zkSync and StarkNet, possibly belonging to airdrop hunters.

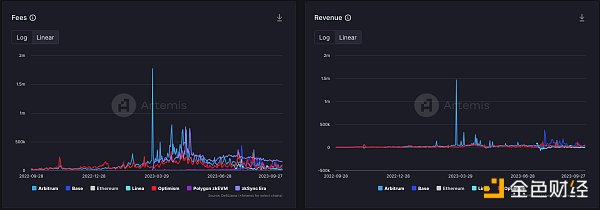

Fees and Revenue

In terms of fees and revenue, Ethereum’s fees and revenue are much higher than those of various Layer 2 solutions. The fees of zkSync Era are still significantly higher than other Layer 2 solutions. Their daily fees are approximately as follows: Ethereum $2.69 million, zkSync $159,000, Arbitrum $94,000, Base $82,000, Optimism $52,000, Linea $18,000, Polygon zkEVM $4,000.

In terms of revenue, their daily revenue is as follows: Ethereum $2.05 million, Arbitrum $50,000, Base $42,000, Optimism $28,000.

The fees and revenue of zkSync Era have not risen with the increase in active addresses in the past few months, possibly due to the decline in gas prices, resulting in a downward trend in fees; the fees of Arbitrum and Optimism have dropped to a low point.

Summary

In the past month, the number of active users, transaction volume, and gas prices of Ethereum have all dropped to the lowest point in over three years, indicating low on-chain activity. However, there are many transactions on Layer 2 solutions such as zkSync and StarkNet, and the daily transaction volume of Base even temporarily surpasses that of the Ethereum mainnet.

After comparing the data of active addresses, transaction volume, TVL, and other metrics of various Layer 2 solutions, LianGuaiNews believes that the data from Arbitrum and Optimism, which have a more complete ecosystem and larger capital, may better reflect the on-chain real demand for Layer 2. The current data is in a declining phase, while the recent growth in data for zkSync Era and StarkNet is more likely to come from airdrop hunters.

Like what you're reading? Subscribe to our top stories.

We will continue to update Gambling Chain; if you have any questions or suggestions, please contact us!