Author: Spike @ Contributor of PermaDAO

Review: Kyle @ Contributor of PermaDAO

Rethinking the Web3 Creator Economy: From Metaverse to UDL

Defining the Web3 Creator Economy: A Dimension of History

Currently, the state of the Web3 creator economy is not performing well, whether it’s NFTs, GameFi, social media, or other attempts, all are in a silent period. Azuki’s reckless behavior has even caused significant damage to the entire NFT track and creator economy.

However, looking at the entire industry development cycle, the current state of the Web3 creator economy is still in its early stages. This is not just an empty slogan, but a statement based on the experience of comparing the development cycle of the Internet creator economy.

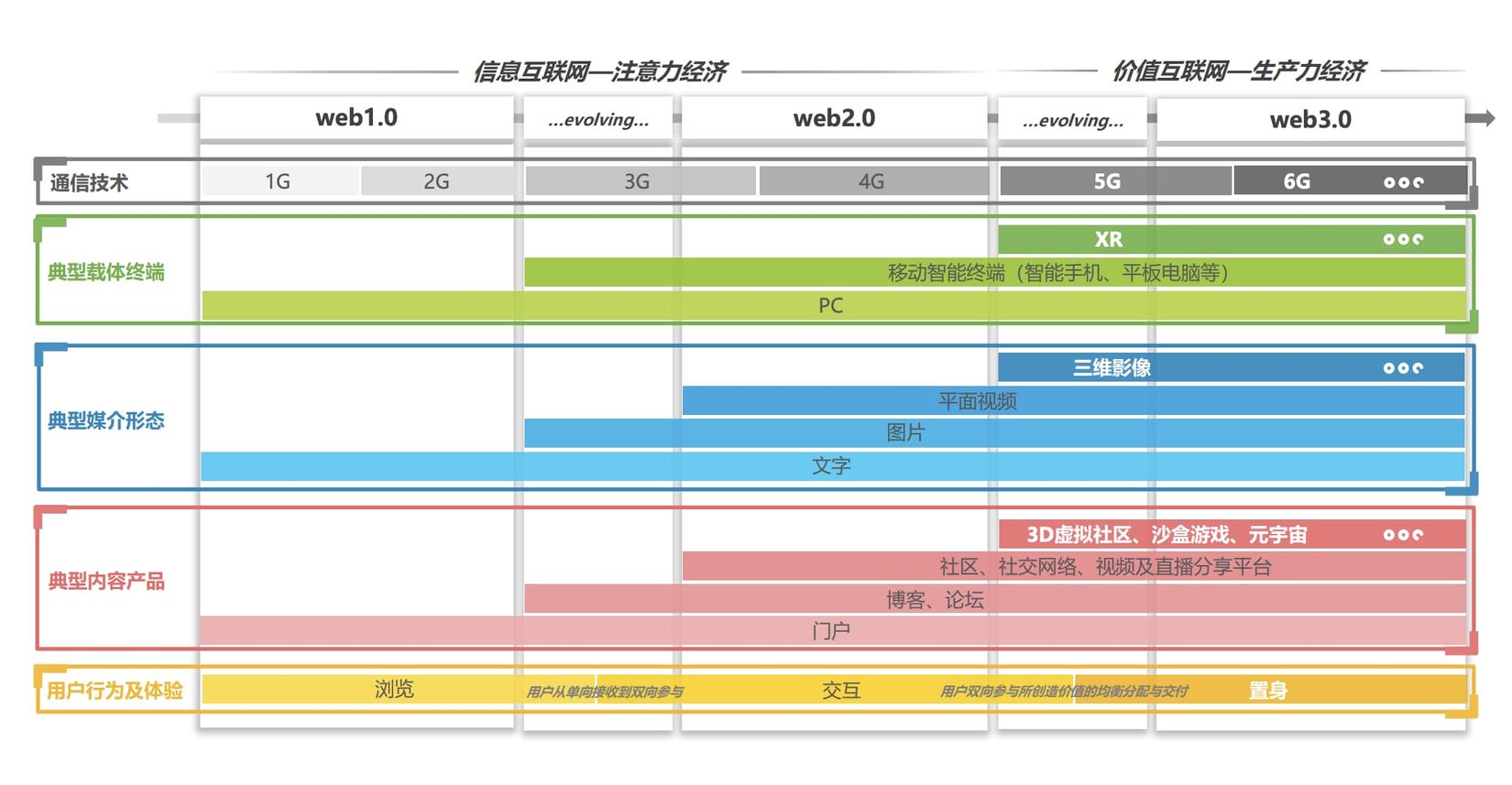

Image description: Overview of the development stages of the internet content market. Image source: https://www.wondershare.cn/document/2022-economic-white-LianGuaiper-of-Internet-creators.pdf

If we say that in the current stage of Web3, we are facing a situation where there are more creators than users, and more gold diggers than audience, then it was the same in the early stages of the Internet. The expensive entry price and electronic devices naturally excluded the participation rights of ordinary users. At that time, the Internet was elitist, and they had a psychological aversion to using the Internet as a channel for monetization.

However, as time progressed to the 1990s, the first wave of the Internet boom in North America, in a sense, completed the initial user education. After the Internet bubble in the early 2000s, everyone’s minds were soaked in the waves of the times. In the eastern world, the tide of going online also signaled that the initial elite group began to break free from the restraints of the system and subsequently accumulated their own capital, forming the basic structure of today’s Chinese Internet.

