Author: Loki, Xinhuo Technology

Introduction: The author believes that MakerDAO’s adjustment of the DAI deposit APY (DSR) to 8% through the SLianGuairk Protocol is essentially compensating for the opportunity cost of holding traditional assets such as ETH and USDC, while emerging stablecoins like eUSD and DAI will continuously squeeze the market space of established stablecoins like USDC through high interest rates. At the same time, it is possible to separate the interest and circulation attributes of DAI to improve the capital utilization efficiency of MakerDAO’s DSR.

1. Starting from the growth of DAI

First, there is a question: why does MakerDAO provide a high yield of 8% for DAI? The answer is very clear – Maker wants to give up its own income and actively provide arbitrage opportunities to users/markets, achieving the growth of DAI scale through subsidies.

- What is special about Helio Protocol that Binance Labs invested 10 million US dollars?

- Evening Must-Read | An Inventory of 8 Old Projects in LSD’s Transformation

- The intersection of crypto gaming and the gambling industry Exploring from GGR to NGR

According to MakerBurn data, the supply of DAI has increased from 4.4 billion to 5.2 billion in the past four days. Obviously, this is directly driven by the high yield of 8% for DAI.

This increase in demand is reflected in two ways:

1) LSD re-collateralization. Since DSR provides a high yield of 8% for DAI, while the interest rate for minting DAI using wstETH is only 3.19%, this creates an arbitrage opportunity. If, based on Staking ETH, wstETH is used as collateral to mint DAI and deposit it into the SLianGuairk DSR, the calculated yield can be obtained based on minting $100 DAI with $200 worth of ETH collateral:

3.7% + (8% – 3.19%) / 200% = 6.18%

Obviously, this is better than direct staking and other unlocked, single-coin, low-risk yields in the market, so stETH holders will adopt this method of arbitrage, resulting in an increase in the circulation of DAI.

2) Exchanging other stablecoins for DAI. So how do those players without ETH or stETH participate? It’s simple, exchange USDT/USDC for DAI and then deposit it into DSR, after all, 8% is attractive both on-chain and off-chain, and this demand requires more DAI to meet, indirectly driving the circulation of DAI.

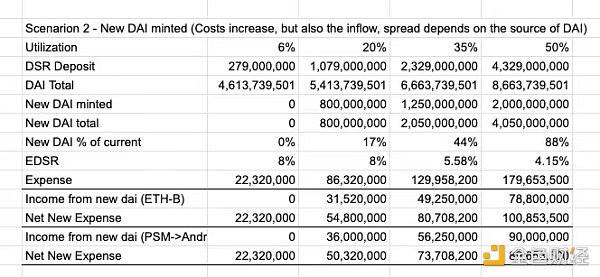

With the growth of DAI, it can be seen from the estimation of EDSR (Enhanced DAI Savings Rate) that the “Income from new DAI” has increased by 90 million.

This means that while the circulation of DAI is growing, the protocol will also have more USDC, which can be used to exchange for more dollars, purchase more RWA assets, provide more real returns, and bring about a flywheel effect.

2. Where does arbitrage end?

The second question is where does the growth of DAI end? The answer is when the arbitrage space becomes small enough. The premise of answering this question is to understand that the EDSR (Enhanced DAI Savings Rate) mechanism fundamentally provides arbitrage opportunities to users.

So for users who pledge stETH/rETH, stETH/rETH has no other purpose except to be used as collateral for minting DAI. Therefore, as long as the interest rate of EDSR is higher than the fee rate of minting DAI, there is an opportunity for profit.

The situation for USDT/USDC users is more complicated. Because USDC/USDT does not need to pledge minted DAI as collateral, it can be directly exchanged for DAI on the DEX. From the perspective of users, holding USDC in AAVE can earn an estimated yield of 2%, while converting it to DAI and depositing it in DSR can earn a yield of 8%, which is attractive. Therefore, there will be continuous exchanges by users.

