Original author: TokenBrice Translation: LlamaC

New stablecoins continue to emerge, so there is a need to constantly track relevant innovations. AMO? PSM? DSR? pegKeeper? This article explores the different mechanisms used by various stablecoin projects and evaluates their interrelationships.

New types of stablecoins are constantly emerging, and this trend will not stop in the future as the number of stablecoin models on chains, layers, and operations increases. In DeFi, gaining insights into the stablecoin field is becoming an important skill.

Although centralized stablecoin models are easier to evaluate, decentralized stablecoins utilize various complex mechanisms, making it difficult to compare data between them. However, dozens of new decentralized stablecoins appear every year, and I don’t think this trend will stop soon.

- Philippines SEC collaborates with US SEC to combat cryptocurrency fraud

- NFT Blind Box Mechanism Seeking Certainty in Uncertainty

- Standard Chartered’s subsidiary, Zodia Custody, will provide returns for institutional clients’ holdings of cryptocurrencies.

Therefore, this article aims to provide an overview map to help you gain insights into the field of decentralized stablecoin design. Before delving into the innovations of decentralized stablecoins, let’s take a minute to understand the background: why are we so concerned about (decentralized) stablecoins?

Scale

Simply put, stablecoins are the most market-fit area in the cryptocurrency market, far exceeding other tracks. DeFi is cool, right? We also like to talk about stablecoins. But in terms of scale, the value locked in stablecoins is about three times that of DeFi protocols.

Currently, the total TVL value of DeFi is about $38 billion, while the circulating stablecoins amount to $124 billion, dominated and served by centralized stablecoins: USDT accounts for 66% of the total, and USDC accounts for 20%.

Now, let’s start exploring! When considering various designs for providing decentralized stablecoins, I will use examples from existing projects to illustrate the mechanisms discussed: you can think of this article as a combination of a recipe and a raider map on the theme of decentralized stablecoins.

◎ Overview of the decentralized stablecoin landscape

How to build decentralized stablecoins

Regardless of how diverse the designs are, they all rely on two basic core requirements:

1. Price stability | Find an effective way to stabilize the price without compromising too much decentralization.

2. Stablecoin liquidity | Actively manage the liquidity of stablecoins to maximize their effectiveness and sustainability.

Although both core requirements serve the same purpose: ensuring that stablecoins can be traded at par value under any circumstances, they operate within different time frames. The establishment of stability mechanisms is to make stablecoins tend to be anchored in the medium/long term. Liquidity strategies aim to ensure that even with a large amount of stablecoins, they can be traded as close to par value as possible.

These are the two prerequisites for stablecoins to gain market attention, and defects in these two dimensions can jeopardize the entire design framework. Therefore, let’s take a look at the currently running price stability mechanisms in the market and their existing impacts.

Stability Mechanism

When faced with a significant exchange demand, decentralized stablecoins can detach from their pegs—meaning they deviate from the peg, usually starting from $1, whether it is upwards or downwards. Although similar, these two detachments stem from completely different design challenges. Let’s start with the most common case, which is the detachment when the value of a stablecoin pegged to the US dollar is below $1.

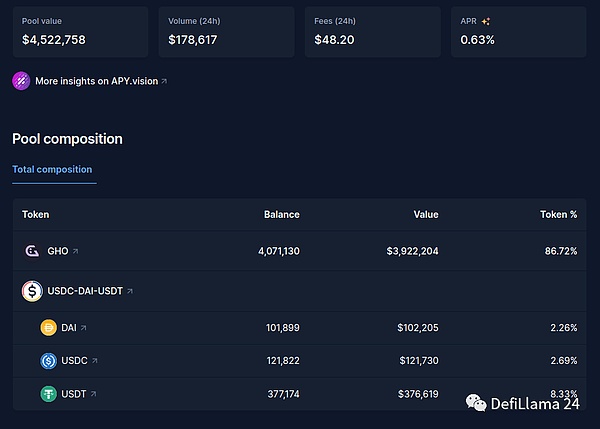

GHO—Insufficient Peg

This usually happens when stablecoins are mainly used for leverage and lack important direct use cases. The current major example is Aave’s GHO, which trades at around $0.97. GHO is one of the cheapest borrowing stablecoins (with a maximum 1.5% management fee), creating a significant initial demand for it. However, apart from providing liquidity, GHO has not many direct use cases. Therefore, many borrowers will exchange their GHO for other currencies, such as DAI, to earn a 5% yield from DSR.