Afterwards, apart from the iPhone in the era of mobile Internet and TikTok (short videos) in the 5G era, the global Internet landscape has basically taken shape, and eventually, super platforms monopolized everything, including the basic forms of content production and creator groups.

From images, texts, short and long videos, to music, and subsequent innovations, most of them have changed the production relations, such as blockchain breaking the platform monopoly, or AI helping people improve production efficiency, but the basic forms tend to be stable.

From this perspective, the Web3 creator economy can be defined as changing the current situation where creators’ income is heavily deducted by platforms, and breaking the censorship of creators’ content, giving creators creative freedom, with the support of blockchain technology.

In fact, even within the Web3 creator economy system, there have been plate rotations, for example, the initial NFT music market hoped to change the issue of centralized platform deductions, but NFTs have not fully played this role and have instead overshadowed the speculation of “small pictures”. Things are never perfect.

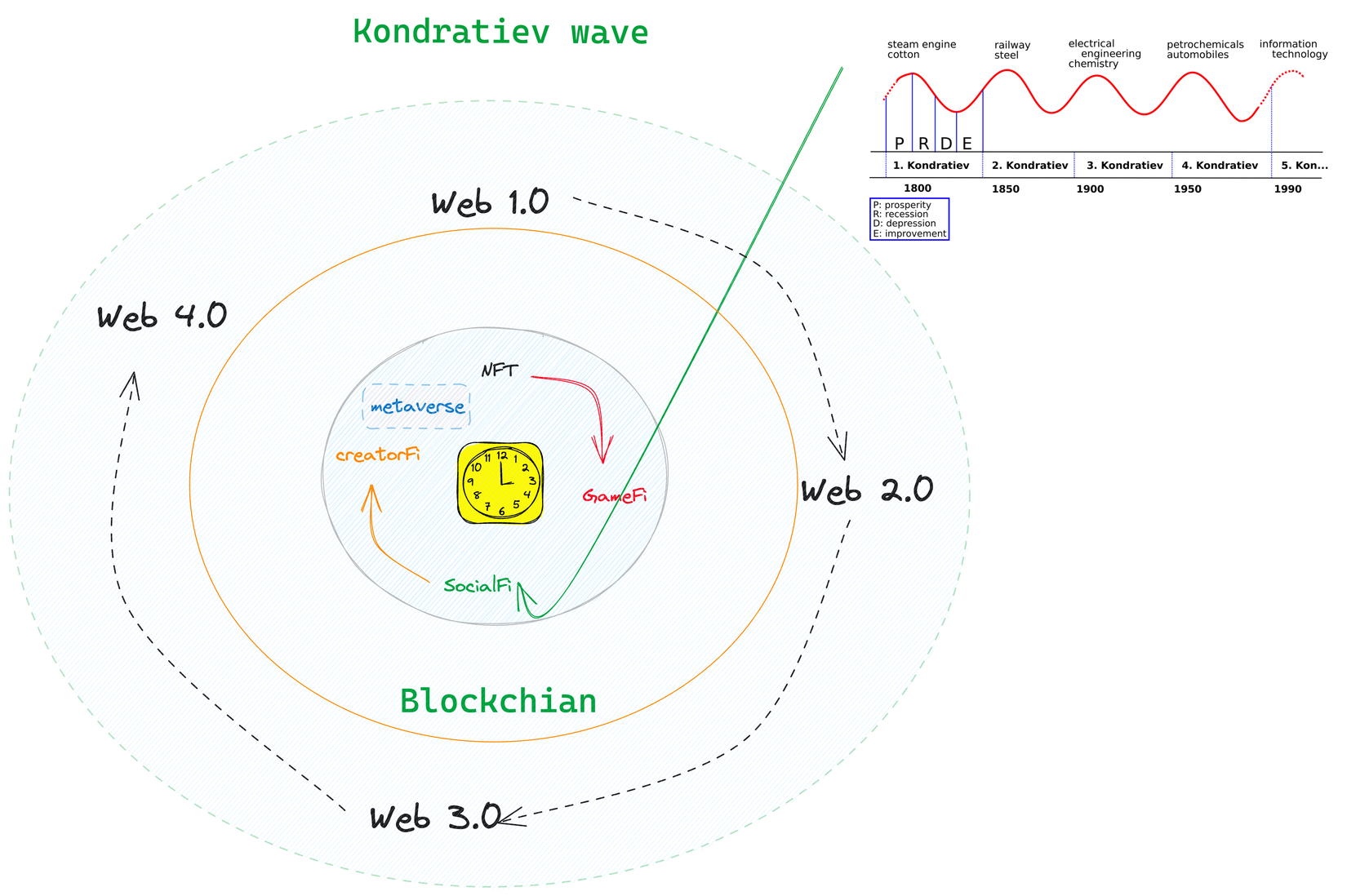

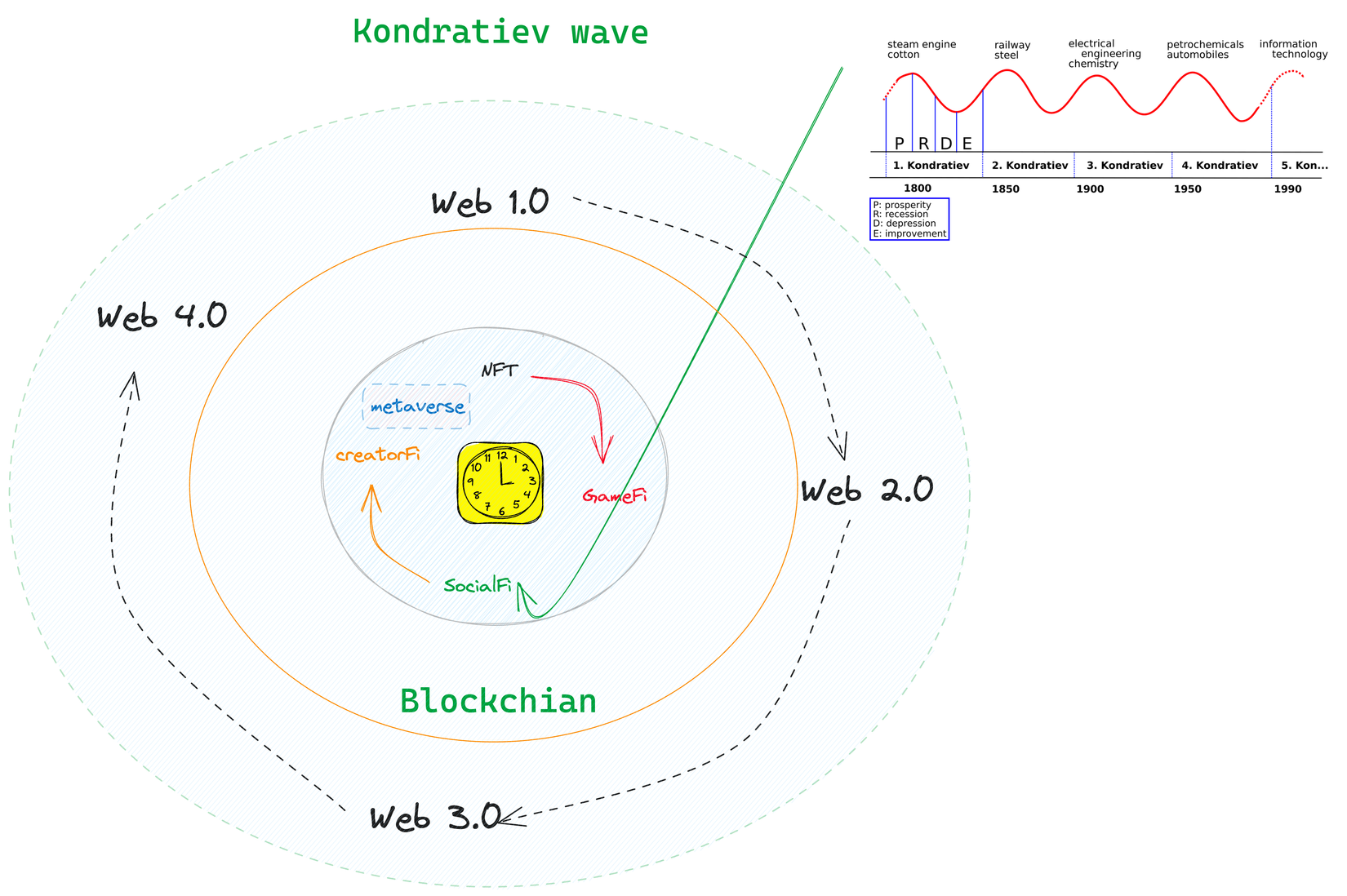

Superposition and Uncertainty: Can the Metaverse Become a Reality?

From a macro perspective, we are in a state of superposition between the Kondratiev wave and the development of the internet. It has been a long time since humanity has had any fundamental scientific innovation, and everyone hopes that superconducting technology will become a reality and break free from the current stock competition.

After experiencing the stages of gathering society, agricultural society, and industrial society, humanity entered the information society predicted by Alvin Toffler in “The Third Wave”. Since the 1990s, the development of the internet has made us feel like we are already in it. From Web1.0 to Web2.0, we have witnessed the persistence of platform monopolies and the stifling of human perception by information cocoons.