Here comes a question. If Maker continues to exchange the USDT/USDC deposited by users for RWA (while keeping the DSR deposit rate stable), DSR should have a minimum yield, and this minimum yield should be higher than the on-chain risk-free yield of USDC/USDT. This means that this type of arbitrage should be able to continue for a long time, and DAI will continue to absorb the market share of USDT/USDC.

III. Similarities between RWA Yield and On-chain Staking Stablecoins: Eating into Traditional Stablecoins

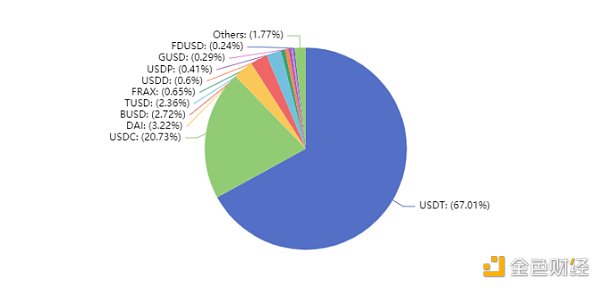

Of course, the road for DAI to take over Tether/Circle’s market share may not be so smooth, because DAI itself has some shortcomings (such as the security issue of RWA) and is still at a disadvantage in terms of scale. But don’t forget, DAI is not the only player trying to take over USDT/USDC. In addition to DAI, there are crvUSD, GHO, eUSD, Frax, and even Huobi and Bybit have launched their own RWA assets.

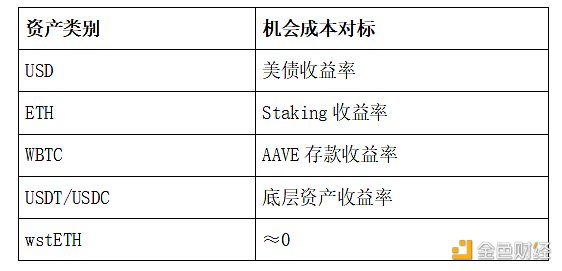

Here arises a division among stablecoin factions: Where does the underlying yield come from?

One faction is the approach taken by Huobi/Bybit, where the underlying yield comes entirely from the yield of RWA, and all that needs to be done is to return the portion of the yield invaded by Tether/Circle to the users. Another faction is pure on-chain collateral stablecoins like crvUSD and eUSD, where the underlying yield comes from the staking yield of the collateral in other protocols (which may expand to more scenarios in the future, such as using debt notes as collateral). DAI’s model actually combines these two sources of yield.

But all these types point to the same goal – reducing the opportunity cost, or compensating users for their opportunity cost (such as holding USDC, which is actually users giving up their opportunity cost to Circle for investing in traditional targets like US bonds).

If you choose to use wstETH to mint DAI, you can still earn Staking yield, without sacrificing any APY that belongs to you; if you choose to use ETH to mint eUSD, Lybra will charge a small fee, but most of the Staking APY still belongs to you. But when you use USD to purchase USDT/USDC, 4%-5% of the RWA yield is taken by Tether/Circle.

Tether’s net profit reached $1.48 billion in Q1 2023 alone. If DAI can fully replace Tether/Circle, it will bring in a real income of $5-10 billion to the cryptocurrency market every year. We often criticize the lack of real income scenarios in the cryptocurrency market, but we overlook the biggest one, which is also the simplest – just give back the income/opportunity cost that belongs to currency holders (for example, SLianGuairk can provide a DAI deposit rate as high as 8%, returning the opportunity cost paid by USD holders due to inflation).

In my opinion, embracing RWA or decoupling from RWA, and adhering to decentralization or catering to regulations, these different choices may coexist, but the route of eroding the market share of centralized stablecoins is clear. As long as the APY advantages of SLianGuairk or Lybra still exist, the market share of USDC/USDT will continue to be eroded. In this regard, the stability of RWA collateral model and the stability of on-chain native collateral are consistent.

