Author: GABE TRAMBLE

Translation: Deep Tide TechFlow

Introduction

For some people, Automated Market Makers (AMM) are the only thing of interest in decentralized exchanges (DEX). Centralized exchanges often exclude these assets due to low liquidity and reliance on traditional market makers. Whether it’s Uniswap, Curve, Balancer, or aggregators like MetaMask and 1inch, AMMs have facilitated trillions of dollars worth of transactions since their inception a few years ago. The permissionless design of DEX makes it an ideal platform for trading low liquidity or long-tail assets, as anyone can create a market for new assets. Unlike traditional CEX, which requires manual integration of assets, AMMs can seamlessly deploy and trade any ERC-20 token as long as someone provides liquidity. This is because AMMs allow anyone to deposit assets and become a market maker without the need to be an institutional entity like in traditional finance (TradFi). Market makers increase liquidity on exchanges by providing buy and sell orders to ensure users can execute trades without relying on other users. They make money by exploiting the price difference between buying and selling.

- Week 36 On-chain Report in 2023 Continuous outflow of funds may reveal weakening market sentiment.

- Secondary Market Observation Livepeer (LPT) market resumes, can it break the previous high?

- Less than 48 hours of ‘bull market’ SEC delays Bitcoin ETF, market responds with a decline.

However, most spot AMMs are very basic and typically only support buy and sell orders. Some spot AMMs and aggregators offer advanced features such as limit orders and deep liquidity (liquidity sufficient for large entities to trade). However, they still cannot translate their liquidity into other trading primitives.

In the product world, it is often said that a product needs 10 times improvement to replace existing products and achieve significant adoption. The introduction of DEXs like Uniswap solves the liquidity problem by allowing users to create markets for any ERC-20 token at lightning speed.

DEXs like Uniswap and Curve have been battle-tested for a long enough time and can be used as primitives for other products.

Similar to DEX spot markets, other trading products such as perpetual futures (Perps) and options are also fiercely competitive and still dominated by CEXs in terms of trading volume. Despite the dominance of CEXs, there is still a huge growth opportunity for perpetual futures, options, and other trading products by leveraging the composability of DeFi, stacking DeFi “building blocks,” or building applications that can interact with each other.

Most on-chain perpetual futures and derivatives have only a few assets, use oracles, and are susceptible to liquidity issues. Without sufficient liquidity, derivative exchanges cannot operate and attract more users, which is the so-called chicken and egg problem. To achieve this goal, new protocols are leveraging centralized and constant function AMM liquidity to drive new trading products (leverage, perpetual futures, and options). In short, the protocol uses AMMs like Uniswap as liquidity primitives to create new trading products.

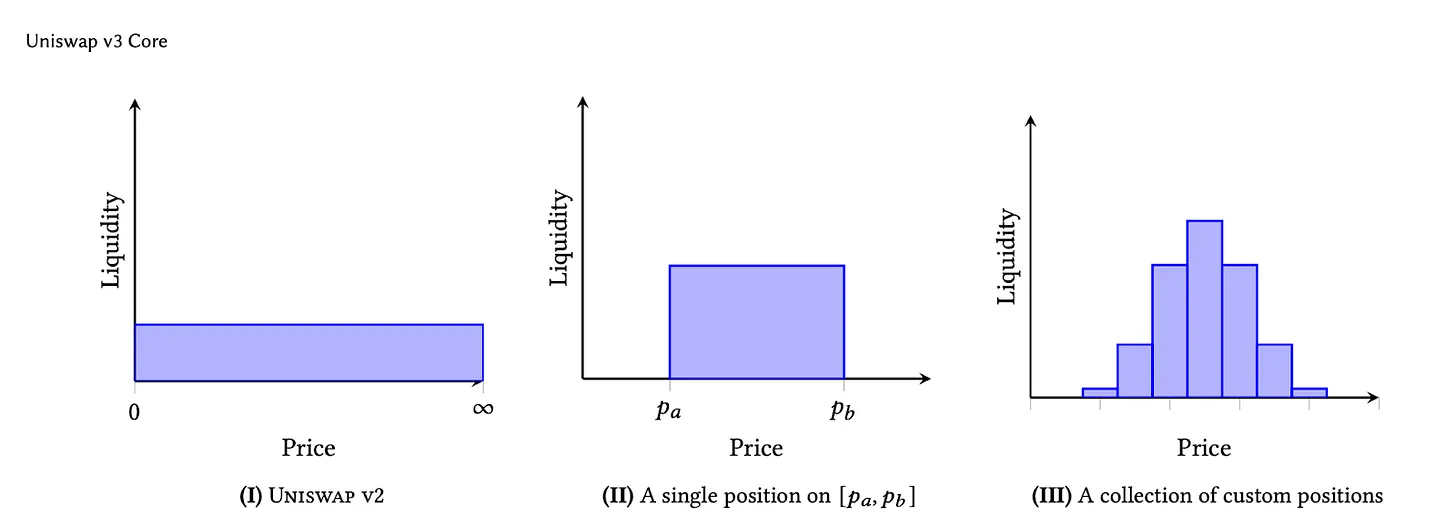

- Constant Function AMM: Liquidity is typically spread infinitely across the entire price range (Uniswap v2, Balancer).