The reason why the information society is still considered the future is that the scale of the digital economy is not large enough, and industrial production capacity is still an important criterion for determining national competitiveness. Toffler’s statement that “information becomes the most important production factor” is still not a reality, at least not entirely.

The emergence of the concept of the Metaverse has the potential to truly trigger a transformation in the social form of humanity. According to the Kondratiev long wave cycle (which believes that there is a long-term fluctuation with a length of 48 to 60 years and an average of 50 years in the development process of capitalist economy, generally understood as the result of collective human behavior), the vibrant computer technology that developed after World War II has reached the time node for upgrading.

Coincidentally, after the rebranding as Meta, the craze for the Metaverse has reached its peak, covering applications such as VR, games, social media, and even blockchain technology and cryptocurrencies. In short, we are seeing the embryonic form of a new format that goes beyond existing internet platforms, and this will fundamentally change the overall pattern of the creator economy.

Image Description: Web3 Creator Economy Cycle, Image Source: Arweave SCP Ventures

The Metaverse for Creators: A New Container

Looking back at the origin of the concept of the Metaverse, it is often mentioned that the science fiction novel “Snow Crash” introduced it. In this novel, the “Metaverse” is actually a virtual human living environment, where corporations and organizations are responsible for street construction, and individuals are part of the economic system. The librarians can be seen as AI NPC characters, and the various architectural spaces can be seen as virtual land.

Inspired by this, Second Life was launched in 2003 and basically realized the fantasy in Snow Crash. It even issued its own Linden Dollar, which could circulate within the game. There are now 6,000 events held in Second Life every day, and its GDP reached $500 million in 2015. From a gaming perspective, being able to exist for 17 years and still operate stably is considered highly successful.

