Original Author: Scarlett Wu

In the past two weeks, the roller coaster ride of YGG price has refocused the market’s attention on the game guild track. At the beginning of the rise, I shared a summary of the game guild treasury from the perspective of the treasury on Twitter called “Game Guild Treasury Comparison & Valuation Summary: YGG, MC & GF, whose valuation is more reasonable?” At that time, MC was the most promising, and now its price has risen by 50%. On the other hand, the price of YGG has rapidly declined after reaching its peak, returning to the price before the summary was written. This article is a revision and expansion of that summary, conducting a comprehensive inventory of the game guild track from four perspectives: business capabilities, investment capabilities, risk control capabilities, and valuation.

Many game guilds, Quest platforms, game information aggregation platforms, and NFTfi protocols for pay-after-use are actually subdivisions of the same service. This is because game project parties have only three demands:

- THORChain launches lending protocol Understanding THORChain in 12 pictures

- Introduction to native Account Abstraction in zkSync

- Binance.US will use MoonLianGuaiy as a banking alternative to restore USD business.

1. User acquisition

2. User engagement

3. Promotion of in-game consumption

Web3 players only have two demands:

1. Sense of companionship

Due to the demand for upfront capital investment brought by the ponzi scheme at the beginning of the years 2020-2022 (for example, when Axie prices were thousands of dollars, guilds purchased NFTs to lease to Southeast Asian players and took a cut from their subsequent income), and the wealth effect generated by the booming economic system, people mistakenly believe that the drumbeat of passing the flower will never stop, giving birth to another important function of Web3 game guilds:

2. Capital funding

The premise for generating the need for companionship is that users will spend enough time on the game, a requirement that is not met by any non-ponzi Web3 game at present. However, guilds need to invest in purchasing “shovel” NFTs to lease to users, which requires a Web3 game with a continuously expanding economy. If the capital invested two weeks ago has already started to lose money, any institution that provides capital funding will have to be on edge. However, the fact is that, except for the crypto game ponzi pioneer Axie Infinity, there is still no game in the industry that has sustained user growth for more than half a year. Given that the premise for ponzi profits is user growth, guilds willing to provide capital funding need to spend two months finding a game that “can make stable profits,” two months observing “this game can indeed make stable profits,” and two months implementing the plan to desperately discover that the invested capital cannot be recovered because the “scholars” (the term guilds use to refer to their players) may never be able to recoup their investment even after playing for ten years.

Guilds have obviously realized this problem earlier. Under the driving force of the fact that every Ponzi cannot reproduce the popularity of Axie and that every game’s demand for a sense of companionship is not strong enough to charge through live broadcasts (the traditional source of income for game guilds), guilds have transformed from “serving players” to “serving project parties”: on the one hand, guilds hold a large number of player resources (which is now actually questionable and will be discussed in the following text), on the other hand, guilds have a large amount of funds in their treasuries (although the liquidity is likely to be questionable and will be discussed in the following text), and they can enjoy the growth dividends of the Web3 game track through investments. Of course, there are also cases like Merit Circle, which cooperates with Avalanche’s subchain, using the narrative of a game public chain to enhance valuation imagination.

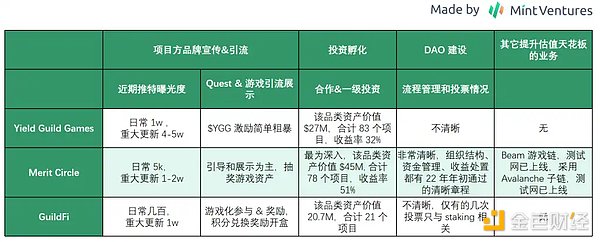

1. Business Data Comparison: YGG and MC are still active, while GF’s volume has fallen behind

Currently, the main traffic sources for the major guilds are:

1. Quest System

2. Twitter

3. Discord

Discord is deceptive, even in YGG’s 70,000-member DC group chat, without hot games/tasks, there are only a few hundred messages in the General Chat every day, half of which are gm and hi, and the other half are team members answering questions with Medium/official website links.

