As we approach June, Hong Kong is becoming increasingly active in the field of virtual assets and Web3. According to Bloomberg, Hong Kong will announce that individual investors can trade cryptocurrencies under its new industry rules, and it is expected that individual investors will be able to trade tokens such as BTC and ETH under appropriate safeguards starting from June. This move will mark an important step for the Hong Kong government in opening up cryptocurrency trading and embracing Web3 innovation. In addition, the Hong Kong Monetary Authority announced on May 18 that the “Digital Currency Era” pilot program has also attracted attention.

In the digital age, we urgently need various types of new financial infrastructure that match digital innovation, one of which is the digitization of currency. Although the underlying technology of virtual assets can solve the problem of automatic execution of transactions without trusted authorization, the risks associated with them cannot be ignored, and they cannot be widely used as payment tools or to expand financial inclusiveness. Therefore, currency innovations such as Digital Currency Era have come into the public eye with strong endorsements.

Digital Currency Era is not only the “backbone” and pillar connecting fiat currency and virtual assets, but also a new digital financial infrastructure necessary for the development of Hong Kong’s Web3 ecology and digital economy.

Digital Currency Era = HKD stablecoin? No, there are at least 7 differences between the two

Before the central banks of various countries develop CBDC, stablecoins are the most watched type of digital currency in traditional financial markets. Since CBDC and stablecoins have certain similarities in some aspects, such as both being stable asset types, with almost no price fluctuations, they have obvious advantages over other virtual assets. They can also be used as a new type of payment tool, affecting or even changing the current payment pattern. Therefore, the two were often confused with each other in the early days. This situation is once again playing out with Digital Currency Era and HKD stablecoins.

- Viewpoint: NFTs seem to be making a comeback

- Lookonchain: A Super MEME Coin Hunter with a Win Rate of 63.5%

- Complete Guide to BTC STAMP NFT and SRC-20 Ecosystem for Beginners

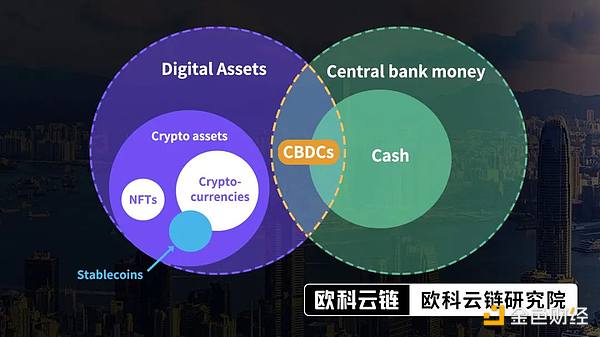

Figure: The position of stablecoins and CBDC in the current monetary system

Chart: Ouke Cloud Chain Research Institute

As the Hong Kong Monetary Authority accelerates the development of Digital Currency Era, many people are now actively or passively confusing Digital Currency Era with HKD stablecoins. However, in essence, Digital Currency Era and HKD stablecoins are two completely different forms of digital currencies.

From the perspective of issuance mechanism, operation mode, and technical features, there are at least 7 differences between the Digital Currency Electronic Payment (DCEP) and Hong Kong Dollar-pegged stablecoins:

-

Issuer: This is the most important difference between the two. The DCEP is to be issued and backed by the Hong Kong Monetary Authority (HKMA), while stablecoins can theoretically be issued by various private institutions or banks. In its regulatory framework for stablecoins, the HKMA has stated that banks can issue their own stablecoins, as long as they meet certain regulatory requirements.

-

Purpose of issuance: The HKMA initially focused on developing wholesale DCEP, but started exploring retail DCEP as well due to increasing international attention on how DCEP could improve cross-border payments and remittances. Its purpose is to explore how the latest technology can effectively address current and future evolving payment needs. On the other hand, the main purpose of stablecoins is to accelerate the development of Hong Kong’s Web3 industry and strengthen Hong Kong’s voice in the field of virtual assets.