In addition, AaveDAO has been slow in supporting GHO. Despite the fact that GHO stablecoin has been launched since mid-July, there are still not many incentives to increase the liquidity of GHO, and the allocation is improper as most of it is concentrated in stablecoin exchange pools, while GHO is overweight due to its price. As 80% of these pools are dominated by GHO, the liquidity they provide is insufficient given the current price.

◎ One of the major GHO pools on Balancer

Currently, the only pressure for GHO to re-peg comes from existing borrowers, who can consider repaying their debts with a discount of about 3% if they can borrow and exchange GHO at around $1.

GHO will need to provide attractive profit options directly to get closer to the peg again, such as providing liquidity incentives. Nevertheless, a pledging module based on GHO and with profit-sharing functionality can still do a good job in completing this task. Overall, we need more GHO trading pairs: mechanisms that lead to the minting and long-term holding of GHO. Currently, governance seems to be pushing for more support for GHO liquidity incentives and potential GHO PSM (Peg Stability Module): we will discuss this design in more detail when discussing Maker/DAI.

Since its launch a few weeks ago, GHO currently faces major challenges due to its young nature, combined with insufficient preparation on the DAO side. The DAO is improving and proposing multiple suggestions to address this issue.

LUSD — Over-Collateralization

Liquity maintains its price stability by utilizing a unique mechanism called redemption. In Liquity, users deposit ETH as collateral to borrow and mint stablecoins (LUSD). The key innovation lies in the redemption mechanism, which allows users to redeem LUSD for the underlying collateral (ETH) at a fixed ratio even if the ETH market price significantly drops.

This mechanism incentivizes users to redeem LUSD when the ETH price is low, stabilizing the price of LUSD, reducing its circulating supply, and supporting its peg to the US dollar. It provides LUSD holders with instant and immutable access to LUSD collateral without the need for decentralized exchanges to provide liquidity.

Redemption provides an additional layer of guarantee for LUSD holders but adds complexity for borrowers, forcing them to monitor and adjust their loan-to-value (LTV) based on other protocol users and market conditions.

Collateral redemption offers the most direct way to obtain stablecoin support. Centralized stablecoins like USDC or USDT achieve dollar pegging through similar but permissioned mechanisms.

Although the situation has improved recently, LUSD has mostly been in a premium state during its existence. In fact, several factors have contributed to increased liquidity and pegging pressure: the success of Chicken Bonds, the aggressive liquidity strategies of new types of DEXs like Maverick, or LUSD accumulation by DAOs and treasuries.

The reasons for the premium still need to be accurately identified. One possible main factor is that LUSD serves a niche market of maximizing elasticity in stablecoins, where demand (people wanting to hold LUSD) often exceeds supply (ETH holders borrowing LUSD and selling it). Liquity’s blog extensively discusses this topic from last year.

While under-collateralization is usually more concerning, over-collateralization can also have other consequences as it makes it harder to predict users’ effective borrowing costs.

The over-anchoring of LUSD is mainly driven by psychological mechanisms: during market panic movements, we observe the worst cases of its persistent over-anchoring, especially when a significant centralized stablecoin is perceived to be at risk.

In fact, due to its elasticity, LUSD is seen as a safe haven stablecoin. This is a remarkable achievement, but it comes at a cost: when other stablecoins face problems, such as USDC detaching by 10% after the Silicon Valley Bank run, people flock to LUSD. The trading volume of LUSD on that day is incredible, with bids breaking through $1.03, $1.04, and $1.05 amid market panic. In the midst of panic, some users are willing to pay a high price for safe passage.