- Concentrated Liquidity AMM: Liquidity is concentrated within a price range (Uniswap v3).

The Moment of Uniswap for Perpetual Futures and Options

The killer use case for AMM-driven trading products is the ability to create perpetual futures (Perps), hybrid options, and other volatility markets for illiquid and newly deployed assets. During its FOMO period, $PEPE skyrocketed to a market cap of billions of dollars in just a few weeks. In this highly volatile period, traders repeatedly asked, “Where can I go long on $PEPE?”

Despite the significant increase in popularity of PEPE, attracting billions of dollars in trading volume, initially only spot markets were available to trade the asset. Several weeks later, some exchanges began supporting perpetual futures (Perps) trading, and it has remained the sole trading source even until now. Even on some exchanges that support $PEPE trading, many traders believe there are issues with liquidation and settlement, which are core problems in the design of perpetual exchanges. Through AMM-driven volatility products and derivatives, LPs have the opportunity to marketize options and perpetual futures on token issuance, similar to Uniswap.

Crypto assets have a significant speculative demand, especially in terms of leverage. Apart from leverage, these products provide good tools for hedging LPs’ positions on assets.

Perpetual Trading Products

Many on-chain perpetual contracts rely on oracles, which can be easily manipulated for long-tail assets. Oracles convert off-chain data into on-chain data that protocols can use, usually for price feeds. Have you ever wondered why decentralized exchanges for perpetuals only support a few assets? Most on-chain Perps and options platforms only offer a handful of assets aimed at achieving deep liquidity and utilize external oracles as pricing mechanisms. Liquidation risk is also a significant issue as managing liquidation relies on accurate oracles and ensuring that trades can be liquidated in a timely manner to meet collateral requirements. In other words, liquidations need to happen seamlessly to ensure there is enough collateral to cover the trades. Through Concentrated Liquidity AMMs (CLAMMs)-driven trading products, oracles and liquidation risk are often eliminated as liquidity is borrowed from pre-defined LP ranges.

By adopting this approach, traders’ risk is also predefined and limited within the parameter range set by the exchange protocol for closing positions. Many protocols that enable AMM LPs use perpetual mechanisms to determine the duration of trades, and as long as fees are paid to keep the positions open, the trade duration continues.

AMM and LP Fees

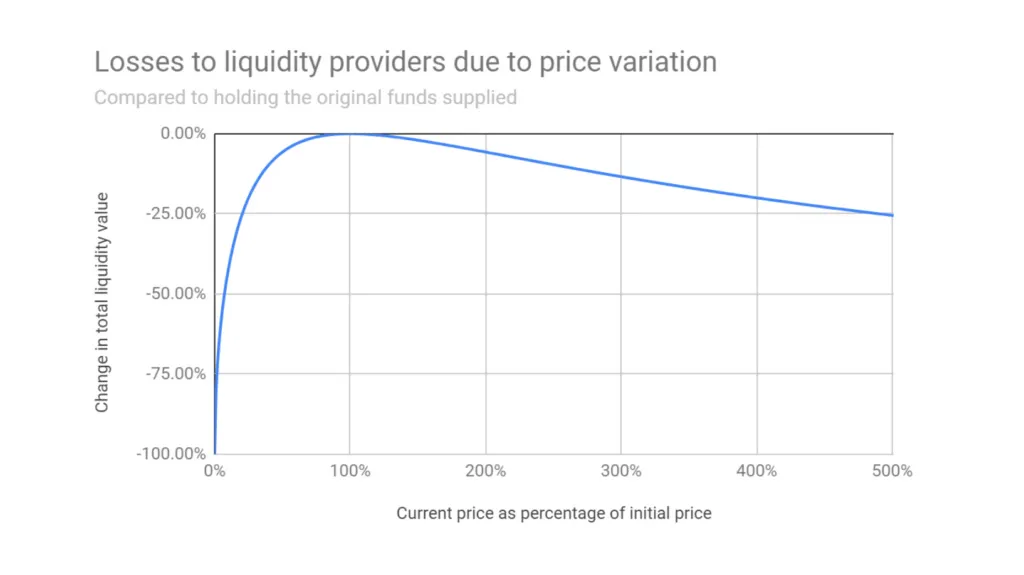

Concentrated Liquidity Automated Market Makers (CLAMM) and Constant Function Automated Market Makers (CFAMM) constitute a two-sided market involving liquidity providers (LPs) and traders. For traders, the experience with AMM products is mostly similar. On the contrary, many exchanges strive to optimize the experience of providing liquidity, as it often leads to losses. In many cases, LPs need additional incentives to make a profit.

Many liquidity providers add liquidity to AMMs based on the assumption that they will receive enough fees to offset impermanent losses (IL). It is also worth noting that not all LPs adopt a HODL strategy. A core improvement to the centralized AMM liquidity derivatives model is that LPs now receive compensation not only through trading fees but also through volatility. This innovation introduces a new dimension to the rewards for providing liquidity.

