In 2023, the Cancun upgrade is undoubtedly one of the most critical industry events following the Shanghai upgrade. The L2 projects benefiting from it are also one of our key tracks to follow this year.

According to current information, the Cancun upgrade included in EIP4844 is expected to take place between October 2023 and January 2024. The token prices of the two main L2 projects, Arbitrum (referred to as ARB) and Optimism (referred to as OP), have experienced significant pullbacks after reaching new highs in the first half of the year. It may still be a better period for layout.

Of course, in terms of market capitalization, OP’s circulating market capitalization has been hitting new highs consistently after entering 2023, while ARB has been consolidating at a low level. In this article, the author attempts to sort out the following content:

-

The value source and business model of L2

-

Comparison of competitiveness and business data between OP and ARB

-

How the Cancun upgrade can significantly improve the fundamentals of L2

-

The potential risks of OP

The following content of the article represents the author’s phased views at the time of publication, with a focus on evaluating and interpreting from a business perspective and less emphasis on the technical details of L2. This article may contain factual errors and biases and is only intended for discussion, with the expectation of corrections from other investment research peers.

1. The value source and business model of L2

1.1 The value source and moat of L2

L2 provides products similar to L1, namely: stable, censorship-resistant, and open block space. We can also view it as a specialized on-chain cloud service. Compared to L1, the main advantage of L2 block space is its lower cost. Taking OP as an example, the average gas cost is only 1.56% of Ethereum’s.

Because block space is a specialized cloud service, it also means that its demand does not apply universally, and most internet services do not need to operate on L1 or L2. However, in the traditional world where there are many constraints and lack of transparency, financial services have the richest application practices on the blockchain.

The demand of service builders and users for L2 block space determines the upper limit of L2’s value.

Like L1, L2 can build a moat based on network effects.

On L2, the larger and more diverse the user base, the lower the difficulty for people to collaborate on L2, and new service models are more likely to emerge here to further meet and attract users into this network. Each new user entering and staying on the L2 network increases the potential value of this L2 network for other users.

In the Web3 world, the network effects of L1 & L2 are second only to stablecoins represented by USDT. The more dominant the L1 & L2, the higher their barriers, and as a result, they often enjoy higher valuation premiums.

1.2 The profit model of L2

The profit model of L2 is clear and simple. On the one hand, it purchases storage space from a trusted DA (Data Availability) layer to back up its L2 data (so that when there are problems with L2 operation, it can be restored using the backup data). On the other hand, it provides users with cheaper block space services and charges fees accordingly. Its profit comes from: L2 fees (base fees + MEV income) – costs paid to DA service providers.

Take OP and ARB as examples. They choose Ethereum as the DA layer, which has the highest degree of decentralization and credibility, and store their compressed L2 data on Ethereum by paying Gas. The fees they charge are the Gas paid by users (including ordinary users and developers) when they use their L2, as well as the MEV income. The latter minus the former is their gross profit.

The term “gross profit” is used because this part of the profit has not yet deducted other expenses of the project, such as labor costs, rewards for the ecosystem, and marketing expenses, etc.

The fee collection of L2 and the cost payment of L1 are both executed by the sequencer of L2, and the profit also belongs to the sequencer. Currently, the sequencers of OP and ARB are operated by the official party and the profit goes to the official treasury. Of course, a centralized sequencer means extremely high single-point risks, and both OP and ARB have long-term commitments to decentralize the sequencer.

It is very likely that the mechanism of decentralized sequencers will operate on a POS mechanism, which means that decentralized sequencers need to stake the native tokens of L2, such as ARB or OP, as credit deposits. When they fail to fulfill their responsibilities, the deposits will be slashed. Ordinary users can stake their own tokens as sequencers, or they can use staking services provided by platforms like Lido. Users provide collateral tokens, and professional and decentralized sequencer operators perform sequencing and uploading services. Staking users can receive the majority of L2 fees and MEV rewards from the sequencers (90% in the case of Lido’s mechanism).