However, compared with the rising star Roblox, Secondlife can only be said to be out of time, after all, Roblox is the biggest contributor to pushing the concept of the metaverse into the mainstream world. Roblox was founded in 2004 and launched its game of the same name in 2006. Currently, it has nearly 40 million daily active users (DAU), with a peak concurrent user count of 5.7 million, and over 8 million developers.

In March 2021, Roblox first mentioned “Metaverse” in its IPO prospectus and defined eight elements of the metaverse: Identity, Friends, Immersiveness, Low Friction, Variety, Anywhere, Economy, and Civility.

The biggest feature of Roblox is that it maximizes the use of MOD (Modification) mode. Roblox provides an extremely customizable game editor and environment, allowing users to customize their game experience and create their own virtual world.

Technology is a natural product of human evolution. The elements defined by Roblox itself are ambiguous and more of a directional guide rather than a specific implementation path. We need to continue refining the technical points.

Just like Bitcoin and blockchain, they are not the result of technological breakthroughs. Similar to how James Watt improved the steam engine, P2P, cryptocurrency, anonymous mechanisms, and PoW consensus mechanism all existed before, but it was Satoshi Nakamoto who combined them to develop Bitcoin and truly achieved a decentralized economic system.

The same goes for the metaverse. The technologies needed for the metaverse, such as XR (VR/AR/MR), 5G, edge computing, and blockchain and NFT, already exist. However, the metaverse truly integrates and envelops them into a unified concept.

- VR/AR: The entry and key path of the metaverse. Currently, it is mainly focused on visual and auditory aspects, but it will continue to advance in terms of touch, temperature, and motion. The global market size of virtual reality technology was $12 billion in 2020, with China accounting for 55% of the market share. Currently, VR accounts for 68% of the market share, and AR accounts for 32%. The global shipment volume reached 5.12 million units.

- 5G, WiFi 6, cloud computing, edge computing: The linking channels between people in the metaverse. It will achieve ultra-high definition, dynamic rendering, and preloading, achieving a never-offline effect. According to Huawei’s report, humans will overcome dizziness only when the resolution of a single eye reaches 6K and the frame rate (FPS) reaches 90Hz. At this time, a bandwidth of 1.4Gbps is required, and the ideal state is 16K@180FPS. However, the global adoption rate of 5G was only 10% in 2020, and among the top 10 countries, the average home internet speed is only 200Mbps, which can only support 2K@90FPS.

- AI, visual development kits, all-in-one development platforms: Reduce development difficulty, such as Nvidia’s Omniverse all-in-one development platform.

Roblox consists of three parts.

- Roblox Studio: A modular game development engine for developers, with 1/5 of its players being developers and creating user-generated content (UGC) independently;

- Roblox Cloud: Deployed in 21 regions worldwide with 21,000 interconnected servers, capable of processing 12 million requests per second;

- Roblox Client: Targeting users, including iOS, Android, PC, and Xbox, with the power of UGC, there are currently 20 million games available.

In terms of user composition, it is definitely skewed towards young people and can attract users to engage in social interaction within it, completing the traffic loop.

- Age: 9-12 years old accounts for 29%, 25 years old and above is only 15%, 5-24 years old accounts for about 70% of DAU;

- Region: North America accounts for 32%;

- Devices: 72% on mobile devices;

- Gender: Balanced;

- Usage time: Daily usage duration per user: 153 minutes;

- Social interaction: Average of 61 messages per day, while WhatsApp is 50 messages.

In terms of game production, it already has the ability to create popular games with high retention rates. Adopt Me! reached a peak of 2 million concurrent players. 0.9% of game playtime exceeds 10 million hours, and there are 1,504 games with over 1 million hours of playtime. The top 10 games account for 37% of total game playtime, games ranked 10-100 account for 28% of playtime, and games ranked 100-1000 still occupy 25% of playtime.

In terms of the economic model, it is heavily focused on developers. In the 12 months of 2020, 0.5% of development and creator revenue exceeded $10 million. In 2020, mobile game revenue exceeded $1 billion, with a revenue split of 25% for the platform, 24.5% for developers, 26% for platform consumption costs, and 24.5% for Roblox. The $250 million loss in 2020 was due to the rapid increase in the revenue split for developers. In Q1 2021, the total developer revenue was $120 million, and there were nearly 800 developers who earned over $30,000. The company expects to share nearly $500 million with the community in 2021E.

We can see that the four key success factors are: young people, economic incentives, social interaction, and open platform, and only Roblox satisfies all four of these factors.

From this perspective, I think we can understand Meta’s impulse, as well as the popularity of MANA/SAND at the time. Land economics and virtual real estate are all imitations of Roblox, and then naturally extended to GameFi. We all believe that this will change the current gaming landscape.

However, in the present of 2023, nothing has changed.

Take the development of the metaverse platform as an example, the current problems are mainly due to poor development reusability, high technical integration difficulty, and high costs.

- Apple, Huawei, and Microsoft have different standards, and NVIDIA Omniverse requires hardware support;

- At the hardware level, chips are monopolized by Qualcomm, and the hardware devices (HoloLens, HTC, Oculus) are divided into three;

- At the system level, Facebook, Steam, and Sony all develop their own, Huawei has self-developed AR Engine;

- At the service level, the development platforms and distribution platforms are not unified, and each hardware has its own ecosystem;

- At the application layer, it is divided into 2B/2C, with 2B being smart education and healthcare, and 2C being streaming media and games, with fewer supported games;

- The market share of hardware, content, software, and services: 37%, 36%, 19%, and 8%, but the overall market size is small. Facebook’s Oculus Quest 2 is expected to reach 10 million units, but before that, economies of scale are difficult to achieve, and costs remain high.

