A client came to consult in Manchester not long ago. The basic situation is as follows: The client is a foreign trade company in Guangzhou. After completing a transaction with an overseas company, the client’s original intention, of course, was to settle the payment through normal channels. However, the overseas company couldn’t make the payment for some reason, so they proposed a feasible solution to “settle the payment in USDT”. After careful consideration to avoid any potential risks, the client agreed and quickly received the USDT payment from the overseas company. They then found a domestic “service provider” to cash out the USDT (exchange it into RMB). As you can imagine, the result of seeking legal assistance from Manchester Lawyers was that once the “service provider” received the USDT, they became unreachable and couldn’t be found.

Many people may think that “anything related to virtual currencies is doomed to be more bad than good” when they first hear about this consultation. Considering that virtual currencies have different regulatory policies in different countries, using USDT as a settlement method has become one of the collection options for some foreign trade companies. However, it should be noted that the traditional collection methods in the foreign trade industry already have many pitfalls (risks). Is it really appropriate to choose USDT as a collection method?

01 Common problems faced by cross-border foreign trade merchants in receiving payments

It is very easy for small and medium-sized foreign trade enterprises to step on landmines when it comes to cross-border collection. Some businesses have even been deceived and ultimately had to withdraw from the market in disappointment. Therefore, in foreign trade transactions, payment is a matter of great concern for both buyers and sellers. Small and medium-sized foreign trade companies face rising comprehensive costs, operating risks, and pressures, to varying degrees, leading to phenomena such as “not daring to take orders” and “increasing revenue without increasing profits”. This is because foreign trade companies encounter many problems when collecting payments, including but not limited to: ① lengthy account opening process, slow payment processing time, and high withdrawal fees; ② support for too few currencies, with existing channels not supporting small currencies; ③ limited RMB withdrawal limits; ④ inability to withdraw funds at real-time exchange rates; ⑤ inability to directly pay suppliers; ⑥ difficulties in receiving payments from high-risk regions; ⑦ even encountering problems such as frozen cards and frozen funds. For both domestic and foreign trade merchants, the return of funds in cross-border settlement is undoubtedly a very important link, and the difficulty of receiving payments is a real problem they face. In order to avoid the problems encountered in reality, many foreign trade merchants now give up collecting payments through legal and compliant methods and channels. Instead, they rely more on “underground banks” to recover funds.

- Fireblocks CEO Institutions Still Avoiding Cryptocurrency Risks

- a16z crypto and others establish the Crypto Freedom Alliance, advocating for clear regulation.

- SEC Chairman Cryptocurrencies Must Comply with Securities Laws

02 The operation mode of cross-border “underground banks”

Normally, cross-border payments refer to the international transfer of funds between two or more countries or regions due to international trade, international investment, and other aspects, using certain settlement tools and payment systems. In actual economic activities, there are quite a few domestic cases where “underground banks” are used as settlement methods for cross-border trade.

“Underground banks” is not a definite and standardized legal concept. It mainly refers to “a special illegal financial organization that operates outside the financial regulatory system, using or partially using the settlement network of financial institutions to engage in illegal foreign exchange trading, cross-border fund transfers, fund storage, lending, and other illegal financial activities.” Its essence is an underground bank that operates foreign exchange, lending, and payment settlement financial activities without the approval of the country, providing a funding channel for corruption, gambling, smuggling, tax evasion, and tax evasion. It is also a form of money laundering crime (relevant regulations: “Anti-Money Laundering Report” issued by the People’s Bank of China in 2005, “Measures for the Prohibition of Illegal Financial Institutions and Illegal Financial Activities” promulgated and implemented by the State Council on January 8, 2011).

Although it carries the label of “illegal,” the existence and prosperity of “underground banks” have always been an open secret. Currently, the operation of domestic “underground banks” mainly includes three types: cross-border “offsetting” model, “payment settlement” model, and other illegal operating models.

1. Cross-border “offsetting” model

This refers to the use of onshore RMB settlement and offshore foreign currency settlement, with funds not crossing borders in terms of form (referred to as “cross-border settlement model”), to achieve substantial exchange and cross-border transfer of funds. This is currently the main operating mode of underground banks, mainly used to transfer domestic illegal income and other funds to overseas and to evade foreign exchange in cross-border trade through underground banks.

2. “Payment settlement” model

This refers to the use of false deceptive means, fabricating or creating legitimate transaction forms to conceal illegal purposes, and achieve illegal cross-border transfer of funds in the “payment settlement” model. For example, using props goods for import and export to achieve cross-border fund transfers, and using shell companies and fake trade for public-to-private transfers.