By then, ARB and OP tokens will gain economic value empowerment in addition to governance.

1.3 ARB VS OP

Advantages of OP

Since its launch, ARB has consistently outperformed OP in various L2 business data. According to the L2 network effect mentioned earlier, as a leading L2, ARB should enjoy higher valuation premiums than OP.

However, this has gradually changed after OP proposed the Superchain strategy in February this year and began to actively promote the OP stack.

Op stack is an open-source L2 technology stack, which means that other projects wishing to run L2 can use it for free to quickly deploy their own L2, greatly reducing the cost of development and testing. Superchain is the future blueprint outlined by OP, which uses the L2s of OP stack. Due to the technical architecture consistency, these L2s can achieve secure, efficient, atomic-level communication and interaction of information and assets with each other, similar to Cosmos’ “Interchain”, called Superchain.

After the launch of OP stack and Superchain, they were first adopted by Coinbase. The L2 Base built with OP stack and the Superchain strategy were officially launched in February and on August 10th. With the demonstration effect of Coinbase, OP stack has gained more and more project adoptions, such as Binance’s opBNB, NFT project ZORA invested by LianGuaridigm, Loot ecosystem project Adventure Gold DAO, public goods service project Public Goods Network (PGN) supported by Gitcoin, leading options project Lyra, well-known on-chain data dashboard Debank, and even Celo, which was originally an L1, chose OP stack as its L2 solution.

The previous L2 projects served users who used their own block space, while Superchain and OP stack expanded the definition of users to include L2 operators. It transformed from a 2C business (here, L2 developers are also defined as C) to a 2B2C business, which created new sources of value and moat for OP:

-

Multi-chain network effect. By expanding the definition of “network” from a single chain to a “multi-chain network,” funds and information can be cross-chain linked between multiple chains through the standardized OP stack. L2 operators are responsible for user acquisition and operations, enlarging the total user population of the “multi-chain network.” The increase in the total population of the multi-chain network also enhances the value of each user and each L2 within the network.

-

Economies of scale. The fixed cost of technical infrastructure (such as the upgrade and maintenance of OP stack) is borne by OP, but the feedback and improvements provided by other OP stack users further improve the quality of OP stack. This reduces the cost of technical maintenance and upgrade, sorter and indexer incentives for single chains, and enhances the attractiveness to potential adopters of L2 solutions.

-

Community of interest. By bringing more Web3 industry giants into the OP ecosystem, it is easier to gain their support in various aspects such as technology, users, developers, and investments due to the consistency of interests.

By upgrading from a single-chain ecosystem to an interconnected chain ecosystem, OP not only benefits from the expected growth in the number of total users and developers, but the main business data of the OP main chain is also continuously approaching or even surpassing ARB, which used to be far ahead of it, for example:

a. Monthly active addresses: The weekly active addresses of OP/ARB have risen from a low of 32.1% to the current 73.6%

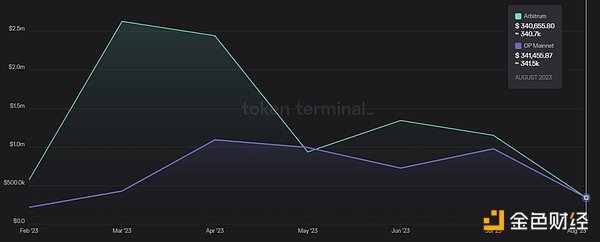

b. Monthly L2 profits: The L2 profits of OP/ARB have risen from a low of 16.4% to the current 100.2% (surpassing)

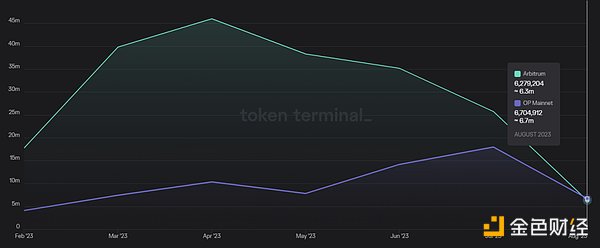

c. Monthly interaction times: The monthly interaction times of OP/ARB have risen from a low of 22.4% to the current 106.5% (surpassing)