Outlining the Characteristics of the Creator Economy

The previous boom was not entirely without value. At least we can summarize the characteristics that a successful creator economy platform should have:

- Open system and closed-loop economy: In a virtual world open to everyone, economic activities should be kept within the system as much as possible. The mainstream world values its openness, and the current trend of platforms staking their claims undoubtedly has strong appeal. The crypto world hopes to achieve economic circulation through the use of NFTs.

- Virtual interaction and real emotions: Non-physical interactions can trigger genuine emotions in humans. The further development of XR devices presents the possibility of replacing real-life human interactions.

- Asynchronous loading and synchronous rendering: Massive multiplayer collaboration and simultaneous online presence require massive amounts of network bandwidth. However, interactions need to be presented simultaneously, and user devices have varying performance capabilities. This calls for asynchronous loading and cloud rendering, with local devices only responsible for rendering the results.

- Public platforms and private creations: New platforms must have a public nature. Building on the blockchain eliminates centralized management organizations. However, specific scenes are hosted in various “venues” and “streets,” which are typical UGC content.

If we want to achieve the above points, following the old path is of no value. We need to redefine the rules of action, at least considering the following points during the design:

- Economic system: From B2C and C2C transaction forms to NFTs, truly realize the operation of a decentralized economic system, at least reducing the share of channel commissions.

- Operating infrastructure: Transitioning from centralized internet platforms to blockchain platforms, achieving decentralized data storage. The goal is to achieve “one login, network-wide operation,” while protecting personal privacy and breaking down the current isolation of the internet.

- Short term: The crypto economy requires the creator community to educate users in a new round, and creators also need the crypto economy to help them escape platform exploitation.

- Medium to long term: Establish blockchain as the underlying operating infrastructure for the creator economy, enabling individuals to control their data. Only when the underlying infrastructure is built on the blockchain can we avoid the issue of platform monopolies.

So far, we have outlined the basics of the Web3 creator economy. In the following sections, we will analyze typical cases, all based on Arweave’s solutions, which are stable and have long-term viability, unaffected by market conditions. We believe that these practices will become models and examples for the future Web3 creator economy, completing the revolution of the existing creator system.

Case Study: Creation, Socialization, and Standardization

Thanks to the advancement of computer technology, the objects that people can create are no longer limited to text. The barriers to entry for games, music, and videos are decreasing, and the creator community is becoming more mainstream, eliminating the elite nature of the early internet era and truly democratizing the right to create.

In the social stage, there is a new change, which we can call the migration of the on-chain data production paradigm – the transformation and addition from DeFi data to social data. Although social data is a rich mine waiting to be explored, its direct economic value is not as high as DeFi. Therefore, storage-based public chains such as Arweave are the most suitable place to accommodate it.

Finally, Arweave proposes UDL (Unified Data Standard), hoping to unify the future on-chain data format, create a universal standard similar to URL, truly unleash the potential of creators, and solve their worries from a technical level.

The clever use of economic incentive mechanisms and the self-organization of open worlds

“二创” is not a new concept. At least in the 1980s, a RPG game called “Ultima” provided players with an open world map. A highly accomplished game in this aspect is “Elite” in 1983, where players can play as astronauts flying spaceships, travel through the universe, complete various tasks, and their behaviors start to influence the game ecosystem.

Currently, game “二创” can be divided into five types: 二创, MOD, home, sandbox, and UGC.

However, there is a problem here, which is also the irreplaceable value anchor of the encrypted economy in the metaverse – the self-organization of UGC content production. The previous UGC content had a big problem of unstable profit expectations and unclear ownership, such as Blizzard taking the copyright of “Warcraft 3” MOD for themselves.

By introducing the NFT economic incentive model, it will promote clear copyright and value transmission mechanisms. The ownership of game items obtained by players is clear, tradable, and storable, eliminating the problem of copyright infringement in 二创. In addition, players can develop their own gameplay within more developed games, and the income is also very clear. There is no high channel fee for centralized platforms, while Steam and App Store charge 30%, Microsoft and Epic charge 12%, and in China, it is generally around 50%.

A typical example is the popularity of Axie Infinity in Southeast Asia. Many Filipinos have achieved a “play-to-earn” mode through Axie Infinity during the pandemic. The minimum wage level in the Philippines is $200, and the average amateur Axie Infinity player can earn more than $1,000 per month by earning an average of 200 SLP (Small Love Potion) per day. This is several times their own work income and can even exceed the minimum wage level. The players’ activity also promotes the prosperity of land sales and the market, which can be understood as the prosperity of trade driving the rise in land prices.

In addition, the P2E mode is also a counterattack against digital labor. The theory of digital labor believes that centralized platforms exploit the data generated by users, and even games become the “playbor” of platforms. The P2E mode of the encrypted economy is not only the evolution of game creation models, but also the reshaping of economic systems.

Next is the necessity of free creative content. The reason why UGC is used to generate content instead of traditional producers providing an open-world model is mainly because the production capacity is clearly unable to keep up with the time consumption of gamers. Currently, it takes an average of 5 years for a thousand-person team to create content for a AAA game, but players can experience all of it in just 189 hours. For games like “King of Glory” that have been profitable for over 5 years, basically only one in a thousand remain.