4. A more efficient future: Separation of interest and circulation

Maker DAO’s SLianGuairk DSR also has a problem: entering DSR means exiting circulation, so the growth of circulation does not really contribute to actual business, but is a game of idle funds. So the question is whether there is a better solution? My answer is to separate interest and circulation.

The specific implementation is as follows:

Separation of DAI’s interest-bearing properties

Currently, when DAI is deposited into SLianGuairk, it becomes sDAI, and the income generated by DSR accumulates on sDAI. For example, when you initially deposit 100 DAI, it is converted into 100 sDAI. With the accumulation of DSR income, when you withdraw, you can exchange your 100 sDAI back into 101 DAI, and the extra 1 DAI is your profit.

The drawback of this mechanism is obvious: interest and circulation are a binary choice for DAI. After entering DSR, DAI loses its circulation ability, becoming a game of idle funds.

So, suppose we adopt a different approach. Instead of users depositing assets directly into SLianGuairk, they first deposit DAI into another protocol (let’s call it XLianGuairk for now). XLianGuairk then invests all the DAI into SLianGuairk for income accumulation. At the same time, XLianGuairk issues xDAI to users. XLianGuairk always ensures a 1:1 exchange ratio between xDAI and DAI; however, the income from DSR is only distributed based on the deposit amount of DAI, and xDAI holders cannot obtain any income.

The benefit of this approach is that xDAI can enter circulation, serving as a means of transaction, collateral, payment, and LP in DEX. Since xDAI can achieve rigid redemption with DAI, considering it as an equivalent to 1 USD will not pose any problems. (Of course, it would be a better choice for SLianGuairk itself or MakerDAO to issue xDAI.)

There is one potential issue here: if the adoption rate of xDAI is too low, will it be insufficient to support it as a trusted circulating asset? There is a corresponding solution to this problem. For example, the DEX scenario can adopt a virtual liquidity pool (or super liquid staking) to achieve:

1) The protocol initially pools $1m ETH and $1m DAI, with 80% of DAI deposited into DSR and 20% of DAI and ETH pooled together

2) When users swap, the remaining 20% is used for acceptance, and if the proportion of DAI rises or falls to a threshold (e.g. 15%/25%), the LP pool redeems or deposits from DSR.

3) If under normal circumstances, the transaction fees bring an LP mining APY of 10% and the DSR’s APY is 5%, then adopting a virtual liquidity pool under the same circumstances, LP can achieve:

An APY of 10% + 50% * 80% * 5% = 12%, achieving a 20% improvement in capital efficiency.

A more thorough separation

Let’s imagine another scenario where the collateral for a stablecoin includes national bonds RWA, ETH, WBTC, USDC, and USDT. The way to obtain the highest APY is to let RWA earn USD income, ETH earn staking income, WBTC earn AAVE current income, and USDT-USDC be used for LP in Curve. In summary, we try to put all collateral into an interest-earning state as much as possible.

Based on this, stablecoin issuance can be carried out. Let’s temporarily call it XUSD. XUSD cannot earn interest, and all income from collateral is distributed to the creators of XUSD based on minting volume and collateral type. This approach differs from the previous XLianGuairk approach in that XUSD has been separated into interest-earning and circulation functions from the beginning, maximizing the utilization efficiency of funds from the beginning.

Of course, the vision for XUSD seems to be still far away, and even xDAI has not yet appeared. However, the appearance of tradable DAI DSR certificates will be a certainty. If MakerDAO/SLianGuairk doesn’t do it, I believe that soon there will be third parties working on this. At the same time, Lybra v2 also plans to achieve this complete separation, with peUSD as the circulating currency and eUSD as the interest-earning asset after conversion.

In summary, the vision for xDAI or XUSD is still distant, but absorbing more real yields, maximizing capital efficiency as much as possible, and separating the functions of interest-earning and circulation will be a necessary path for on-chain stablecoins. Along this path, the twilight of the gods of USDC can be vaguely seen.

Like what you're reading? Subscribe to our top stories.

We will continue to update Gambling Chain; if you have any questions or suggestions, please contact us!