3. Other illegal operating models

The operation models of underground bank syndicates are often diversified and also referred to as comprehensive underground banks. Common methods include currency speculation, illegal modification of mobile phone devices for overseas use, overseas cash withdrawals using bank cards, illegal splitting of foreign exchange purchases, and cash smuggling. In recent years, to evade crackdowns, there have also been cases of illegal cross-border transfer of funds using virtual currencies and fourth-party payment platforms.

In summary, regardless of the above-mentioned models, the profit-making methods of “underground banks” can be summarized as follows: earning price differences by buying foreign currency at a low price and selling it at a high price, charging clients a certain percentage of fees or commissions based on the amount of exchange transactions and fund lending, and obtaining illegal profits through trading deception, government rewards, export tax refunds, and other cross-border arbitrage.

03 Risks of Choosing USDT for Cross-Border Trade Settlement

When domestic and foreign traders choose a settlement method, why do they choose to receive USDT? The most probable reason is based on the aforementioned difficulties that already exist. Choosing USDT conveniently avoids some of the difficulties in receiving payments. However, what they receive in their hands is virtual currency, not real gold and silver. After receiving it, they have to decide whether to hold, invest, or cash out. These are the practical issues that domestic traders need to consider. Considering that China’s current regulatory policies for virtual currency are so strict, whether it is receiving, holding, investing, or cashing out, it is all high-risk situations.

1. Risks of receiving USDT

If overseas buyers convert their foreign currency into USDT through “underground banks” or over-the-counter exchanges, domestic traders provide them with a wallet address for receiving USDT, and overseas traders pay USDT according to the requirements of domestic traders, it seems that receiving payments through USDT is very fast and avoids restrictions such as currency, foreign exchange, and taxation. However, if we analyze it further, we will find that because overseas traders convert their own funds into USDT through “underground banks” or over-the-counter exchanges, it is difficult for domestic traders to identify the legitimacy of the source of funds, and risks follow.

Assuming that the funds of overseas traders are illegal, based on our previous case handling experience, we can preliminarily predict that the reason why overseas traders want to convert their own funds into virtual currency is nothing more than to launder the originally illegal funds through “underground banks” or over-the-counter exchanges. Domestic traders, as a link for receiving USDT (or other virtual currencies), are very likely to be implicated in the process of case investigation. In the end, the inability to recover the foreign trade funds from this transaction is a small matter, but if it is determined as a criminal offense, the gain is not worth the loss.

2. Risks of holding USDT

After domestic traders receive USDT, if the aforementioned criminal risks do not occur, can they consider it secure? Not really, the value of virtual currency in China may not be realized, but some countries have already recognized virtual currency as legal property. If domestic traders receive USDT and do not immediately convert it into RMB, but plan to observe the international market situation before making a decision, and the value of USDT appreciates, why not take advantage of it?

However, theft of virtual currency (whether it is Bitcoin or USDT) is not something new in the cryptocurrency circle. It is believed that in order to have a glimmer of hope of recovery, domestic traders will choose to attempt to report a criminal case. However, due to the current domestic laws and regulatory policies, combined with our previous cases and public judgments on criminal cases, whether virtual currency has the attribute of property is the key to determining whether it can be identified as a criminal offense. Some courts have determined the property attribute of virtual currency, and generally file investigations based on theft charges. However, from practical experience, regardless of whether a criminal case is filed or not, the difficulty of recovering stolen virtual currency (USDT) is relatively high.

3. Risks of Investing in Virtual Currency

Of course, holding USDT is not the ultimate goal for domestic merchants. Ultimately, they want to gain some benefits through USDT and may use the received USDT for investment. In real economic activities, most of the time, when entrusting others to invest in virtual currency on their behalf, there will not be a written contract, which is what lawyer Zhou often refers to as “naked investment”. In case of “investment failure” (which could be due to the project going bad or the project party not performing at all), the court generally determines the establishment of the entrusted investment contract based on materials such as chat records and transfer records between the two parties. However, the establishment of the entrusted contract does not mean it is effective. Many court judgments consider the contract to violate financial regulatory policies, the virtual currency itself to be an illegal subject matter, or the contract to violate public order and good customs, and therefore deem the contract invalid. Of course, there are also a few typical cases that recognize the validity of entrusted investment contracts for virtual currency.

The legal consequences resulting from the determination of the invalidity of the entrusted investment contract for virtual currency are also different. Some courts require both parties to bear partial responsibilities based on this; some courts believe that the investor should bear the risk based on the “Notice on the Prevention of Risks Associated with Token Issuance and Financing”; and some courts believe that debts related to virtual currency are illegal, and thus the law does not protect the investor’s property.