Twitter, on the other hand, can provide insights through page views. Even though YGG has 180,000 Twitter followers, Merit Circle has 100,000, and GuildFi has 120,000, the page views of YGG’s Twitter content remain stable at several thousand to tens of thousands, with only major updates reaching 40,000-50,000 views. Merit Circle falls slightly behind with daily content views around 5,000 and major updates reaching tens of thousands. GuildFi’s situation is even worse, with less than 1,000 views for regular update releases and only 10,000 views for semi-annual reports. In comparison, a tweet casually posted by the author’s 2,000+ followers on Twitter receives at least several hundred views, and a slightly more in-depth summary can garner tens of thousands of views. With the transparent data display on Twitter, the inflated data of game guilds is nowhere to hide.

As for the Quest System, it can be explored from two aspects: project status and incentive situation:

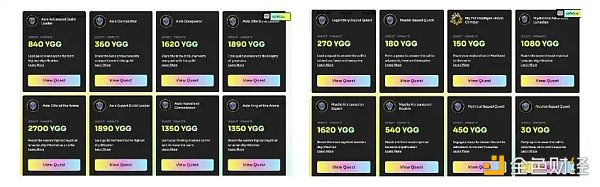

YGG Guild Advancement Program

Recently, YGG launched Guild Advancement Program Season 4, where players can complete tasks and upload evidence to share the corresponding task rewards pool. Among them, Axie’s rewards still have the advantage, with the highest individual reward reaching 2,700 YGG tokens (equivalent to approximately $900 based on the current YGG price), while rewards for other games range from 30 YGG tokens (i.e., $10) to over a thousand YGG tokens. For players who still have the ability to compete for the Axie Infinity rewards pool, the rewards offered by Axie are undoubtedly more appealing (with a maximum value of tens of thousands of dollars), while for players of other crypto games, the rewards pool to be shared with competitors, totaling tens to hundreds of dollars, is not very attractive. From a user’s perspective, YGG’s Quest System is difficult to attract a lot of attention.

From the project’s perspective, YGG’s cooperation with games will likely receive cash or other game assets, while what is given to players is rewards valued in YGG tokens, which is essentially YGG exchanging its own tokens for other cash/game assets.

https://www.yieldguild.io/gap/season-4

Merit Circle Gaming

Compared to the straightforward tasks in YGG’s Quest System, Merit Circle Gaming’s interface is more game-friendly. The official website of this incentive system is divided into four sections: Home (focused on game introductions and activity timelines), Games (focused on game showcases and related information summaries), Academy (game tutorials and Web3 operation basic tutorials), and Quest System (complete tasks, receive experience rewards, and participate in game NFT lotteries).

In the Quest system of YGG, players can have a more direct ROI calculation (although the ROI is not high, it is still attractive to the Southeast Asian population), while the Quest system of Merit Circle is more inclined towards information aggregation and game display, with most task rewards being distributed through lottery.

Merit Circle – Homepage

Merit Circle – Featured Game Display

Merit Circle – Academy

Merit Circle – Task Reward System

GuildFi Quest & Achievements

GuildFi has created a task & achievement system using in-game points, and players can earn corresponding point rewards by completing corresponding tasks and achievements.

GuildFi Quest & Achievements

Points can be used to exchange for gift cards, game tickets, whitelist access, treasure chests, NFTs, etc. However, currently, the products that can be exchanged with GuildFi points are quite limited, mainly Steam gift cards (with a probability of getting gift cards worth $0.5 – $30, and a possibility of 15% cost refund), Genopet and Axie game tickets, Axie NFTs, and CyBall NFTs (distributed in the form of limited-time lottery). This lottery blind box exchange model for Steam gift cards/game items has already been widely used in traditional game information aggregation and casual game platforms. On one hand, it cooperates with game project parties to distribute game assets (although it can be seen that GuildFi’s BD capability is quite limited, and the cooperation is mainly with old projects), and on the other hand, it directly converts a small portion of the income into assets with existing value concepts for players, and introduces blind box mode to gamify the elimination of inflation.

GuildFi Marketplace

In GuildFi’s semi-annual summary, they stated that “in the past year (2H22 – 1H23), there have been over 200,000 purchases on the platform, a 42% increase compared to the previous year. It is evident that our community’s enthusiasm for the game products on our platform is rising. It is worth noting that the Lootbox event of Diablo IV won the championship with over 65,000 purchases, while the KOF Lootbox had over 30,000 purchases.” With such collaborations, GuildFi has brought a total of 92,000 pre-registered users to 21 partner companies in one year, averaging less than 5,000 registrations per game. Considering that pre-registration usually does not require wallet interaction and it is easy for users to create multiple accounts for profitable projects, the actual number of effective users brought in is even more worrying.