For certain AMM-driven derivatives, such as infinite pools and LianGuainoptic (LianGuainoptic Option Sellers), LPs can generate fees when they are within a range and commission fees when they are outside the range. When LP tokens are outside the range, they can be used for protocol volatility products, whether it’s leveraged trading, margin trading, or options trading.

How do AMM LP-driven trading products work?

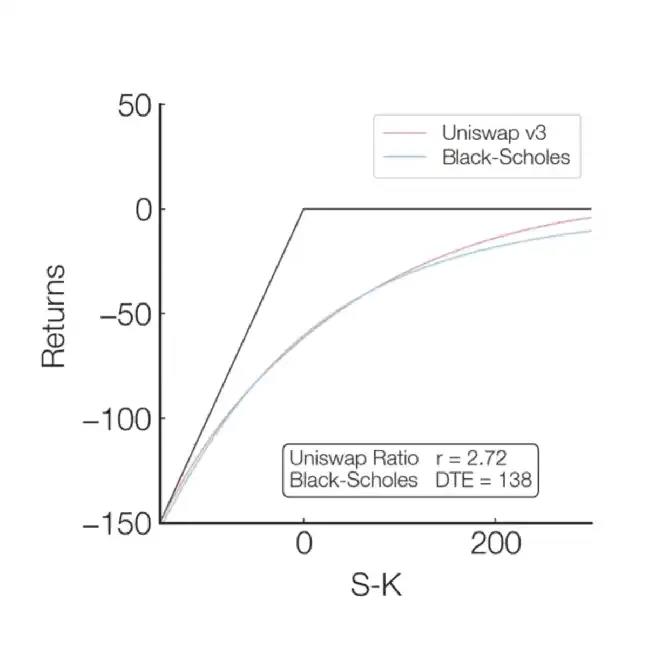

Currently, protocols that offer AMM-driven trading derivatives follow a simple assumption: providing LPs in CLAMM is similar to selling put options. In other words, the return structure for liquidity provision is mathematically similar to selling put contracts. Perpetual and volatility trading protocols are able to build trading derivatives and strategies around this concept, creating leverage, perpetual futures, perpetual options, and other structured products.