Therefore, if domestic merchants engaging in cross-border trade receive USDT and consider using it for investment, they should be aware of the possible consequences of the invalidation of the entrusted investment contract and the risk they will bear, and make investment decisions cautiously.

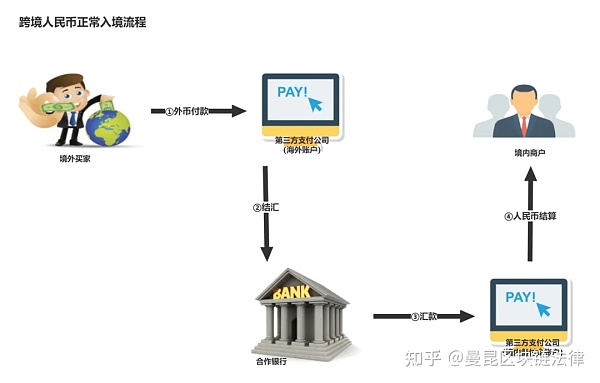

4. Risks of Cashing Out USDT

Whether it is through traditional payment methods or receiving USDT, the main purpose of domestic merchants is to receive payment and achieve the turnover of funds. As mentioned at the beginning of the consultation, the ultimate goal is to convert USDT into RMB. However, according to China’s existing regulatory policies, the possibility of legally converting it into RMB through domestic institutions is very slim. Therefore, the only options for cashing out are: exchanges and over-the-counter (OTC) markets (or underground banks). Regardless of which service provider is chosen, it has already bypassed the legal and compliant process of cross-border RMB inflow. The process of receiving USDT payments can be briefly summarized as follows: overseas merchants convert foreign currency into USDT → domestic merchants provide a wallet address to overseas merchants → overseas merchants transfer USDT to the wallet address provided by domestic merchants → domestic merchants exchange it for RMB through exchanges or OTC markets (or underground banks), perfectly bypassing the national foreign exchange and tax management system and overcoming the problem of slow processing time. However, there are also various risks involved. If the RMB obtained through the exchange of USDT contains illegal funds, the bank account or funds may be frozen, and the public security organs may require cooperation in the investigation, with no definite timeline for unfreezing; there is also the possibility of being implicated in criminal cases such as money laundering and concealing criminal proceeds. Even if the RMB obtained through the exchange of USDT is all legal funds, bypassing the legal and compliant process of RMB inflow may constitute illegal buying and selling of foreign exchange, tax evasion, etc. Once relevant authorities start investigating, criminal or administrative penalties may be imposed.

Of course, even if the relevant national units or departments do not pursue it, the process of cashing out USDT is not necessarily foolproof. Just like the situation where the service provider disappears and runs away after receiving USDT, it is not an exception. This is also because the current regulatory attitude in our country is strictly to prohibit speculation in virtual currencies. It can be imagined that it would be difficult to recover the already paid USDT. In this way, it was expected to avoid problems such as foreign exchange, taxes, high fees, and slow processing time, but in the end, it may be fruitless.

04 Summary by Lawyer Man Kun

Speaking of this, I believe that domestic merchants already have their own ideas about whether to choose USDT (or other virtual currencies) for settlement. As a law firm engaged in the web3.0 industry, we have been paying attention to the process of legalizing virtual currencies in China. It can only be said that it is still in the stage of strict regulatory measures. It is recommended that domestic merchants choose cross-border settlement methods on the premise of legality and compliance. Finally, let’s summarize today’s topic:

1. The main reasons why domestic and foreign trade merchants have difficulty receiving payments are: long account opening process, slow payment processing time, high withdrawal fees; support for too few currencies, existing channels do not support small currencies; limited RMB withdrawal limits; unable to withdraw based on real-time exchange rates; unable to make direct payments to suppliers; difficulties in receiving payments from high-risk areas; and even troubles such as frozen cards and frozen funds.

2. There are three main operating models for cross-border underground money houses: cross-border “matching” model, “payment settlement” model, and other illegal operating models. Regardless of the model, they may be subject to criminal or administrative penalties.

3. The risks of receiving USDT in cross-border trade settlements are mainly: (1) Risks when receiving USDT: funds cannot be recovered and may even become part of a criminal offense; (2) Risks of holding USDT: large price fluctuations leading to depreciation, or inability to recover after being stolen; (3) Risks of investing in USDT: the possibility of being deemed an invalid entrusted investment contract and assuming risks; (4) Risks of cashing out USDT: losses of funds due to exchanges or over-the-counter (OTC) platforms running away, violation of foreign exchange, tax, and other national management regulations, and being subject to criminal or administrative penalties.

Like what you're reading? Subscribe to our top stories.

We will continue to update Gambling Chain; if you have any questions or suggestions, please contact us!