Source: GF Semi-Annual Summary

Combining the previous content, it is not difficult to see that the power of the game guild in the market has been greatly reduced. YGG and Merit Circle are still relatively active in the market, while GuildFi has fallen behind in terms of business resources and content production.

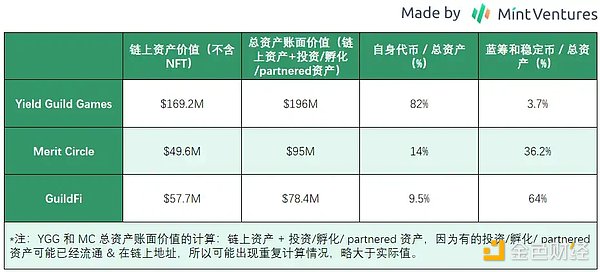

2. Financial Situation Comparison: MC’s financial and business levels are balanced, YGG has strong business capabilities but lacks financial level, GF’s market value is less than the value of blue-chip + stablecoin assets held

YGG: Game dissemination platform + game investment fund, the treasury is almost all YGG, less than 4.4% of high liquidity assets on-chain

Due to the significant depreciation and illiquidity of game NFTs on the market, we can roughly estimate the situation of the project’s treasury directly from FT. According to the official address disclosed by YGG, 95% of the on-chain treasury of YGG is its own token YGG, and less than 4.4% is high liquidity stablecoins and blue-chip assets (USDC/USDT/ETH, etc.), indicating a significant imbalance in asset allocation.

YGG treasury address asset situation Arkham, Mint Ventures chart *Excludes assets off EVM chains, the amount of these assets is approximately $220,000, which can be ignored when calculating

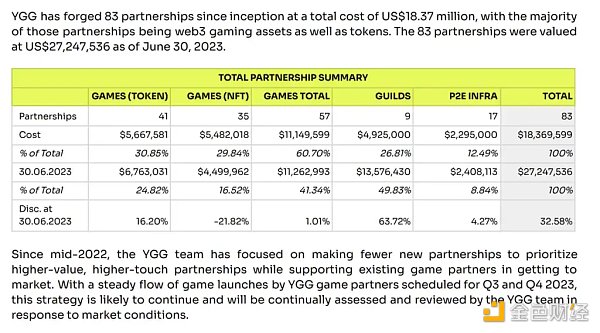

In addition, YGG’s 2023 Q2 Community Update released in early August gave a value calculation of investment/cooperation project assets: YGG holds a total of $27.2 million worth of game assets (NFTs, tokens, equities, etc.), with a corresponding cost of $18.3 million and a book profit of 32%.

Source: YGG Medium

Although YGG honestly disclosed the market price decline of Gaming NFTs, there may be certain calculation errors in the valuation of tokens/NFTs in the Games section: even if YGG obtained a good price when investing, the book value of primary investment game tokens is likely to shrink significantly after listing. In the current situation of poor NFT liquidity, selling NFTs for liquidity requires a substantial discount. The same situation applies to Merit Circle and GuildFi.

YGG LianGuairtnered Games (held assets, including primary investments and secondary market purchases, incomplete statistics from chainplay.gg)

Merit Circle: Stable business development, optimal treasury fund balance, equal distribution of stable income and high-risk assets

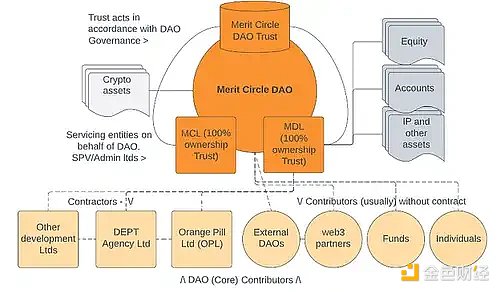

On Merit Circle’s official website, they define themselves as a Gaming DAO with four functions: investment, game studios, reward system, and infrastructure (building the game chain Beam through the Avalanche subchain). In terms of communication transparency, MC is superior to the other two guilds: the dashboard of the treasury funds is updated in a timely manner, which not only includes on-chain FT/NFT data that can be checked, but also discloses non-liquid assets such as primary investments. Here, we mainly analyze two parts: the situation of investments and incubation, and the allocation of treasury funds.