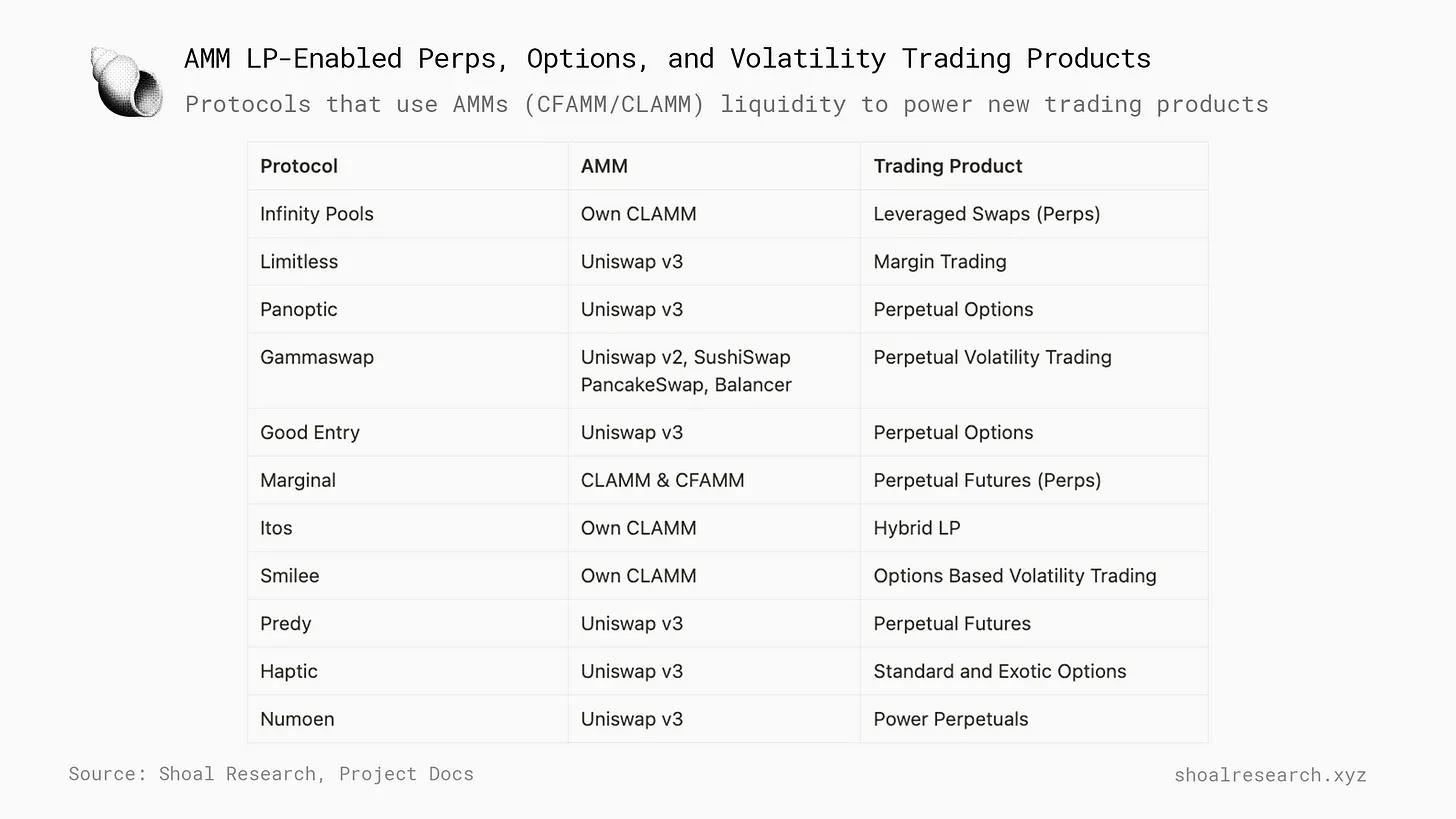

Protocol Overview

Currently, there are several protocols aimed at utilizing CFAMM and CLAMM liquidity for trading. Some of these trading products include leverage and margin trading, options products, perpetual futures, and more. Although this concept is still novel, many developers have found opportunities to fill the liquidity and asset gap in trading products between major assets and long-tail assets. The table below shows the protocols, their liquidity AMMs, and the trading products created:

Let’s further explore the mechanisms and designs.

Perpetual Options Mechanism Design

Protocols like LianGuainoptic and Smilee utilize centralized liquidity LP to support their trading products, including perpetual options and volatility trading. Among the few protocols that utilize existing AMM centralized liquidity, each protocol presents slightly different architectures and implementations in building trading products.

At a high level, the protocol extracts centralized liquidity from AMMs such as Uniswap v3 or its own AMM, and allows traders to borrow these assets. Traders then redeem the underlying LP tokens to obtain a single asset, simulating long or short positions limited to the range of centralized liquidity. Due to the nature of centralized liquidity positions, they always consist of 100% of one of the assets in a pair (e.g., USDC/ETH) when outside the range. As LPs expect to hold 100% of a pair of assets in the liquidity pool, traders need to pay fees to borrow and redeem LP tokens to obtain one of the assets. Depending on their trading strategy, they can sell the redeemed tokens and convert them into directional bets.