Therefore, if a massive number of users and a large amount of time enter the metaverse, UGC is the inevitable choice, as no organization or individual can develop the entire environment. Moreover, this UGC is not disorderly, but will give rise to new organizational forms – DAO. For example, YGG formed the Axie team to play the game and share profits, with currently over 2000 members and fundraising of millions of dollars.

Furthermore, platforms like Mirror are closer to the most traditional creator economy, namely the writing paradigm. Unlike Ethereum and other transactional information, Mirror’s data is in text format, which will then be uploaded to Arweave for permanent storage.

One can understand it this way: Mirror does not solve the problem of data portability, but it does solve the issue of permanent storage for text. In the previous creator community, which has gone through various eras and platform updates such as forums, blogs, and microblogs, the data on these platforms frequently encountered problems of loss. Although it can be solved through downloading and other methods, it creates difficulties in accessibility.

However, after uploading to Arweave, the content can be accessed anytime and anywhere using the same link. Even if the Mirror project ceases operation, it will still be stored on Arweave for at least 200 years.

Although platforms like Mirror are more friendly to creators, they are still too professional, and UGC content requires a massive number of producers. Therefore, the DAO model is obviously more suitable for the access of ordinary users. For example, PermaDAO is centered around the theme of strangers co-building. Content guilds on PermaDAO can engage in writing, translation, and content operations. After statistics on the production data, it will be stored on Arweave through blockchain, forming an immutable ledger.

Using UGC X DAO to generate content will not only promote the growth of new organizational forms but also facilitate the operation of new economic models.

Social Data: The On-chain Migration of Real-world Relationships

This stems from the exploration of human social identities. Humans are social animals and have an identity system of role sets. They can express themselves according to different social roles, such as in the family, workplace, and digital space. In a sense, this is the most logical process. Whether in virtual spaces or real-life scenarios, we always need to communicate with specific identities, and with the help of digital tools, this is the most realistic and feasible migration path.

We are able to map relationships because an increasing number of humans have existed in a networked society since birth. For Generation Z and post-2000s, the internet is a given, unquestionable existence, just like water, air, and screens.

Overall, we are evolving along the logic of digital immigrants, digital twins, and digital species, and the intuitive understanding of relationship mapping is to project real-world relationships into the metaverse, which is virtual interaction + real behavior logic, such as video conferencing, live streaming, and video socializing, enabling real-time contactless interaction. Digital twin is already in progress.

Secondly, the reason why migration is possible is because people’s activities are increasingly shifting online. The NBA Finals had 7.5 million viewers, and the League of Legends World Championship Finals had 46 million viewers. The total expenditure on video games was $174.9 billion, a 19.6% increase compared to the previous year, which is twice the total revenue of the film and music industries during the same period.

The pandemic period also marked the first highlight for online or metaverse products. Roblox hosted Lil Nas’ online concert, Fortnite hosted DJ Marshmello’s online music festival, UCB held graduation ceremonies in “Minecraft,” and Fortnite organized a Travis Scott concert with a peak of 12.3 million players online simultaneously.

People’s social activities will also tend to shift online with the changing consumption scenarios. For example, Tencent is secretly developing a social product called “M8,” which will be led by the QQ team. It is positioned as a map-based virtual social product targeting young people’s social needs. If traditional social products are striving to prevent external disruption, why don’t native blockchain-based social products have a chance?

In fact, if we break down blockchain-based social interactions, at least two aspects of behavior shaping are needed – online image shaping and offline influence migration:

- For example, the classic Avatar virtual online image. As early as 2021, Epic launched the MetaHuman Creator to help humans create virtual appearances and motion animations. The AI-powered face sculpting system is already extremely close to real human faces.

- The second is the migration of offline influence, such as Damus, created by Twitter founder Jack, which caused a sensation at one time. Meta’s social product Threads leverages Instagram’s account system.

We can speculate that if a sufficient number of people and enough time are spent in the blockchain space, the product with higher economic value will undoubtedly be social data. This will serve as proof of people’s activities, and this is also the reason why products like Lens can raise $15 million in funding.

It’s strange for a social product to charge fees, as it emphasizes the concept of an open platform. However, paying for data storage space is in line with real-world behavior logic, and it is easier to attract most people to migrate if it can be done at a low cost.