Merit Circle Official Website

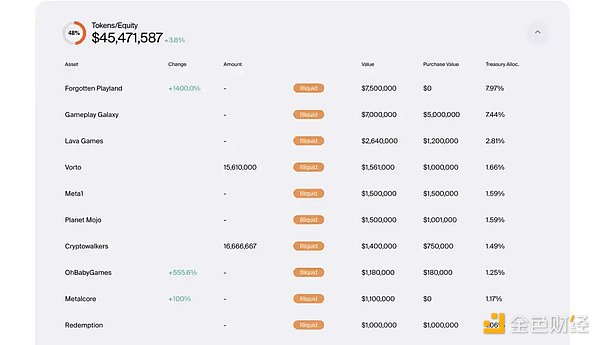

First, let’s look at investment and incubation. According to the data publicly available from the MC Treasury until June 23rd, MC holds equity/tokens in a total of 79 gaming projects. Among them are major projects with good team backgrounds and financing backgrounds, such as OhBabyGames and Xterio. The value of these assets is $45.4 million, of which $1.6 million is available for public trading, $43.8 million is illiquid assets, and $300,000 is MC. In addition, based on the disclosed purchase prices, the total cost of these assets is $29.9 million, with a book profit of 51.8%.

https://treasury.meritcircle.io/treasury Incomplete screenshot of MC investment projects

The quality of the on-chain treasury funds is also significantly stronger than YGG. Only 27.4% of the funds in the wallet are MC tokens, while 69.5% are highly liquid stablecoins and mainstream assets.

Merit Circle treasury address asset situation, Arkham, Mint Ventures

In addition, the launch of the Avalanche sub-chain Beam on the testnet by MC is also an important event for future trends. Beam will adopt a Proof of Stake model, using MC as the gas token, and will use LayerZero as the cross-chain infrastructure. Currently, three games are being developed based on Beam. On August 14th, the team proposed a draft and opened it for discussion in the community governance section:

https://gov.meritcircle.io/t/beam-development-and-ecosystem-funding/822

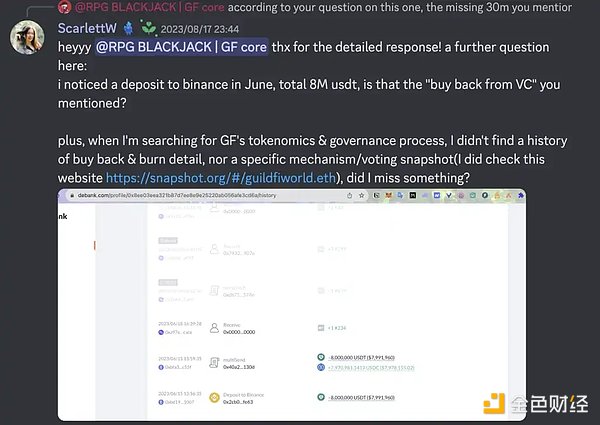

GuildFi: Weak business capabilities, good balance of on-chain treasury funds, 13% GF, 46% stablecoins, 41% stETH seeking stable returns

Since GF’s assets include many LPs on Uniswap, it is difficult to directly display them through Arkham. The following figure shows the on-chain asset statistics of the publicly disclosed wallet: It can be seen that GF’s on-chain treasury consists of 46% stablecoins, 41% ETH/stETH, 13% GF, and some small game-related token investments, totaling $57.7 million.

Compared to the data in GF’s semi-annual financial summary, the official on-chain assets have decreased by 19% from the $71 million reported in the summary, mainly due to token price declines and the transfer of 8 million USDT to Binance. The official team stated that the assets held in cex are mainly used for daily operations and buybacks from investors.

Source: Debank

Source: GuildFi

However, when further asked about the “existence of a public buyback mechanism and buyback history records,” besides a two-day “please be patient” response, no reasonable answer was given.

Discord Q&A Records

In the semi-annual summary, in addition to the $71 million assets in Reserve (currently totaling $57.7 million on-chain), there are also $15.9 million worth of primary market investments and other game tokens, as well as $4.8 million worth of NFTs.

