Author: Zixi.eth, Investor at Jingwei China. Source: Twitter @Zixi41620514

I’m very optimistic about General L2 and vertical L2.

Analysis below:

All L1s have the problem of the impossible trinity, that is, they cannot achieve decentralization, scalability, and security at the same time. All L1s from 2018-2020 and 2021-2023 have been trying to solve this problem. The fact is that no one can achieve all three points, and a trade-off is necessary.

- Evening Must-Read | SEC Launches Final Battle Against Cryptocurrency

- Decoding OFT (Omnichain Fungible Tokens) on the decentralized exchange Trader Joe

- Understanding the Pendle Protocol for Permissionless Yield Generation in One Read

When people realized that the direction of L1 was problematic, Israel created the first Layer 2 Starkware. L2 is the project party operating node, creating its own “chain”. In a batch, there are multiple transactions that can be packaged into a single transaction submitted to the L2 contract on L1. The contract will be executed on L1, and then the main chain confirms L2 transactions. This can achieve fast and cheap transactions, and security, decentralization can also be inherited from L1.

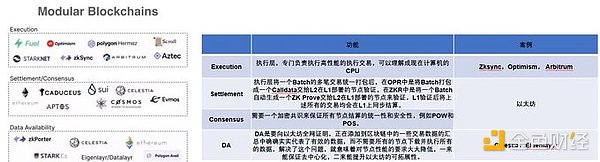

In 2022, Celestia proposed the concept of modular blockchain, that is, blockchain should be divided into four parts: Execution, Settlement, Consensus, and DA (data availability). Execution and DA are the most worthy of attention. These two parts undertake the top layer (execution) and the bottom layer (archiving transactions) of the business.

Let’s go back to 2017-2018. At that time, investment targets were mostly ethereum fork chains. The prosperity at that time doesn’t need to be said much, but why could it be so popular? This is related to the issuance of new asset types ERC 20 IEO IDO. Anyone can issue new assets without permission and let the market subscribe. This was the fuse of the bull market at that time. At that time, the investment targets that made money were L1 (eth fork) and various new asset trading platforms.

From 2020 to 2021, the investment targets, in addition to Ethereum competitors, slowly had dapps represented by defi and gamefi, and new asset types NFT can also be regarded as one of the entrances of traffic. The targets that made money and survived were L1 (eth competitor) and various asset trading platforms (in addition to the various cexdex mentioned above, NFT exchanges, and various derivatives trading platforms also began to grow and strengthen).

Let’s look at an interesting phenomenon, thanks to Boss Tang for his inspiration. Let’s take a look back at the L1s that emerged in the last cycle. At that time, we would feel that their last round of financing before being listed was expensive, but after experiencing a bull-bear cycle, when compared with the current valuation, we still feel that the valuation at that time was so cheap. But this sentence has the survivorship bias.

Why did L1 make money in the last cycle? Because: 1. People did want to solve Ethereum’s scalability issue in different ways 2. Innovations in various consensus methods 3. Everyone wanted to establish their own ecological perspective 4. The pandemic-induced easing of monetary policy led to funds flowing into the grandest story 5. Ethereum’s ecosystem did not have absolute dominance at the time.

From the perspective of General L1, I define them as large and comprehensive, with the grandest narrative. Everyone is an Eth killer, and everyone wants to create their own ecosystem. Even if you invest in the last round, or even one and a half levels after the issuance of the coin, even at the current valuation, the return is more than double, and if sold at the peak (and can be sold because it is unlocked), the multiple is quite high, which is the best solution.

Looking at L1 as a service, this seems to be a bigger and more comprehensive story than L1, but the problem is: 1. It tests the ability of team building and ecological construction more than L1 2. The token’s ability to capture value is very poor (the cosmos token is pure air, and the Polkadot slot auction has been criticized for a long time). Still, it can earn a lot, and even if you invest in the last round, the return is more than double, but the overall ceiling is relatively small.

Looking at vertical L1/L2, this is more subdivided, and indeed, from the perspective of ceiling and other angles, it is inferior to the above options. But the reason why it was not done at the time was: 1. There was no modular thinking at the time 2. Essentially, it still made an L1, and it was necessary to re-create the VM, funds, users, and development 3. The performance is still quite bad, and it cannot support enterprise-level finance or mass adoption on the consumer side. But when the trend comes, the return will be extremely obvious.

But in the next cycle, I think there may be different situations, such as ethstorage and xxxx (sell a spoiler), one solves the problem of data storage on Ethereum, and the other achieves an extreme execution layer, thus supporting consumer applications and serving high-performance derivatives/spots trading platforms for enterprises. The reason why there has been no mass adoption is that blockchain is simply not suitable for mass adoption? Not necessarily, especially when considering the financial side, blockchain or distributed technology is very suitable for mass adoption of transactions. If a fast vertical layer 2 can be created, especially a fast Chinese development team, it is likely to create a new paradigm on it.

In these two cycles, the unshakable position of Ethereum has been proven; will the public chain war reappear in this cycle? I don’t think so. The reasons are: 1. Development (30,000 developers). 2. Users (300,000-400,000 DAU). 3. Funds ($30 billion TVL). 4. Ample iteration and updates. We have confirmed the direction of Rollup, modularity, and DA in three years. Therefore, the public chain war of the next cycle will be the L2 war.

Currently, L2 is still dominated by General [purpose], which is still expensive and not fast. There is still room for improvement, and the current L2 ecosystem is not that large. The performance of L2 currently lags behind other L1 competitors. For example, for 2B type financial projects, we can use Gravity as an example.

CeDeFi on-chain derivatives are naturally designed to serve large customers, but due to the performance of Starknet, even if we make an appchain, it is still impossible to achieve on-chain matching (currently only off-chain matching and settlement). Therefore, it is still not completely transparent and trustless. If we migrate Gravity to [a different chain], it will be a high-performance and fully transparent 2B on-chain derivatives exchange.

Can we take a different approach and temporarily abandon some of the decentralized capabilities to create a very high-performance L2 to differentiate and compete with the current General L1? This L2 may not be suitable for DeFi, but it is very suitable for consumer projects (such as games or e-commerce) and some enterprise-level financial projects (orderbook exchanges for on-chain matching). This creates a possible soil for potential mass adoption.

Currently, this type of vertical layer 2 may provide good infrastructure for achieving mass adoption dApps by taking a different approach, but this may require improvements in hardware storage, parallel MEV, data structures, etc. Let’s wait and see the progress of high-performance vertical L2 in six months or a year. See if we can achieve mass adoption on them two or three years later, whether it is for consumption or finance.

Like what you're reading? Subscribe to our top stories.

We will continue to update Gambling Chain; if you have any questions or suggestions, please contact us!