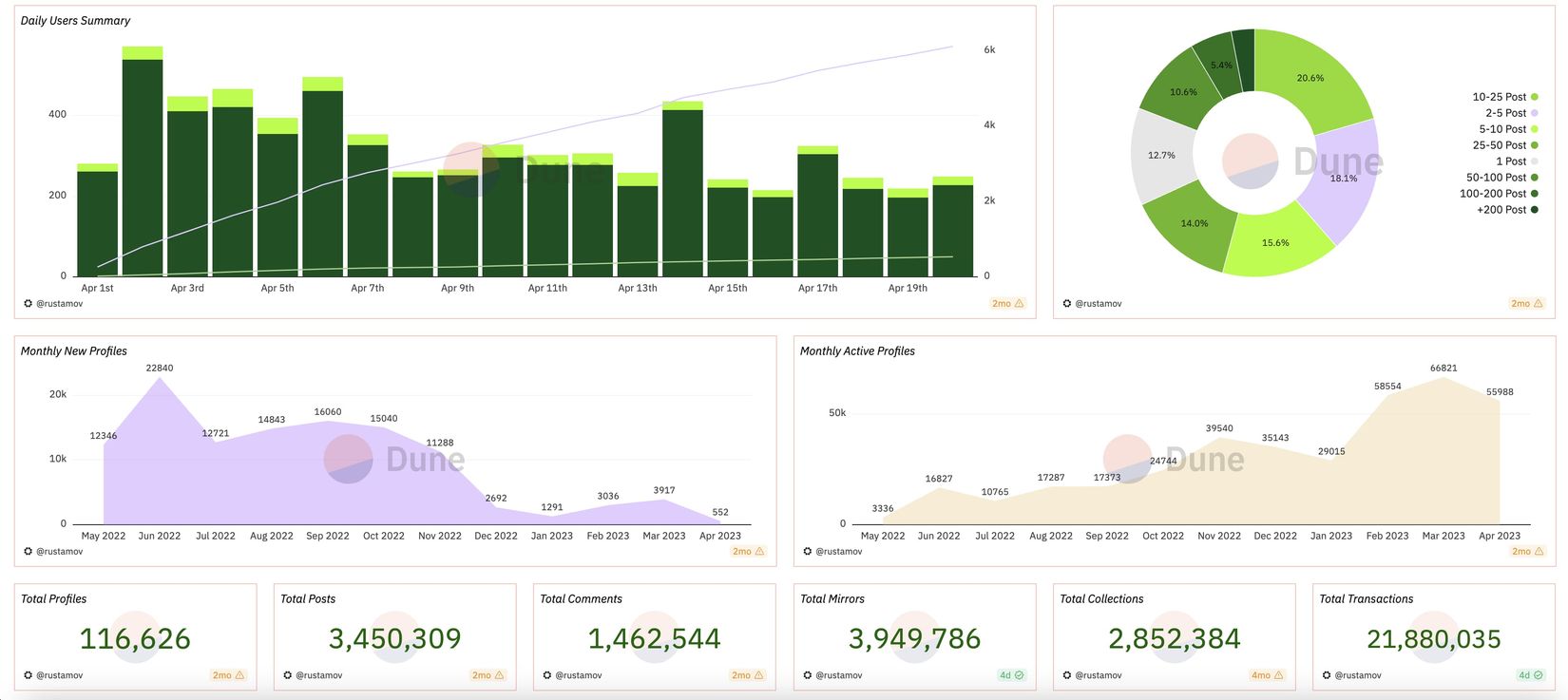

Image caption: Lens data image source: https://dune.com/rustamov/lens

After Lens upgrades to Momoka, its various functions will be decoupled, similar to the concept of modular blockchain. Lens data will be hosted on Arweave for permanent storage, and Bundlr will be used as a data rollup tool. In nearly 500,000 transactions, data storage services cost less than $180, supporting the daily use of 6,000 users. The cost of a single transaction is less than $0.0004, which is enough to support large-scale promotion and use.

As mentioned earlier, social data needs to be classified and organized in a complex way to reflect the interpersonal relationships on the chain, and then undergo data mining and organization to carry out complex operations such as monetization. Arweave has already reduced the cost of data storage to a range that most people can accept. Next, it is necessary to unify and organize the data according to a standard paradigm.

Monetization of Content: $U and UDL

As McLuhan said, “the medium is the message.” The greatness of an era lies not in the content of its dissemination, but in the use of the communication tools and the impact they generate. The couch potatoes of the television era and the internet-addicted teenagers of the internet era are all people’s stress responses to new media. If people use social media intensively beyond their basic physiological needs, they are likely to be considered as having mental illnesses.

In fact, the current market share of blockchain content creation, social products, and more mainstream applications such as DeFi and metaverse is still very small in the global market. Even during the peak of the blockchain bull market in 2021, when the global pandemic situation was not good, blockchain still has a very large development space compared to other sectors.