GF Cooperative Games

3. DAO Construction and Governance Capability Comparison: Merit Circle is far stronger than its competitors

Although both YGG and GuildFi stated in the whitepaper released in 2021 that the ultimate goal of this gaming guild is to become a Gaming DAO, in reality, it is Merit Circle that has actually achieved this goal.

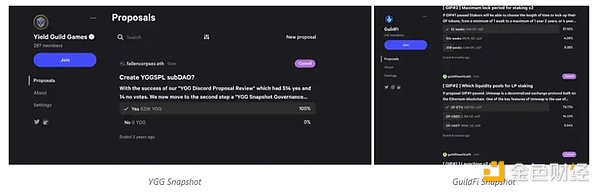

When we open YGG and GuildFi’s Snapshots, we can only see a few ancient voting records:

YGG: A proposal for SubDAO two years ago.

GuildFi: Three proposals and details about the Staking System launched eight months ago.

On the other hand, Merit Circle shows users how a Gaming DAO / Investment DAO with a complete operation process and risk control awareness should operate: In the past two years, Merit Circle’s Snapshot has a total of 26 proposal votes, including DAO governance, investment risk management (exit and investment authorization mechanisms), game development, etc. Some important proposals include:

2022.01 MIP-7, determining revenue distribution and token burning. 20% of the revenue is saved in the treasury in the form of USDC, 5% of the revenue is saved in the treasury in the form of ETH/WBTC, 60% of the revenue is used for low-price repurchases at appropriate times to maintain price stability of the tokens (repurchases are conducted when the price is 10-35% below the 7-day average price, and this part of MC mainly goes into staking rewards and can also be sold to long-term lock-up strategic investors), 15% of the revenue is used for direct repurchase and burning of MC tokens. In addition, since most of the unlocked tokens are released to “community incentives,” it is decided to burn 75% of the unlocked “community incentive” tokens each month (the proportion can be modified by community voting). Provide enough tokens for the DAO’s treasury to cover any major community proposals and transform mCap into a more realistic FDV. It is difficult not to be surprised by MC’s foresight and the calmness in the face of great temptations – actively burning 75% of the tokens released to the community is not an easy decision, and the completeness of the mechanism is the foundation for the balance of MC’s treasury.

MC repurchase and burning announcement: https://treasury.meritcircle.io/

https://gov.meritcircle.io/t/mip-7-sustainable-future-vision/192

Return of investment to YGG in May-June 2022. Dissolving relationships with investors who have provided no substantial help.

https://snapshot.org/#/meritcircle.eth/proposal/QmT71tWtTwk6q5Cd2kvhoLzxm76SpNaQGBR9RE7pCxBM58

https://snapshot.org/#/meritcircle.eth/proposal/QmanW7dTyF2LvvU9iAGwj3i9D4F3TS7ZbxR33jVCmKMrgR

2022.07 DAO restructuring.

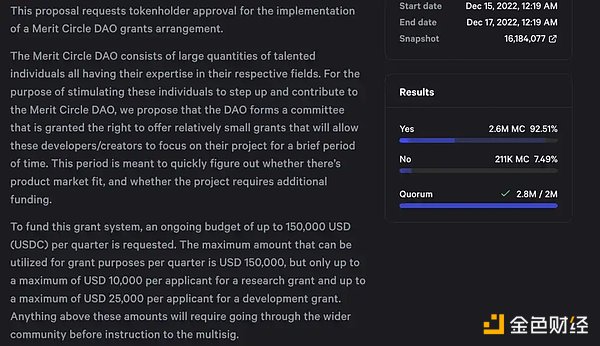

2022.12 Proposal for Merit Circle Grants. Set aside 150k USDC per quarter for small incentives for research and game development. Research Grants should not exceed 10k per project, and Development Grants should not exceed 25k per project.