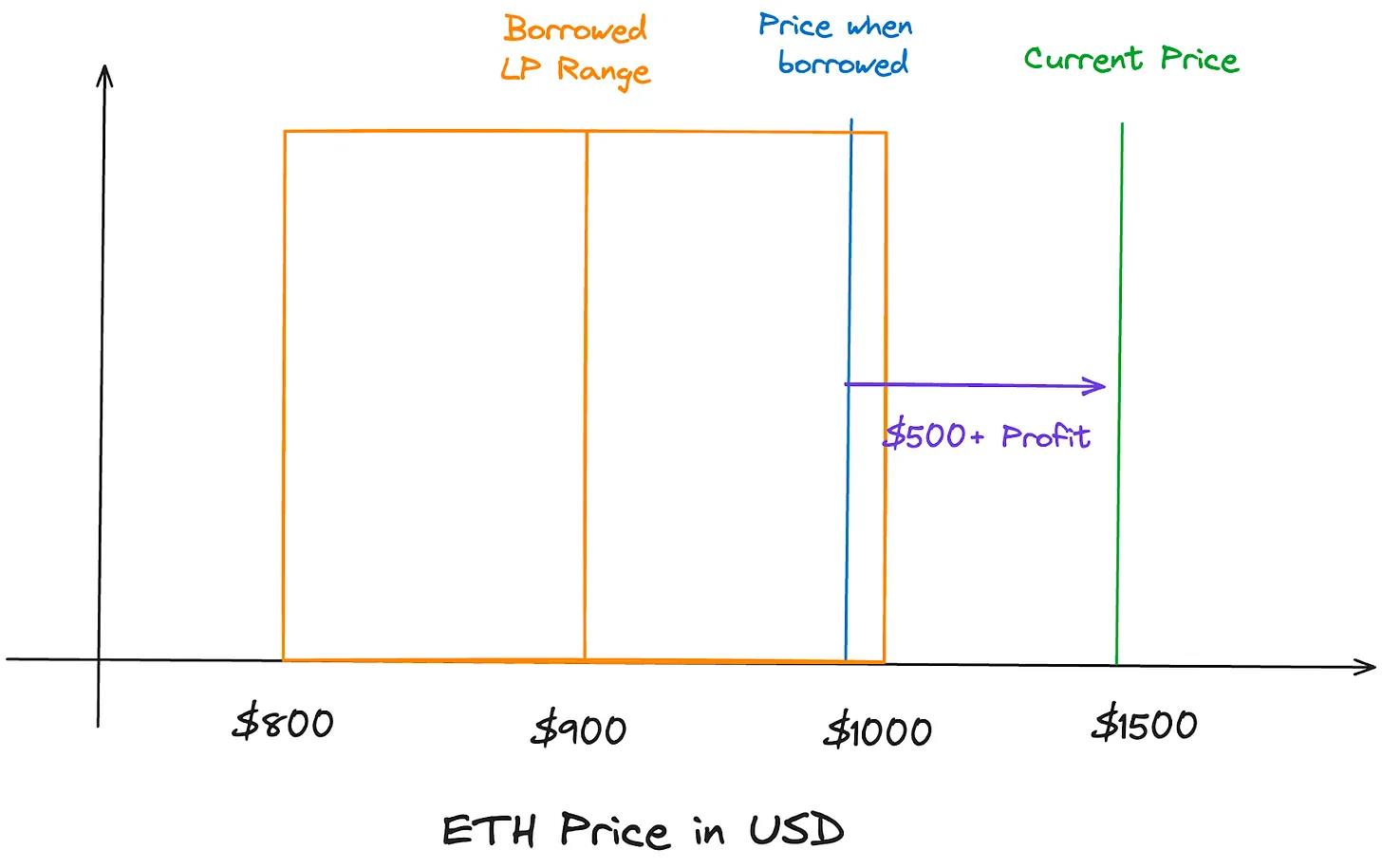

Example: Long ETH

Using perpetual options as an example, let’s assume a trader wants to borrow a USDC/ETH LP token where ETH is priced at $1000. The trader wants to go long on ETH, so they borrow the out-of-range USDC/ETH LP token at a price lower than the current price, valued at $1000 USDC. The LP token is valued at $1000 USDC because the current price has moved to the right of the range, causing the LP (the option seller) providing liquidity to hold 100% USDC. The strike price for the option buyer can be seen as the midpoint of the LP range; in this example, we’ll use 900. As the trader is long, they redeem the LP token valued at $1000 USDC and exchange it for 1 ETH valued at $1000 as well. If the price of ETH rises to $1500, the option buyer can exercise the option by selling 1 ETH at a price of $1500, as the value of ETH now exceeds the value when the option buyer purchased it, earning them a profit of $500. The option buyer only needs to repay the LP $1000 because that is the endpoint of the liquidity range they provided.

Protocols typically abstract away most of the complexity. Users may need to deposit collateral to fund the position, select the position duration (if included), the strike price, and the direction of the trade.