DAI and PSM: Solving the Over-Collateralization Issue at a Price

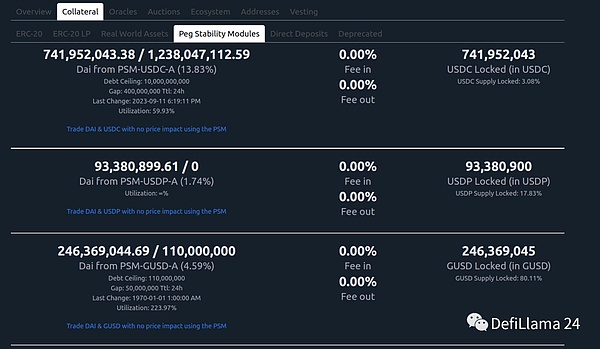

In the early days, before the Multiple Collateral Dai (MCD) upgrade, DAI faced a similar challenge as LUSD: it tended to be over-pegged. Through the upgrade, Maker introduced the Peg Stability Module (PSM) to manage the price stability of its stablecoin DAI. The PSM acts as a buffer between the market and the DAI ecosystem. It allows users to exchange stable assets such as USDC for DAI at a fixed exchange rate.

By adjusting the exchange rate based on market dynamics, MakerDAO can influence the supply of DAI on the market and make its price closer to the peg with the US dollar. It helps MakerDAO address the over-pegging issue observed before the introduction of the PSM. However, it comes at a cost: the accumulation of USDC and other centralized stablecoins as collateral for DAI.

Accumulated $~1B of centralized stablecoins as collateral for DAI through the PSM

FRAX’s AMO: Scaling Liquidity and Risk to Infinity

FRAX is a decentralized stablecoin that maintains its peg through algorithmic market operations. FRAX adopts an adaptive mechanism to adjust its collateral ratio according to market conditions. When the price of FRAX is higher than its pegged price, the system mints new FRAX and buys back collateral to increase stability.

Conversely, when the price of FRAX falls below the pegged exchange rate, it lowers the collateral ratio to incentivize users to mint FRAX, which helps restore the pegged rate. The AMO introduces additional risks, primarily depending on the usage of uncollateralized minting assets: the greater the risk, the greater the threat.

This design’s main risk becomes apparent when one of the services utilized (usually a money market or DEX) encounters an issue. Suppose the AMO mints 10 million FRAX and deposits them into a money market for users to borrow. Now, one of the collateral assets in the money market encounters a problem and gets depleted: the circulating supply of FRAX has increased by 10 million tokens, while the collateral is reduced to 0.

Addressing this issue requires very active management of the AMO – managed by humans through multi-signature, which is not ideal from a security standpoint since the AMO can mint FRAX arbitrarily without backing.

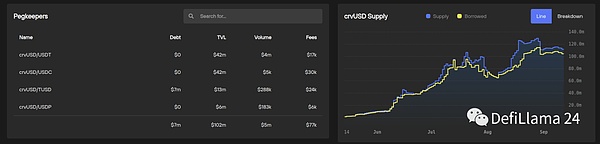

crvUSD pegKeeper: A Better PSM?

To ensure the peg stability of crvUSD, Curve explores a path similar to the PSM but with slight improvements. In fact, it no longer relies on user external participation:

For the Maker PSM, it is still user-driven: when over-pegged, users provide USDC as collateral for the Maker PSM and mint DAI, thus helping push down its price. If DAI falls below the pegged rate, users can also buy DAI (below $1) to exchange for 1 USDC, helping its price recover the pegged rate.

The operation of crvUSD at a high level is similar to (if crvUSD>$1 => minting, if crvusd<$1 => burning), but it does not require any external input: the system can stabilize itself due to its pegKeepers contract. These special contracts can mint uncollateralized crvUSD under certain conditions and only for specific use cases.

There are 4 pegKeepers, each inserted into a different crvUSD pool, paired with redeemable centralized stablecoins USDC, USDT, USDP, and TUSD. When crvUSD is overpegged, they can mint crvUSD to trade into the relevant pool, helping to push the price of crvUSD back to $1. When crvUSD is below the peg level, pegKeepers can buy back crvUSD on their associated pools (using centralized stable balances accumulated over the peg duration) and burn it to push the price of crvUSD back to the peg level.

Therefore, when stablecoins are overpegged, pegKeepers accumulate crvUSD debt to the protocol and ideally reabsorb it once crvUSD is underpegged. The key here is balance, ensuring that the price difference between the supply of crvUSD (including Pegkeeper debt) and the borrowed supply does not grow too large.