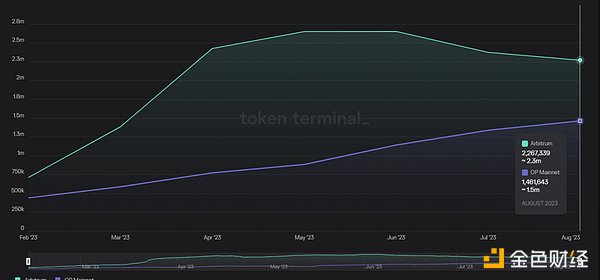

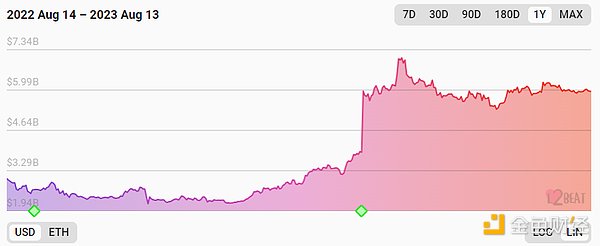

d. On-chain funds: The on-chain TVL of OP/ARB has increased from 1/3 of the low point to 1/2 of the current level.

OP’s on-chain funds TVL was around 2 billion in March and is currently around 3 billion.

ARB’s on-chain funds TVL was around 6 billion (peaking at 7 billion) in March and is still around 6 billion.

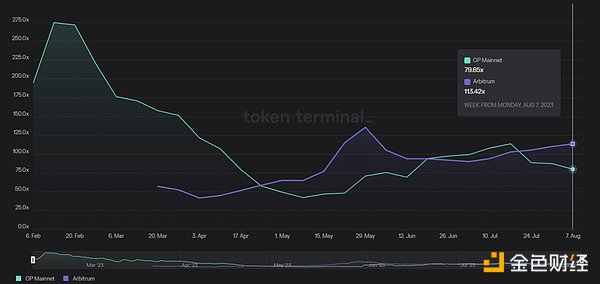

Comparison of OP and ARB valuations

Corresponding to the rapidly rising business data of OP, the valuation of OP’s main chain is becoming more and more attractive compared to ARB.

P/E (market cap/annualized profit of L2): Based on the revenue of the past week, OP’s PE has dropped to below 80, while ARB’s is 113. This is achieved even in the case of significant OP price strength and continuous increase in circulating supply.

Rapid development of new forces in the OP ecosystem

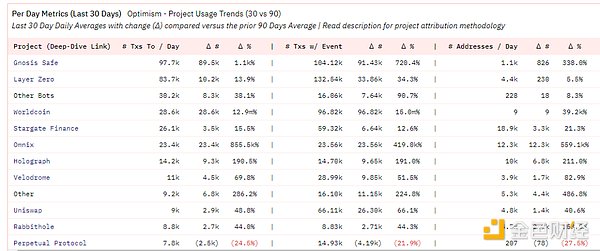

In addition to the continuous catching up of OP’s main chain business data with ARB, the new business partners joining the OP camp have made a greater contribution. For example, among the projects that have contributed the most to the number of transactions in the past 30 days on the OP main chain, Gnosis Safe ranks first and Worldcoin ranks fourth.

In fact, a large number of transactions in Gnosis Safe are also contributed by the Worldcoin team. As early as the end of June this year, World App had deployed over 300,000 Gnosis Safe accounts, which was caused by the migration from World App accounts to the Optimism mainnet.

According to the official website data of Worldcoin on August 11th, the number of registered users has exceeded 2.2 million, and in the past 7 days, 257,000 new accounts have been created. The average daily transfer volume of World app is as high as 126,000, which is equivalent to about 21% of the current daily transfer volume of OP and ARB mainnets.

Currently, Worldcoin has only migrated its ID system and tokens to the mainnet, and will develop application chains based on the OP stack in the future, which is expected to bring more active users and developers.