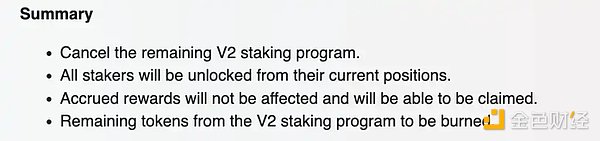

2023.07 Cancel future Staking rewards for Uni V2 and burn the remaining rewards. This decision is mainly based on the fact that the existing Staking model does not bring much benefit to Merit Circle, but staking on Beam (the game chain MC plans to build, proof-of-stake) has clear use cases. Therefore, the rewards for staking will be focused on Beam in the future.

https://gov.meritcircle.io/t/mip-26-cancel-all-future-v2-v3-staking-rewards-and-unlock-all-v2-stakers-proposal/803

From the analysis of several proposals, although the proposers are mainly the team and the number of voters is not large (around 5 million MC), the Merit Circle team has a clear strategic vision and is willing to sacrifice short-term interests to safeguard the long-term interests of the community. The governance is relatively transparent.

4. Summary and Comparison: Business Capability, Investment Capability, Risk Control Capability, and Market Value Comparison

4.1 Business Capability: MC has a more diverse business, YGG has a broader user base, GF lags behind

In addition, from an organizational structure perspective, YGG’s model is a product of the Axie era – YGG extends sub DAOs in different regions to facilitate regional members’ reach and management, but lacks an up-to-date risk control system. On the other hand, Merit Circle is more like a game factory, with investments (and a complete risk control system), incubation, promotion, and infrastructure, all done well. GuildFi’s investment capabilities and market activity are inferior to the first two.

4.2 External Cooperation and Investment Capability: MC is in the lead, followed by YGG in terms of scale and profitability, GF has the smallest scale, and the profitability is unknown

4.3 Risk Control Capability: MC is in the lead, followed by GF, YGG performs poorly

The evaluation criteria for this part are twofold:

· Whether the team’s transactions, management, and control of assets are transparent and in line with pre-established mechanisms, in this aspect MC>>GF/YGG

· The extent to which the asset token affects the total asset price. If the ratio of “self-token/total assets” is too high, it indicates poor risk control. Position management GF>MC>YGG.

Overall, MC is in the lead, followed by GF, while YGG performs poorly.

4.4 Valuation Comparison: MC has reached a high level, YGG is experiencing a normal decline, and GF’s weak business results in a market cap < the total value of the treasury stablecoin and blue chips

Due to the nature of the guild’s business, the treasury assets of the project can partially reflect the business situation. As mentioned earlier, the guild’s current core functions are:

1. Serving game projects based on the players at hand

2. Investment and incubation

These functions correspond to part of the project’s assets entering external cooperation and investment book value (NFT, FT, equity), and part of them may have been converted into stablecoins and blue chips left in the treasury. Therefore, the comparison of treasury assets can partially reflect the valuation of the guild’s projects.

Before the YGG rally, YGG’s daily trading volume was only a few million dollars, and liquidity was quite limited. With YGG accounting for 82% of the YGG in the treasury, it means that once sold, it will only cause devastating impact on the price. Therefore, here we will compare “mCap/book value of total assets” and “mCap/total market value of assets excluding self-tokens” for objectivity. Taking all factors into consideration, the value support is GF>MC>=YGG (Please note that both “book value of total assets” and “total market value of assets excluding self-tokens” include “stablecoins + blue chips” and “FT/NFT brought in by investment/external cooperation”. The valuation of the latter is not fair market value but comes from financing valuation, which poses a significant risk of asset impairment in the future if the token is listed or the project does not develop smoothly. In addition, for “FT/NFT brought in by investment/external cooperation”, besides Merit Circle disclosing the cost and book value of all projects, the other two have not provided specific algorithms, so there may be statistical calibration issues.)

Since most of MC’s unlocks have already been completed, but YGG and GF still have a large number of tokens unlocked, from the perspective of FDV/mCap, the potential downside risks are YGG>GF>MC.

Except for MC, which has a clear token repurchase mechanism, the other projects do not have a token repurchase mechanism. GF has a Staking mechanism with fixed reward release, while YGG doesn’t even have staking. Combined with GuildFi’s weak position in the business, even if GF’s market cap is lower than the total market value of its on-chain stablecoins and blue chips, it is difficult to conclude that it is “undervalued”.

Looking forward to the future, Upside observes that MC will have a game chain narrative and the value capture of staking on the POS chain will naturally follow. YGG, on the other hand, will establish a new Quest System on top of the Base. GF, for now, does not have any breakthroughs in terms of business narrative.

Like what you're reading? Subscribe to our top stories.

We will continue to update Gambling Chain; if you have any questions or suggestions, please contact us!