◎ Curve Monitoring Data

Although pegKeepers still pose a significant threat to the protocol, like FRAX’s AMO or Maker’s PSM, the risk seems to be lower. However, crvUSD is still a relatively young stablecoin, and only time will tell.

Liquidity Management

Liquidity management, even for stablecoins, can be a great topic for research. It is one of the most misunderstood topics in the field. Dear readers, I hope you realize its importance.

Liquidity Management as a Non-Topic

If you are reading this blog, you may already be aware that liquidity strategy is at the heart of the stablecoin war storm. However, many teams have not yet achieved this goal. They consider it a less important matter that DAO can handle later, which is a dangerous mindset.

In fact, DAO is not the optimal structure for managing liquidity; they often leverage suboptimal solutions, pay excessive fees, and simply need higher speed to match the fast-paced liquidity game. This is not surprising; we have long established that DAO/governance is well-suited for strategic (long-term) direction but not for medium/short-term (tactical) management, thanks to the example of MakerDAO (although it is absurd that MKR holders still vote on the interest rate of the treasury as a purely operational parameter).

The obvious solution is for DAO to appoint a liquidity committee – a small team composed of liquidity experts and provide them with a budget they can autonomously mobilize. The committee can be hired on a fixed-term basis, while DAO retains the right not to renew or even revoke the committee, similar to other service providers.

I invite you to check out the main stablecoin projects running on DAO and see which ones still have committees. As far as I know, only Aave is considering establishing a GHO liquidity committee. In addition to providing flexibility and improving operational capabilities, it allows the liquidity methods of DAO to be more structured and forward-looking, enabling exploration of relationships and collaborations with more relevant participants. For example, supporting innovative DEX from the same day without spending months explaining the relevance of innovation to stakeholders of DAO and voting and executing budgets.

Scarce Abilities

The harsh reality about liquidity management is that abilities are extremely scarce. This can explain why it is necessary to better understand this topic and rarely prioritize it in project design or later governance discussions. Suitable liquidity managers must accurately understand the following:

• Basic liquidity structure model, x*y=k

• Customized liquidity structures, such as stableswap

• Basic concentrated liquidity, UNiv3 style

• Uniswap liquidity management layer (Bunni, Merkl, etc.)

• CL liquidity manager models (Gamma, Arrakis, etc.)

• veCRV token economy and ecosystem // veBAL

• Voting markets and bribery culture

• Advanced concentrated liquidity, unconventional style

• Maverick incentive model (Boosted Pool)

• Maverick token economics (veMAV)

• DEX aggregator patterns and path logic

The range of tools, services, and protocols for liquidity management is growing exponentially, but few participants pay close attention. There is often an absurd gap between the liquidity expenditures of two similar projects, sometimes reaching several orders of magnitude between investment and results.

How to attract a large amount of ETH&LSD on-chain?

So far, we have focused on stablecoins that use the CDP (Collateral Debt Position) model, such as Maker, Liquity, or Reflexer, where users must deposit collateral to directly sign debt contracts based on the protocol (each borrower on the CDP protocol will mint their “own” debt). This is an elegant design that allows the protocol to implement various mechanisms to absorb the volatility of collateral and maximize the price inertia of stablecoins.

Limitations of CDP-based stablecoins

However, CDP-based stablecoins have one major drawback: overcollateralization requirements. In fact, it is difficult, if not impossible, to suppress the volatility of collateral such as ETH without any margin of error. For example, on Liquity, the acceptable minimum collateralization ratio is 110%, but the average collateralization ratio observed on the protocol is 226.3%.

Overcollateralization is a core limitation of the CDP model and is difficult to overcome. In fact, reducing collateral requirements may attract more borrowers and increase the risk range of stablecoin production. Therefore, expanding CDP-based stablecoins is a daunting task. There are other related ideas to attract more borrowers, such as diversifying collateral issuance, as shown below. However, the risk of stablecoins also increases, as seen with DAI, where the decentralized nature of collateral has significantly degraded over the past few years.

However, many projects are exploring methods that may result in fewer compromises than DAI for stablecoins, while achieving similar scale. Let’s consider some further directions currently being explored for decentralized stablecoins.