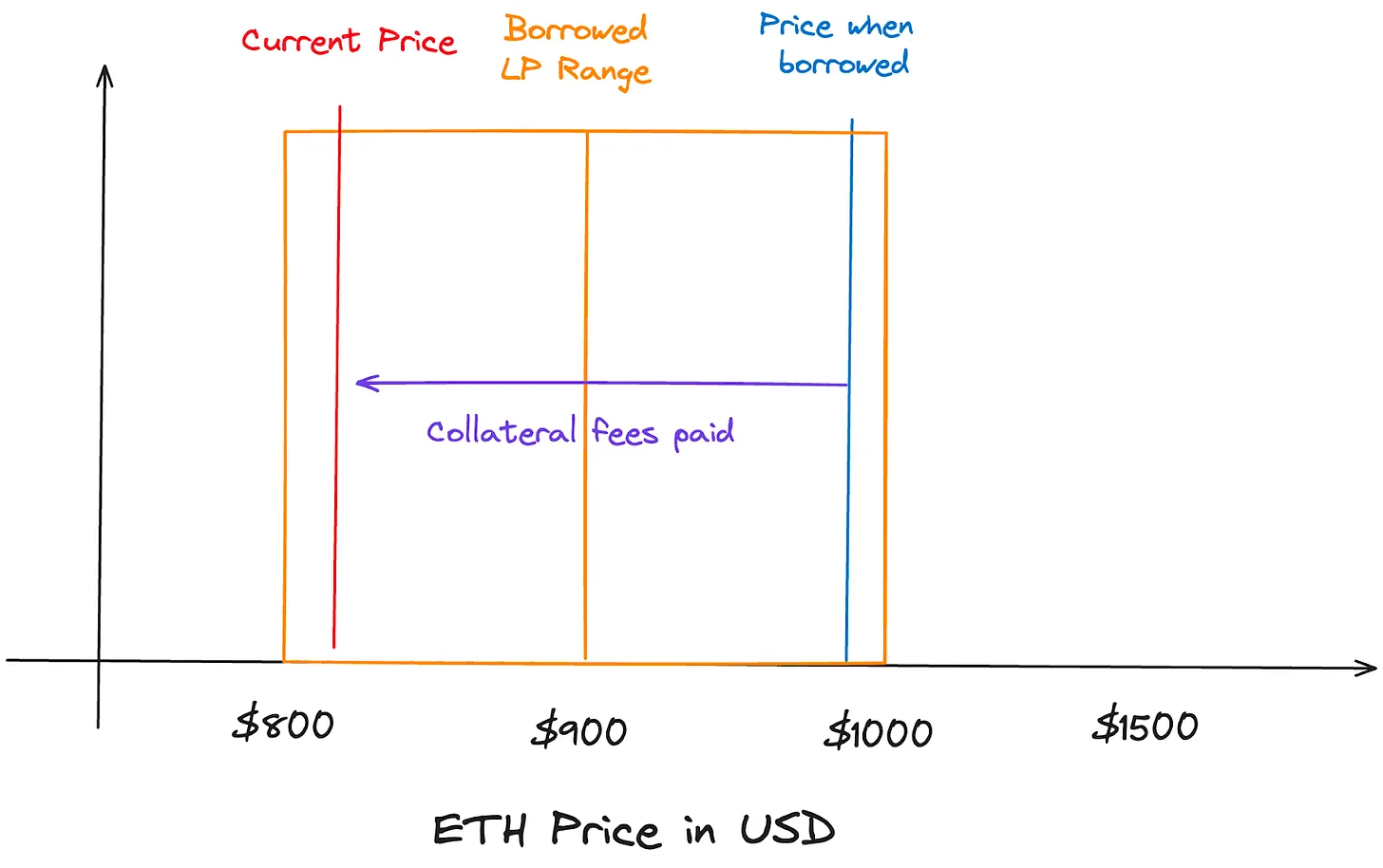

If the trade doesn’t go as planned and the price of ETH drops to $800, outside the opposite direction of the LP range, the borrower now owes 1 ETH instead of USDC. Since the borrower still owes 1 ETH, they need to find a way to acquire 1 ETH to repay the loan. If the value of 1 ETH is $800, the borrower needs to use $800 USDC to purchase 1 ETH to settle the debt.

Decentralized exchanges (DEX) manage protocols like LianGuainoptic to ensure LPs receive rewards. Unlike pre-paying a premium to purchase options, LianGuainoptic requires users to have initial collateral in their wallets to pay for liquidity fees similar to funding rates. Collateral is needed to guarantee fee payments. These fees are determined based on the realized volatility and utilization rate of the underlying Uniswap pool to determine how much the option buyer should pay the seller (LP) in fees. When a trader stops paying funding fees or the funding fees exceed their collateral, their position will be liquidated.

In both examples, the option seller continues to collect liquidity fees to maintain their position. This is a general overview related to LianGuainoptic as each protocol has different approaches in managing liquidity, providing leverage, calculating collateral, premiums, and funding fees.

From a bird’s-eye view, the transaction is bilateral, where LPs deposit their LP tokens into the protocol and receive volatility fees, while traders can open positions. LPs are incentivized to provide liquidity as they can earn rewards that surpass other methods. A core issue for LPs in AMMs is that their fees are not sufficient to compensate for the risks. Finally, profitable traders can exercise their profit positions or continue to pay funding fees to keep the trade open for LPs.

Perpetual Futures Mechanism Design

For perpetual platforms like limitless or InfinityPools, the mechanism is similar to perpetual options. However, users can deposit collateral that combines with borrowed LPs. The required collateral and leverage are determined based on the distance from the spot price. Similar to perpetual options, if a trader borrows LP tokens below a range, they can sell one of the underlying tokens to create a directional leveraged bet. The design mechanism is very similar to the previous examples, with the main difference being the collateral deposited by the user, which covers the maximum loss when the trade moves in the opposite direction. Both limitless and InfinityPools claim to offer leverages of hundreds to thousands, depending on the distance between the range and the current price. If a trader incurs losses in a trade, the protocol will close their position and pay the collateral to LPs to keep the perpetual futures seller’s LP position intact.

Market Opportunities – Cryptocurrency Trading Derivatives

Traditional Financial Market Size

According to Sifma Asset Management’s data, the US stock market dominates globally, accounting for over 42.5% of the global stock market value of $108.6 trillion in 2023, equivalent to $44 trillion.

Traditional Financial Derivatives Market

The nominal value of the derivatives market is estimated to be over $100 trillion, although some believe this valuation may be exaggerated, according to Investopedia. This astronomical figure includes the nominal value of all derivative contracts.

There is a significant difference between the nominal value and the actual net value of derivatives. As of 2021, these two figures are $600 trillion and $12.4 trillion, respectively.

In traditional finance, the scale of derivative trading is much larger than spot trading. The same is true for the cryptocurrency market, but most of the trading volume occurs on centralized exchanges (CEX).