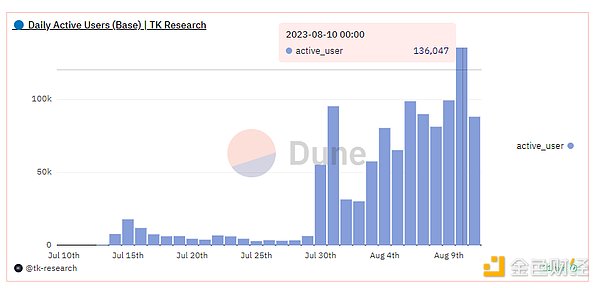

In addition to Worldcoin’s contribution to the OP mainnet, the data growth of Coinbase’s Base L2, the first and largest supporter of OP stack L2, after its launch is also very strong. On August 10th, the number of active addresses reached 136,000, just one step away from the L2 TOP1, ARB, with 147,000.

Among all smart contract L1&L2, this data ranks only after Tron (1.5M), BNBchain (1.04M), Polygon (0.37M), and Arbitrum (0.14M). In addition, the first popular application after Base’s official launch on August 10th is not the traditional DeFi or Meme, but a social application called friend.tech, which is even more surprising.

The dilemma of ARB

The dilemma of ARB lies in the fact that although it has a strong L2 main chain called Arbitrum one, a higher-performance Arbitrum nova, and an Orbiter L3 stack that competes with the OP stack, it is willing to define itself as L3 and use Arbitrum one as its DA layer’s flagship project. However, in the stage where L2 is thriving, there are not many projects with better industrial resources (users, developers, IP content) that are willing to build on L2. This means a higher valuation ceiling and a more targeted user base.

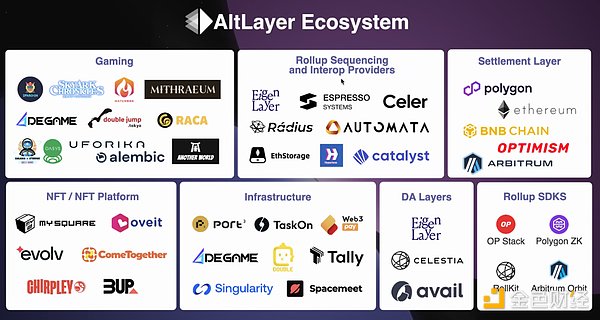

In the smaller Rollup project market, Arbitrum’s Orbiter faces competition from RaaS (Rollup as a service) projects represented by ALTLayer. ALTLayer provides low-threshold, low-code rollup construction and operation solutions, integrating various modules of rollup available in the market for users to build and combine like playing with LEGO blocks.

Among the rollup options provided in the RaaS project’s menu, Orbiter offered by Arbitrum is just one of the choices. Small users may choose an economically affordable L2 solution instead of defining themselves as L3 after comparing the options.

In this situation, although Arbitrum one remains slightly ahead in terms of business data compared to other L2s as a single-chain L2, its market share among the entire L2 market is actually declining rapidly because a large number of new and old users are flowing to OP series and hybrid series L2s.

Overall, OP’s strategy of introducing partner users through an open-source L2 suite in a B2B2C model creates network effects that give it a clear advantage in the business aspect compared to the strong single-chain approach of Arbirtum. If ARB does not adjust its strategy in the future, its position as the king of L2 single-chain is also at risk.

2. How will the Cancun upgrade improve the fundamentals of L2 projects?

2.1 Estimated valuation of ARB and OP projects

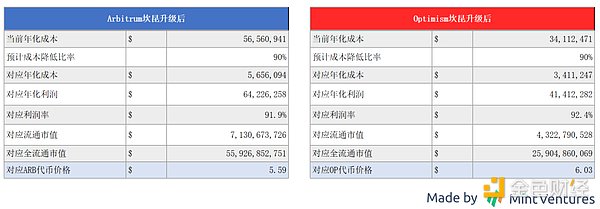

We estimate the valuation levels of ARB and OP based on their revenue data for the past three months and the current price.