-

Credit source: Hong Kong adopts the banknote-issuing system, and the Hong Kong Dollar is issued by three note-issuing banks. Regardless of whether the DCEP ultimately adopts the “coin plan” currently used for issuing Hong Kong Dollar coins and HKD10 banknotes (i.e., the HKMA is responsible for issuing DCEP, and commercial banks exchange US dollars for DCEP), or the “note plan” currently used for issuing Hong Kong Dollar banknotes (excluding the HKD10 banknote) (i.e., banks exchange US dollars for debt certificates, and then issue debt), the DCEP will be a direct liability of the HKMA, and its value will be backed by the credit of the Hong Kong Dollar and the Hong Kong government. Stablecoins, on the other hand, generally cannot be regarded as central bank liabilities, and their credit mainly comes from the credit penetration of the US dollar-Hong Kong dollar and the commercial credit of the issuing institution itself.

-

Legal status: The DCEP is essentially a digital version of Hong Kong Dollar cash and will have the same legal currency status as existing Hong Kong Dollars. The HKMA will promote the revision of relevant legislation at an appropriate time to ensure that all forms of Hong Kong currency are issued on a consistent legal basis. However, stablecoins issued by private institutions cannot obtain the legal currency status of DCEP, and in the short term, they will still exist as a payment tool or a type of digital asset.

-

Technical framework: The HKMA is open to using blockchain technology for the DCEP and has proposed options for a DLT-based technical architecture and design. From the potential use case analysis revealed by the pilot program, it is uncertain whether blockchain technology will play an important role in the issuance and settlement of DCEP, or whether DCEP will ultimately adopt public or private chain technology. However, considering that DCEP is mainly aimed at retail scenarios, and the current blockchain technology has limited processing power for high concurrency, combined with the two-tier operating structure that the HKMA previously revealed may be adopted, it is speculated that in the early stage of DCEP issuance, more secure and controllable private chain technology may be chosen, and a Layer2-like approach may be adopted to solve the usability problem of DCEP: that is, the HKMA and relevant DCEP issuing and operating institutions will build a DCEP alliance as the main body responsible for the issuance and settlement of DCEP on the chain, while transaction and payment-related business links may be conducted off-chain. Based on the issuance and operation mode of mainstream US dollar stablecoins such as USDT and USDC in the market, future Hong Kong Dollar stablecoins may still be issued and circulated on the chain based on public chain technology and networks.

Figure: Progress of global CBDC projects

Source: Citibank

-

Anonymity and traceability. As several Hong Kong fintech researchers have analyzed for the Ouke Cloud Chain Research Institute, considering the balance between user privacy and anti-money laundering and other practical requirements, DigiByte will not directly adopt the issuance model similar to stablecoins and other virtual assets, but will adopt the idea of “centralized management” and “distributed accounting” to achieve a balance between prudence and efficiency as much as possible. DigiByte is expected to refer to the digital renminbi and adopt a hierarchical account model to achieve controllable anonymity, that is, small payments can be anonymous, and KYC is required after a certain amount limit is reached. Li Yinlin, Managing Director of the Investment Research Department of Locke Capital, also believes that the technical characteristics of the traceability of DigiByte will help Hong Kong better deal with various crimes and anti-money laundering activities. Although the Hong Kong dollar stablecoin can theoretically achieve effective anonymity on the chain and will not be restricted in terms of transaction amount, we believe that stablecoins issued by private institutions, including the Hong Kong dollar stablecoin, need to rely on regulatory technologies such as On-Chain AML to balance security and innovation due to compliance requirements.

-

Scope of use. DigiByte will mainly be used in retail scenarios, and due to legal and regulatory restrictions, it will mainly circulate in Hong Kong and related cooperation areas in the future; while the Hong Kong dollar stablecoin naturally has global attributes and will flow freely in public chain networks, it can be applied to many scenarios in the Web3 ecosystem, although it may also be subject to regulation in other countries and regions.