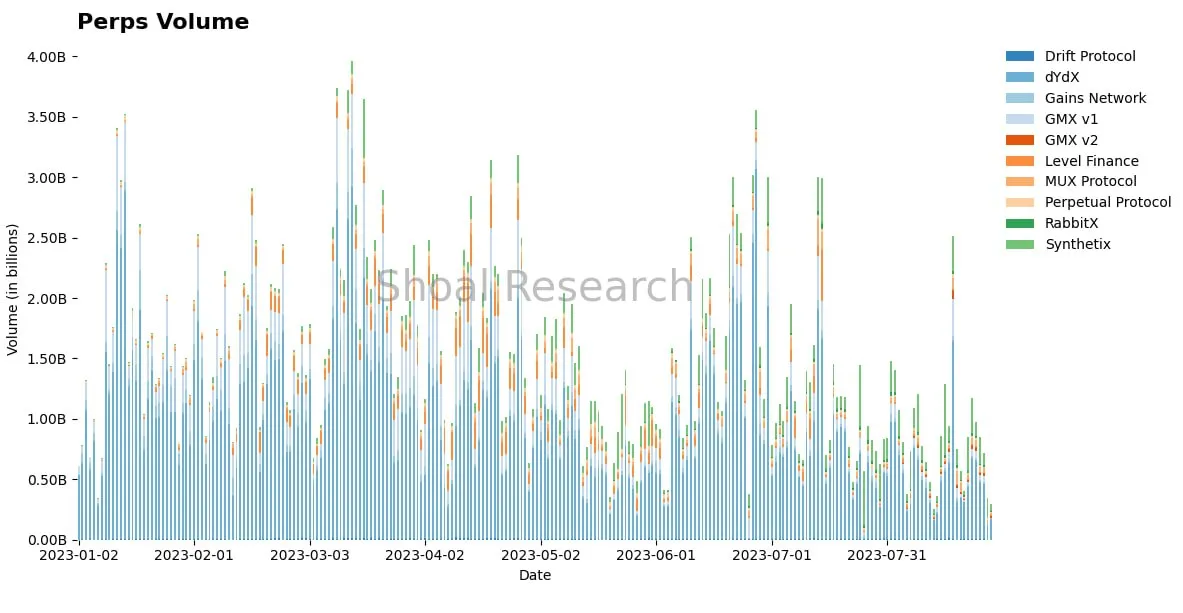

Bitmex is another centralized exchange that launched their perpetual (Perp) trading tool in 2016, namely perpetual XBTUSD leveraged swap. Their new product allows users to trade bitcoin (XBTUSD) with leverage of up to 100x. The contract has no expiration date; longs pay shorts and vice versa. As the largest trading instrument in the cryptocurrency market, this product has expanded from centralized exchanges to various decentralized versions such as DYDX, GMX, Synthetix, etc. Perpetual protocols facilitate billions of dollars in trading volume every day and are the main derivative trading products in today’s cryptocurrency market because they offer high leverage. This is a huge shift that is completely different from traditional finance, where options dominate the derivative market.