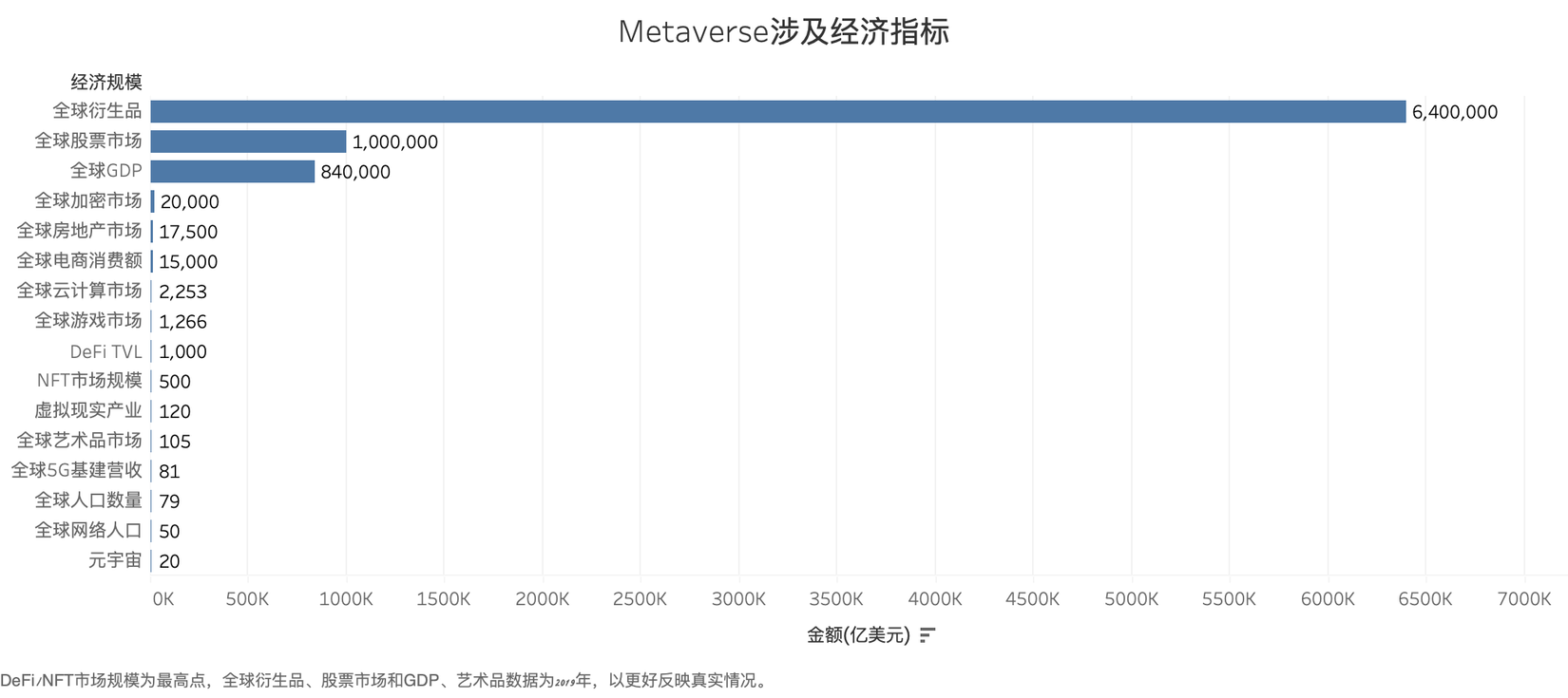

Image description: Scale of major economic indicators, image source: Arweave SCP Ventures

For the Web3 creators’ economy at the current stage, the main problem is the lack of channels for monetizing “content.” This is not an alarmist statement, but a result of the current market size being too small. According to a report by Blockchain Live, “66% of creators consider online content creation as a side job, and only 6% of early-stage creators earn more than $10,000. 35% of creators’ income is not enough to make a living, and 59% of people have not monetized their content at all.”

According to iResearch’s statistics, “in terms of fan distribution, among creators operating personal accounts, the majority are long-tail creators with less than 50,000 fans, accounting for 83.2%.” These two points show that the problem of the current Web3 creators’ economy lies in the importance of traffic. Although traditional centralized platforms have many drawbacks such as monopolies, inequality, and privacy violations, they can indeed capture traffic and support top creators to form a prosperous content ecosystem.

However, blockchain cannot adopt such methods. Technically, it is impossible to capture user data. Therefore, it is necessary to start from the incentive level to encourage more native creators, and this is also the cleverness of Arweave’s introduction of the $U token.

$U is a token issued based on Smartweave, and its name is derived from the abbreviation of “Unit.” The relationship between AR and U is similar to that between ETH and WETH. AR plays a role in paying storage fees within the ecosystem, but it lacks the ability to be called in smart contracts. $U will have stronger versatility and programmability, and will play a role in communicating with the Arweave developer ecosystem.

When users pay storage fees using AR Pay, they will automatically receive returns in $U tokens, which can be directly traded. This is equivalent to receiving a discount on transaction fees. The more data users store and access, the greater the discount they receive. This encourages active usage from a production perspective.

In addition, the launch of UDL is Arweave’s direct solution for content monetization. Even on the blockchain, data portability is a major issue. Various cross-chain bridge accidents are evidence of this. The goal of UDL is to build a unified data protocol. As founder Sam said, “UDL allows users to embed programmable and legally enforceable licenses into any type of data uploaded to Arweave, and generate ongoing revenue from royalties.”

When creating content, UDL can also be used to tag data to support users’ subsequent data management work. UDL not only applies to text and video, but theoretically, UDL can be pre-defined programming for all formats of data on Arweave.

Similar to various licensing systems in the open-source field, UDL delegates permission management to users themselves and tracks and manages them uniformly through code, striking a balance between protecting content copyright and maintaining an open world. Currently, UDL allows for settings such as replication, visibility, and publicity, as well as distribution management and commercial availability.

Conclusion

Starting from the problems existing in the Web3 creator economy, this article focuses on reviewing the development process and current stage of the Web3 creator economy, and explores the reasons for the temporary silence of the creator economy, using games and metaverses as an entry point.

In terms of a long time period, the current problem with Web3 is that various aspects of infrastructure are still insufficient. Although there are practices like Mirror and Lens, there is still a significant gap compared to traditional competitors. In the short term, there is no possibility of direct confrontation. For the industry, it still holds more experimental significance than practical significance.

However, before more infrastructure is built, the most important thing is to have the right direction.

Arweave’s approach is to first build the storage layer, then involve the protocol layer, and gradually move forward with the adoption of Mirror and Lens, hoping to guide the Prometheus fire and illuminate the bright path of the next era.

References:

- The LianGuaission Economy and the Future of Work

- Arweave Ecology Report: Creator Economy

- 2022 Internet Creator Economy White Paper

- Web3.0 Creator Economy Report: Development Status and Imaginative Space of CreatorFi

- The Web3 Renaissance: A Golden Age for Content

Like what you're reading? Subscribe to our top stories.

We will continue to update Gambling Chain; if you have any questions or suggestions, please contact us!