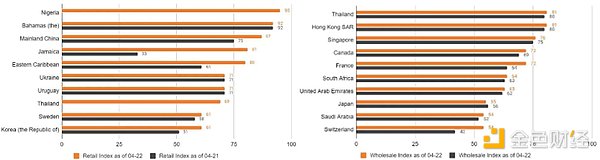

Figure: Retail-type CBDC and wholesale-type CBDC leading the global CBDC index

Source: PwC

Can DigiByte coexist with Hong Kong dollar stablecoins?

Based on the 7 differences discussed above, we believe that DigiByte and the Hong Kong dollar stablecoin cannot be simply equated and will have a certain potential competitive relationship in the short term. However, the possibility of DigiByte completely replacing the function of the Hong Kong dollar stablecoin is not great, because the utilization rate, expansibility, and friendliness of the Hong Kong dollar stablecoin in the virtual asset market will far surpass that of DigiByte, while DigiByte will be in a leading position in value support and reliability. Both have obvious advantages and disadvantages, and the development of DigiByte is a complex systematic work. Referring to the overall progress of the digital renminbi and other retail-type CBDCs, the author believes that it will take at least 3-5 years before it is truly launched. In this process, in the friendly Web3 development environment, Hong Kong may lead the way in the emergence of one or even several Hong Kong dollar stablecoins led by commercial banks and private institutions, which are tied to the value of the Hong Kong dollar and applied to practical scenarios such as cross-border payments and tokenized asset settlements.

However, even if the Hong Kong dollar stablecoin is launched earlier than the digital Hong Kong dollar, it will not affect the Hong Kong Monetary Authority’s original ideas and plans for the digital Hong Kong dollar. After the digital Hong Kong dollar is launched, the digital Hong Kong dollar and the Hong Kong dollar stablecoin can also maintain synergy and cooperation in competition. Possible ways of cooperation include but are not limited to:

Integrating the digital Hong Kong dollar with the already issued Hong Kong dollar stablecoin. The integrated digital Hong Kong dollar will become a synthetic Central Bank Digital Currency (sCBDC), issued by private institutions, responsible for private institutions, but supported by the Hong Kong Monetary Authority with full reserve. Previously, the IMF has mentioned sCBDC many times in its reports and believes that this public-private partnership model enables central banks to focus more on their core functions, which is better than CBDCs that are completely centralized and controlled by central banks.

Figure: Issuance path of sCBDC

Sharing resources and complementing each other’s advantages between the digital Hong Kong dollar and the Hong Kong dollar stablecoin. After the digital Hong Kong dollar is launched, it can choose to use the already established Hong Kong dollar stablecoin system for pilot testing and promotion, accelerating its popularity and scope of application. The Libra Association previously pointed out in the second version of the Diem white paper that after central banks in various countries launched CBDCs, they directly merged with the Libra network to replace other stablecoins in the Libra network with more compliant and secure CBDCs.

These existing forms of cooperation will create imagination space for the future coexistence of the digital Hong Kong dollar and the Hong Kong dollar stablecoin. More importantly, cooperation and coexistence with the Hong Kong dollar stablecoin will also help the digital Hong Kong dollar better adapt to the development of Web3 and make it a “backbone” and pillar between fiat and virtual asset markets.

Relationship between the digital Hong Kong dollar and the virtual asset market from the pilot plan

Recently, the Hong Kong Monetary Authority announced the launch of the digital Hong Kong dollar pilot plan. The 16 selected companies will study the potential use cases of the digital Hong Kong dollar in six categories: comprehensive payment, programmable payment, offline payment, tokenized deposits, Web3 transaction settlement, and tokenized asset settlement.

Figure: List of selected companies and proposed use cases for the digital Hong Kong dollar pilot plan

The launch of the pilot program has attracted widespread attention. Fu Rao, a senior researcher at the Hong Kong International New Economy Research Institute, believes that the launch of the pilot program is a sign that Cyberport has entered the testing phase. After careful study of the participating institutions and potential use cases of the pilot program, the European Cloud Chain Research Institute believes that the following three points are worth noting:

First of all, the types of companies selected for the pilot program are quite diverse, with half of them being commercial banks, and payment giants such as AliBlockingy, MasterCard and Visa also playing important roles. As a well-known blockchain project, Ripple Labs’ selection also fully demonstrates the inclusiveness and openness of the Hong Kong Monetary Authority in exploring the Cyberport Dollar. Referring to the experimental stage of other CBDC projects such as the digital RMB, the author believes that more types of technology companies and payment institutions will participate in the research and pilot process of the Cyberport Dollar in the future.