Cryptocurrency Spot Trading vs. Perpetual Futures

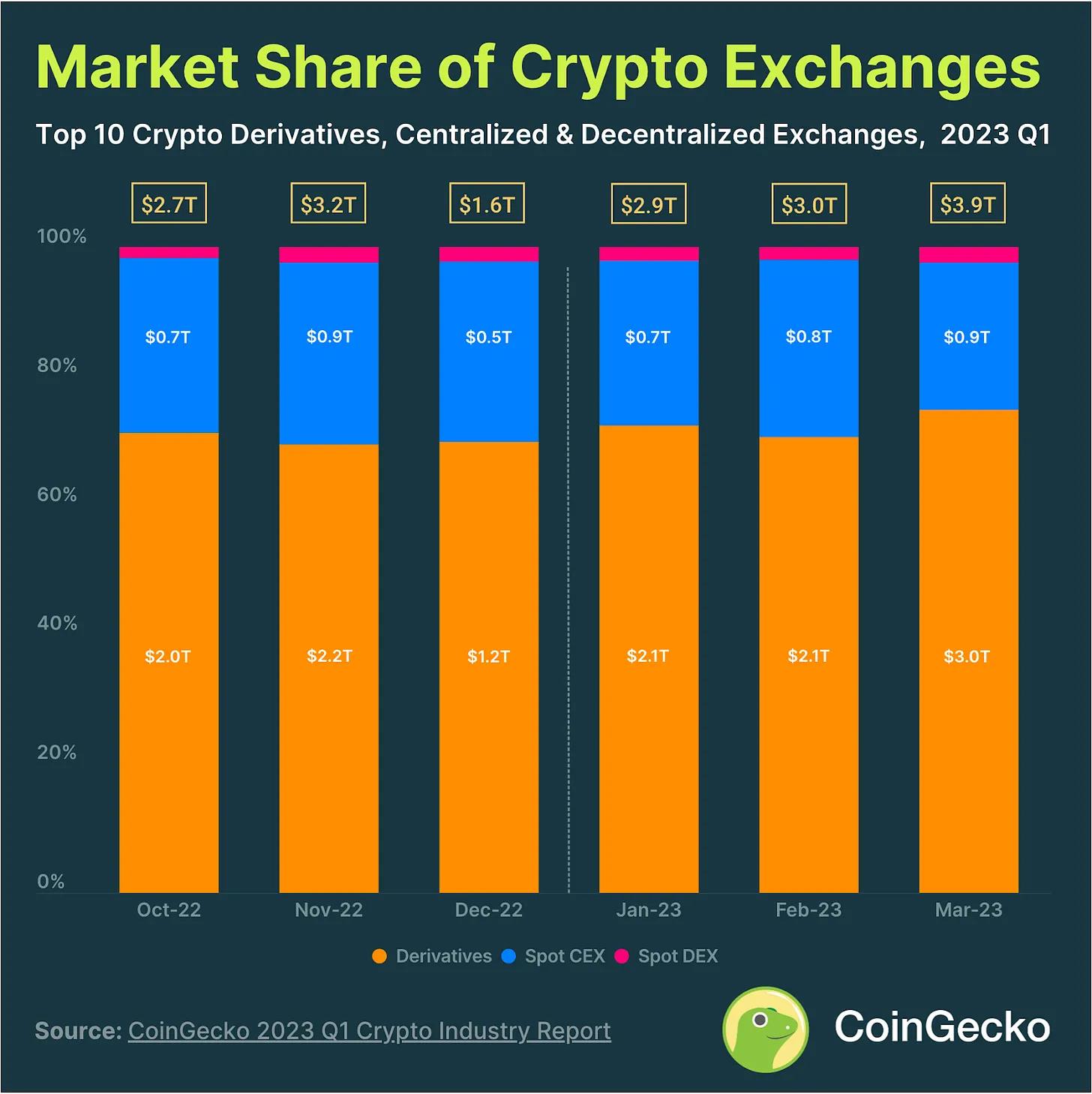

In the first quarter of 2023, derivatives accounted for 74.8% of the total trading volume in the cryptocurrency market, amounting to $2.95 trillion. The market share of spot trading on centralized cryptocurrency exchanges (CEX) and decentralized exchanges (DEX) was 22.8% and 2.4%, respectively. It is worth noting that centralized cryptocurrency derivative exchanges like Binance, Upbit, and OKX dominate the market. According to Coingecko’s 2023 Cryptocurrency Derivatives Report, while derivatives trading volume increased by 34.1% year-on-year, spot trading growth rates for CEX and DEX were 16.9% and 33.4%, respectively.

As of July 2023, 74% of cryptocurrency trading volume was conducted with leverage.

Innovative volatility trading platforms such as LianGuainoptic, Infinity Pools, Smilee, etc., are driving industry growth by offering high leverage without the need for oracles or clearing, and in some cases, providing high leverage. With the support of concentrated liquidity, AMM LP trading products eliminate some prominent weaknesses, such as managing oracles and clearing.

Risks

Although these products can be exciting, risks still exist. The most significant is smart contract risk. As all AMM-LP trading products control LP tokens or require deposits, there is a possibility of smart contract risk if there are vulnerabilities or errors.

Credit Liquidity Risk

In addition, there are also some issues with the economic design mechanism. The Gammaswap team conducted an investigation into the feasibility of developing on Uniswap v3 and CLAMMs because they believe there is “credit liquidity risk”. This risk involves liquidity providers (LPs) being unable to pay long positions or vice versa, usually due to liquidation issues caused by excessive leverage. Due to concentrated liquidity, automatic market makers (AMMs) like Uniswap have areas or “ticks” with lower liquidity, and prices exceeding the range can lead to excessive slippage, even for stable trading pairs. Gammaswap chooses to build on the constant function model, believing it to be a more powerful liquidity primitive.

In Uniswap v3, there may not be enough liquidity to meet the returns of LPs. Unlike traditional finance, where the Federal Reserve can inject liquidity, there is no similar entity in the DeFi space. Additionally, the lack of oracles traditionally used for liquidation adds complexity to this issue.

LianGuainoptic solves the credit liquidity risk issue by requiring pool creators to deposit a small amount of two tokens across the entire range, which traders cannot remove. The initial deposit ensures that there is liquidity in all price ranges.

Complexity and User Adoption

It turns out that perpetual futures (Perps) are easier for cryptocurrency investors to understand. They operate through two mechanisms: long and short positions, and traders can open positions with a simple click of a button. In contrast, options and potential perpetual options introduce additional complexity, such as Greek letters, strike prices, and other traditional option knowledge, which may hinder user adoption. This is especially likely among retail investors, who are often the earliest adopters of new trading tools. Additionally, introducing volatility trading adds to the complexity of the user experience. As the cryptocurrency space has already faced challenges with user adoption, some complex yet powerful products may struggle to gain widespread acceptance due to their financial complexity.

Conclusion

Perpetual futures and options have found their place in the cryptocurrency space, and it is only a matter of time before they are developed into mature products sought after by traders and LPs.

In the coming months, many of the mentioned protocols will launch beta versions and actual products of new trading tools. The next improvement of on-chain derivatives, including perpetual contracts and options, will be the introduction of the ability to leverage long (or short) any asset. The question of “Where can I go long on PEPE?” will be answered by providing leverage liquidity trading channels for mid- to long-tail assets.

AMM-driven trading products pave the way for a new trading paradigm and have the potential to realize new DeFi paradigms supported by other protocols. This includes options, perpetual contracts, volatility trading, and other leverage-based products. An improved trading experience will provide a more outstanding experience that can even rival existing products on the market.

Like what you're reading? Subscribe to our top stories.

We will continue to update Gambling Chain; if you have any questions or suggestions, please contact us!