If we assume that the P/E ratio remains unchanged and the Cancun upgrade reduces the L1 costs of ARB and OP by 90% (EIP4844 is expected to reduce L1 costs of L2 by 90-99%, and we take a conservative estimate, see reference for details), the price calculations for ARB and OP are as follows:

The reduction in L1 costs brought by the Cancun upgrade directly leads to increased profits and an increase in valuation.

2.2 Impact of Cancun Upgrade on L2 Valuation

Of course, with the cost reduction of L1 after the Cancun upgrade, both ARB and OP cannot avoid reducing the fees for the corresponding L2. Therefore, when estimating the valuation, we also need to consider two variables:

1. How much ratio of cost reduction will ARB and OP pass on to users in the form of lower L2 fees

2. How much ratio of increase in L2 transaction activity will be brought about by the lower L2 fees

Based on the assumption that the P/E multiple remains unchanged, I have deduced the prices of ARB and OP tokens after the Cancun upgrade based on the changes in the values of “the ratio of cost reduction converted into fee reduction” and “the increase in the number of transactions resulting from the fee reduction”:

The core logic of the two token price estimation tables above is:

-

The lower the ratio of cost reduction benefiting L2 users after the Cancun upgrade, the higher the operating profit of L2

-

The higher the ratio of increase in transfer activity brought about by the lower second-layer fees, the higher the operating profit of L2

In addition, because the current gas fees of OP are about 30-50% lower than ARB, with the reduction in L1 costs, OP has more room to retain the saved costs. Therefore, I believe that OP has a space of 60-100% to transfer the saved costs as subsidies to users, while ARB has a space of 70-100%.

Based solely on the impact of the Cancun upgrade on the prices of OP and ARB on a single chain, the upside potential of OP and ARB is relatively similar.

Of course, the above analysis of the price sensitivity of ARB and OP after the Cancun upgrade is relatively mechanical, and at least the following factors have not been considered:

-

The above analysis is based on the current project’s PE and the current PE already includes expectations for the Cancun upgrade

-

When the Cancun upgrade arrives, OP will have more token emissions compared to the present, and assuming the circulating market value remains unchanged, the token price should be lower

However, the unchanged logic is that the higher the operating profit of L2, the higher the intrinsic value of its token, and the easier it is to obtain a higher market valuation. The Cancun upgrade will bring significant marginal improvements to L2 projects in terms of cost savings and increased on-chain activity.

3. Potential Risks of OP

As mentioned above, relying on the narrative of Superchain and the widespread adoption of OP stack, OP has upgraded from a single-chain L2 to an interconnected L2 ecosystem in a B2B2C manner, introducing more ecological population through OP stack partners, which have stronger network effects, economies of scale, and common interests in the long term, making it a better business model than ARB. In addition, the main business data of the OP mainnet has been catching up with or even surpassing ARB in recent months, and other OP stack L2s like BASE have also developed rapidly, further squeezing ARB’s market share.

Considering that the L2 main chains of OP and ARB benefit from similar expectations of token price appreciation due to the Cancun upgrade, but OP has the support of Superchain narrative, it is currently seen as a better investment target.

However, the competition in the L2 track is still fierce, and the following risks of OP need to be considered:

3.1 ARB chooses to open its own L2 license and compete for the total network population of L2 in a manner similar to OP

Currently, Arbitrum still uses a commercial code license (BSL), and other partners who want to build the Rollup ecosystem using the Arbitrum stack either need to obtain formal authorization from the Arbitrum DAO or Offchain Labs (the development company of Arbitrum), or develop L3 based on Arbitrum one. However, with the rapid expansion of the OP stack in recent months and the surge in network population, the Arbitrum community is starting to become restless. On August 8th, stonecoldLianGuait, a member of the ARB team, posted a discussion on the governance forum, hoping that the community can participate in the discussion on “the conditions and timing of Arbitrum issuing code usage licenses to partners”. The specific discussion topics include:

-

Understanding the community’s attitude towards granting code usage licenses to other partners of Arbitrum

-

Discussing whether additional conditions should be added to the license authorization

-

How to establish an evaluation mechanism to determine whether to issue licenses to the other party

-

Short-term and medium-term roadmap for the above content

-

In the short term, determine which compliant partners can be issued licenses

-

In the medium term, clarify the standards so that any compliant partner can obtain a license

The discussion post also summarized the feedback received by the official on this topic, including:

“Arbitrum Foundation or Offchain Labs has not yet issued licenses for the Arbitrum software stack to large strategic partners, which seems to be a strategic mistake. This indecision may actually harm the Arbitrum ecosystem.”

“We have not received any feedback suggesting that the Arbitrum Foundation should not issue licenses for the Arbitrum technology stack to strategic partners. Most of the concerns are about the standards for issuing licenses and the conditions that should be attached, and allowing the DAO to provide preliminary opinions on the process.”

Based on the above situation, the OP-ization of Arbitrum’s future strategy has become a definite trend, and it will soon join the competition in the “L2 interconnected chain” market. This will inevitably pose a threat to the comprehensive development of the current OP stack.

On August 9th, Andre Cronje, co-founder and architect of Fantom Foundation, stated in an interview with The Block that they are considering the Optimism L2 solution, including both the Op stack and the Arbitrum stack. In my opinion, as a former first-tier L1, it is impossible for Fantom to consider operating as an L3 for Arbitrum. When AC mentioned “Arbitrum stack,” he should be referring to the L2 solution.

However, the problem lies in how long it will take for the Arbitrum community and partners to reach an agreement and start issuing licenses. How many core customers will still be available in the market at that time? The longer this process takes, the more collaborators will join the OP stack ecosystem, which will be detrimental to ARB.

3.2 Intense competition in the overall L2 service market

In addition to ARB and OP, the ZK family of L2 is also rapidly developing or waiting to go online. Examples include ZKsync with impressive business data (although there is a significant bubble due to airdrop hunters), Linea backed by Consensys (with Metamask having 30 million monthly active users and Infura having over 400,000 developers), and the highly anticipated Scroll, among others. In addition, Rollup as a Service platforms such as Altlayer, by providing a low-threshold modular assembly and operational service for Rollup developers and operators through service aggregators, directly enter the upstream of the OP stack, which will also squeeze the bargaining power of the OP ecosystem.

3.3 The development of the Superchain ecosystem and whether value can be transmitted to the OP Foundation and OP tokens

OP tokens currently do not have a direct means of capturing value. Among the many adopters of the OP stack, except for BASE, which explicitly donates 10% of its L2 profits to the OP Foundation, other cooperative projects have not yet made similar commitments. The validation of value capture for OP tokens may have to wait until the official launch of its decentralized sequencer protocol to observe the acceptance of major OP stacks. If everyone can support and adopt a decentralized sequencer system with OP as collateral, there will inevitably be a direct demand for OP, completing the value transmission. However, if each L2 still implements its own sequencer standard or operates with its own node system, it will not only prevent OP from capturing value but also weaken the synergy between L2s within the OP ecosystem.

3.4 Valuation risk

In the previous section on the valuation of OP, it was mentioned that the calculation of the OP price increase brought about by the Cancun upgrade was based on the assumption that “the PE of OP L2 remains consistent after the upgrade.” Considering that the Cancun upgrade is one of the most anticipated events in the market this year, the current OP PE valuation has more or less already priced in this expectation. For those who hold a pessimistic view, they may even believe that the current PE has already priced in the benefits of Cancun.

References

-

ASXN: EIP-4844 Research Report

-

The Block: Fantom is exploring adding optimistic rollups to connect to Ethereum

-

Supporting EIP-4844: Reducing Fees for Ethereum Layer 2 Rollups

Like what you're reading? Subscribe to our top stories.

We will continue to update Gambling Chain; if you have any questions or suggestions, please contact us!