Expanding Collateral and Network: Liquity Forks

2023 is the year of Liquity forks: many protocols have been launched this year that utilize models similar to Liquity to varying degrees, with some changes. These include Gravita, Prisma, Lybra, and more.

Gravita

Let’s start with Gravita, which is perhaps the closest to the basic Liquity model. The focus here is to make the protocol more attractive to borrowers and introduce some popular features, such as the possibility of borrowing using stETH or rETH as collateral, or protocols provided on L2 (such as Arbitrum). Of course, this is a balancing act, as the rules specified above still apply.

Prisma Finance

Prisma Finance is also exploring similar methods. It is another Liquity fork that can use ETH-LSD as collateral, built by a team close to the Curve/Llama ecosystem. Components of veTokenomics are also envisioned on the fee-sharing/governance token PRISMA, but they still need to go live.

Lybra Finance

Another team, Lybra, has experimented with a lockup/custody model on its governance token LBR. While it initially seemed to effectively attract a large amount of funds, the challenge with this strategy is to sustain them over time…

DYAD

Lastly, let’s talk about DYAD. Technically, it is not a Liquity fork itself, but more like a protocol inspired by Liquity, particularly in its stablecoin’s price stabilization mechanism.

The main challenge they are trying to address is adding new collateral to a real-time CDP protocol without excessively expanding the risk scope of the underlying protocol. To do this, DYAD introduces a “social permission layer,” essentially a governance layer.

However, it doesn’t look like the governance we’re accustomed to: there are no governance tokens here, so it won’t be the plutocracy you typically encounter. Instead, governance rights are directly within the dNFTs required to use the protocol: each dNFT can control a single “switch” for the collateral type of each proposal.

They can change the position of this switch from closed to open or from open to closed anytime they want, and then change it back again. If a given collateral maintains a 2/3 absolute majority of the “open” switch, it can constitute part of DYAD’s collateral basket. The only way to increase governance power is to control more dNFTs.

DYAD also earns reward points for maintaining immutability as much as possible. Although the protocol can be changed as new collateral can be added, the entire governance layer is immutable. DYAD has not fully launched yet, only dNFT has been launched, but I’m excited to see how it progresses!

I agree with the professionals here: LSDfi was popular a few months ago, and we saw many protocols offering options to leverage the recently launched ETH-LSD. Although this submarket may already be crowded, there is still room for the CDP-based model, which offers stable coins with slightly lower elasticity than LUSD but with additional features. The question is which one?

Treat your borrowers well: LLAMA/crvUSD

Another way to create a trading pair for ETH/ETH-LSD is to make the conditions more attractive for borrowers/reduce liquidation penalties. In fact, one of the main innovations behind crvUSD is the liquidation model, which is very different from other leveraged services.

LLAMA (Loan Liquidation AMM Algorithm) replaces the usual liquidation with “soft liquidation,” where underwater borrowers rebalance between “intervals,” each representing a different price range.

It provides considerable protection against liquidation caused by harsh but unsustainable market fluctuations. Unlike the direct liquidation we are used to, LLAMA’s soft liquidation is more gradual as collateral is gradually adjusted based on its market price ratio.

Make it rain: Dai savings rate and variations

When there is a more direct path forward, why bother improving your design? MakerDAO pioneered the idea of providing “risk-free” returns to stablecoin holders to drive demand: the DAI savings rate, currently at 5%.

It turns out that maintaining a DAO is very expensive, and it is increasingly pushed towards riskier but more profitable collateral to sustain its existence. Now, a significant portion of the collateral consists of real-world assets (RWA) managed by custodians, some of which operate slowly, or cannot fulfill their yield or reporting obligations, or are simply suboptimal (MakerDAO currently earns 3% on its USDC, while retail can get 5% through Circle).

Nevertheless, surprisingly, the incentives are working, at least initially. Therefore, in the long run, this harsh, low-effort, inefficient design is spreading:

• Raft launched a similar concept with a 6% rate.

• Frax is also committed to a 5% sFRAX/Frax savings rate target.