Secondly, from the distribution of selected pilot cases, potential use cases related to payments are the main direction of this exploration. This is mainly related to the basic positioning and future applications of the Cyberport Dollar, but considering the current diversification of payment methods in Hong Kong, even if the Cyberport Dollar is officially launched, it will not have a significant impact on the Hong Kong payment industry and user consumption habits in the short term. Some scenarios that are more vertical or not covered by current digital payment methods may be where the Cyberport Dollar’s opportunities lie.

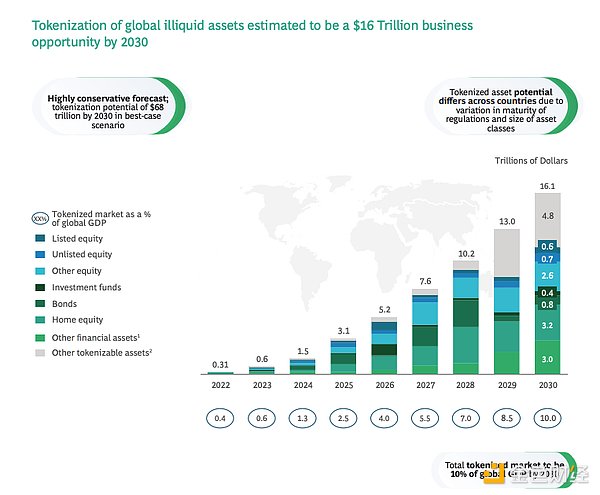

In addition, in the six categories of the pilot program, tokenized deposits, Web3 transaction settlement, and tokenized asset settlement are all closely related to the virtual asset and Web3 industries. Among them, tokenized deposits are viewed by internationally renowned rating agency Moody’s as an alternative to address the shortcomings of stablecoins; Web3 transaction settlement is the use case closest to virtual assets, and may help bridge the connection between the Cyberport Dollar and virtual assets; tokenized asset settlement is expected to accelerate the development of the Hong Kong RWA track, and the European Cloud Chain Research Institute previously proposed that RWAs will break down the barriers between the crypto world and the real world in the next few years, enabling more financial and economic activities to migrate to the chain, and becoming the most important and anticipated track in the development of Hong Kong Web3. These three potential use cases that are highly related to Web3 not only demonstrate that the Hong Kong Monetary Authority is open and forward-looking in the future development direction of the Cyberport Dollar, but also accelerate the integration of the Cyberport Dollar and the Web3 token economy.

Image: Future growth space of tokenized assets

Source: Boston Consulting

Conclusion

Since ancient times, currency has been the core of all economic and social activities, and is also a financial infrastructure with universal social benefits. From the development process of currency, we can see the road of transformation of financial infrastructure in different periods. Today, the virtual asset industry is booming, and emerging technologies such as artificial intelligence, blockchain, cloud computing, and big data are thriving. The Web3 innovation is just in time, and the development of the digital economy has ushered in a new stage. The digital financial infrastructure also needs continuous iteration and change.

Digital Harbor Dollars (DHD) is an important financial infrastructure in Hong Kong to welcome the development of Web3 and the digital economy. It will not only connect the virtual asset market with the real world, but also improve the business capabilities and service efficiency of the existing financial system. More importantly, as a digital financial infrastructure, DHD has the potential to become the adhesive and catalyst of other digital financial infrastructures, strengthening the connection between various financial infrastructure systems and enabling different financial infrastructures to achieve interconnection.

We should not overestimate the role of DHD in the next three years, but we should not underestimate its long-term value for the development of digital finance in Hong Kong and even the world in the next ten to twenty years.

Like what you're reading? Subscribe to our top stories.

We will continue to update Gambling Chain; if you have any questions or suggestions, please contact us!