Now, time will tell the long-term impact of this design. In my opinion, these protocols are consuming most of their income to pay for ongoing acquisition costs – once they stop, they will lose most of the users gained through DSR. For example, they will burn a significant amount of funds to maintain this deception, funds that could have been spent on strategic assets to provide lifelong incentives to stablecoin liquidity providers. This design is a great strategy but one of the most short-sighted strategies I have seen.

Turning towards reserve-backed stablecoins?

A transformation is brewing! While models based on CDPs (such as Maker, Liquity, or Reflexer) are flourishing, reserve-backed stablecoins are also increasingly being considered.

In fact, as we emphasized above, purely loan-based/CDP stablecoins have inherent tension. In short:

• Expanding loan-based decentralized stablecoins requires attracting a large amount of ETH/ETH-LSD.

• But the more lenient the protocol is towards borrowers, the less desirable its stablecoin output becomes.

The status of CDP-based stablecoins is entirely dependent on the behavior of their users. In reserve models, the protocol directly manages the reserves and minting of stablecoins, rather than managing positions separately. Therefore, the reserve-based model seems to provide a reliable answer to the drawbacks of CDP-based stablecoins, as the native protocol reserves provide greater price inertia, and the supply of stablecoins may expand.

Let us summarize this article by examining two main examples of implementing reserve-backed stablecoin models. I will make it concise and understandable, and add further in-depth resources.

f(x): Zero-cost and 90% volatility suppression ETH leverage

F(x) is a newly released fascinating protocol! It is a dual product that allows stETH holders to access two types of assets in the proportion they desire:

• xETH: “High-volatility leveraged ETH”

• fETH: “Low-volatility floating stablecoin”

Similar to the CDP protocol, users deposit ETH (or stETH) to mint fETH or xETH. However, unlike Liquity/Maker/other CDPs, users do not manage their positions (Trove). Instead, the protocol directly manages the stETH reserves. The redemption function allows holders of fETH or xETH to withdraw the underlying stETH. However, the amount they redeem depends on the state of the system, most notably its asset net worth: the overall value of stETH in reserves.

The protocol was launched just a few weeks ago and is still in its early stages, with a TVL of approximately 1300 ETH, and liquidity for fETH is still being developed. The third token, FXN, the governance token of the protocol, is also in the works.

The value propositions of xETH and fETH resonate with me, and once the protocol matures, it should meet demand. In my opinion, it is one of the most exciting versions of stablecoins this year, similar to crvUSD: I’m just waiting for the right time to try xETH.

Liquity v2: Protected LSD leverage

“Liquity v2” (codenamed) has not yet been launched, but was introduced by Robert Lauko at the last Stablecoin Summit in June.

Like fETH, v2 will provide non-clearable leverage for ETH-LSD without paying financing fees, and even increase downside protection. The protocol will output a novel, reserve-backed stablecoin optimized for scalability. As the main AMM for stablecoins, the liquidity demand for the protocol is also minimized: users can mint and exchange stablecoins with ETH pledged with just 1 USD.

V2 is being publicly built: If you want to learn more information or even participate, be sure to visit the dedicated v2 channel on Liquity’s Discord. https://discord.gg/RCRp2CJR2S

Learn more about AladinDAO’s F(x) and Liquity V2

I am keeping an eye on reserve-backed stablecoins as I may publish several articles specifically discussing this topic in the coming months. In the meantime, feel free to get your alpha straight from the builders’ mouths – here are selected articles and interviews to learn more about these two protocols:

• The recent community call where Robert and I joined the AladinDAO/Protocol F(x) team for a broader discussion on decentralized stablecoins [60 minutes] https://twitter.com/aladdindao/status/1684141750900736000?s=20

• Community Call – Deep Dive into f(x) [30 minutes] https://www.youtube.com/watch?v=_xA6AFufGoQ&t=3871s

• f(x) and AladinDAO’s Kmets and Crouger on the protocol (Leviathan News) [28 minutes] https://www.youtube.com/watch?v=Nzy7xO09SFw

• Liquity v2 introduction – Liquity blog https://www.liquity.org/blog/introducing-liquity-v2

• Colin Platt on Liquity v2 (Leviathan News) https://www.youtube.com/watch?v=KOnGCPE5gaU

Like what you're reading? Subscribe to our top stories.

We will continue to update Gambling Chain; if you have any questions or suggestions, please contact us!